Is the banking system well capitalized?

The top US financial regulators say they are stepping up scrutiny of how exposed banks are to commercial real estate, as vacancy rates increase. The Financial Stability Oversight Council said in a statement Friday that delinquency rates are low, but empty offices are on the rise. The group, which was set up after the global financial crisis, includes the heads of the Treasury Department, the Federal Reserve and the Securities and Exchange Commission. “Regulators are taking steps to emphasize risk management and examine exposures to CRE loans at their regulated institutions,” the group said. After several wild months in finance during which three midsize banks failed, Washington’s watchdogs are under pressure to get in front of any looming issues. During their Friday meeting, the regulators discussed “the ability of market participants to manage their interest-rate risk and liquidity risk in the current economic environment,” the group said. Overall, the group, which is known as FSOC, said that the banking system was “well capitalized.” The Fed and the Federal Deposit Insurance Corp. have been peppering lenders with questions related to interest-rate risks and commercial real estate exposure, Bloomberg News reported last month. Federal Chair Jerome Powell on Wednesday said “we do expect that there will be losses” in commercial real estate, and banks that have concentrations in that area will experience bigger losses.

0 Comments

They are down around 10%.

Lennar Corp., the second-largest US homebuilder, is calling an end to falling housing prices — but doesn’t yet see a recovery in sight. “Home prices have come down about 10%,” executive chairman Stuart Miller said Thursday in a Bloomberg Television interview. “They’re probably going to remain right there at least for the foreseeable future.” He qualified that assessment by saying his outlook was subject to change in the event of interest rates moving higher, a day after Miami-based Lennar reported quarterly earnings and the Federal Reserve announced a pause in its hiking cycle. A chronic shortage of affordable housing units in the US will keep the market tight, Miller said. Investors may be signaling that their concerns about homebuilding are easing. Lennar is heading for its highest close on record, eclipsing the $116.91 mark set in December 2021. The shares rose 3.7% to $119 at 2:23 p.m. in New York, buoyed by Lennar’s boost in its forecast for full-year new-home deliveries and quarterly beats against estimates for gross margins and new orders. Miller said on an earnings call that the average sales price of a new Lennar home was now $450,000, down from a peak of $500,000 last year. The exuberant demand that marked the COVID-19 pandemic has withered under the pressure of the fastest rate-hiking cycles in Fed history, crimping prices. Inventory of existing houses has evaporated as owners choose to stay put rather than move and borrow at higher rates, and builders have benefited as new buyers enter the market. Still, lower prices have dented Lennar’s profitability, a metric Miller said is likely to remain lower than it once was. New homeowners, including young people who have lived at home with their parents, have become the principal drivers of demand for Lennar homes, Miller said, while “those that have that 3%, 4% mortgage are going to be very reluctant to give up that interest rate.” They are down around 10%.

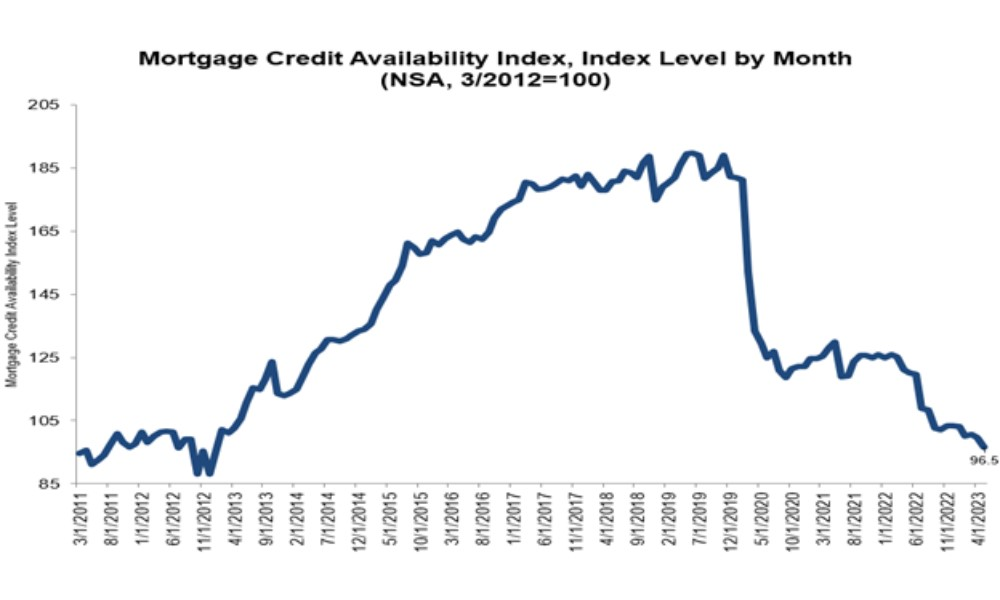

Lennar Corp., the second-largest US homebuilder, is calling an end to falling housing prices — but doesn’t yet see a recovery in sight. “Home prices have come down about 10%,” executive chairman Stuart Miller said Thursday in a Bloomberg Television interview. “They’re probably going to remain right there at least for the foreseeable future.” He qualified that assessment by saying his outlook was subject to change in the event of interest rates moving higher, a day after Miami-based Lennar reported quarterly earnings and the Federal Reserve announced a pause in its hiking cycle. A chronic shortage of affordable housing units in the US will keep the market tight, Miller said. Investors may be signaling that their concerns about homebuilding are easing. Lennar is heading for its highest close on record, eclipsing the $116.91 mark set in December 2021. The shares rose 3.7% to $119 at 2:23 p.m. in New York, buoyed by Lennar’s boost in its forecast for full-year new-home deliveries and quarterly beats against estimates for gross margins and new orders. Miller said on an earnings call that the average sales price of a new Lennar home was now $450,000, down from a peak of $500,000 last year. The exuberant demand that marked the COVID-19 pandemic has withered under the pressure of the fastest rate-hiking cycles in Fed history, crimping prices. Inventory of existing houses has evaporated as owners choose to stay put rather than move and borrow at higher rates, and builders have benefited as new buyers enter the market. Still, lower prices have dented Lennar’s profitability, a metric Miller said is likely to remain lower than it once was. New homeowners, including young people who have lived at home with their parents, have become the principal drivers of demand for Lennar homes, Miller said, while “those that have that 3%, 4% mortgage are going to be very reluctant to give up that interest rate.”  "The depressed supply of government credit is particularly significant". Mortgage supply fell again in May against the backdrop of an industry facing a period of consolidation and reduced capacity, according to the Mortgage Bankers Association. MBA’s Mortgage Credit Availability Index (MCAI) tumbled 3.1% month over month to 96.5 in May, marking the third-straight month of declines and a tightening in lending standards.  “Mortgage credit availability decreased for the third consecutive month, as the industry continued to see more consolidation and reduced capacity as a result of the tougher market,” said Joel Kan, MBA’s deputy chief economist. “With this decline in availability, the MCAI is now at its lowest level since January 2013.”

The Conventional MCAI dropped 2.3%, while the Government MCAI fell 3.8% in May. Of the component indices of the Conventional index, the conforming MCAI slipped 3.9% to its lowest level in the survey’s history dating back to 2011. According to Kan, the jumbo index saw a 1.5% decrease, its first contraction in three months as some depositories assess the impact of recent deposit outflows and reduce their appetite for jumbo loans. “Additionally, lenders pulled back on loan offerings for higher LTV and lower credit score loans, even as loan applications continued to run well behind last year’s pace,” Kan explained. “Both conventional and Government indices saw declines last month, and the Government index fell by 3.8% to the lowest level since January 2013. In a market where a significant share of demand is expected to come from first-time homebuyers, the depressed supply of government credit is particularly significant.”  But affordability index is still well below the breakeven point of 50.

Housing affordability showed signs of easing in the first quarter, according to the National Association of Home Builders (NAHB). The NAHB)/Wells Fargo Housing Opportunity Index (HOI) improved by 38.1% from the Q4 2022 reading, the lowest level since 2012, thanks to lower home prices and solid wage gains. HOI data showed that the national median home price declined to $365,000 in the first quarter from $370,000 in the previous quarter. Additionally, long-term mortgage rates averaged 6.46% in Q1, down from a series-high of 6.80% in Q4. The US median family income jumped 7% from $90,000 in 2022 to $96,300 in 2023. The quarterly HOI increase brings the share of new and existing homes affordable to families earning the US median income of $96,300 to 45.6% of all homes sold in Q1. However, the index remained significantly lower compared to the first quarter 2022 reading of 56.9%, a reminder of ongoing building material supply chain issues and other affordability challenges. “Elevated interest rates and higher home prices coming out of the pandemic have left housing affordability conditions considerably lower on a year-over-year basis,” said NAHB chief economist Robert Dietz. “While affordability posted a gain in the first quarter, it is still well below the breakeven point of 50. The lack of housing units is the primary cause of the nation’s housing affordability challenges, and the best way to reduce housing costs and fight inflation is to put into place policies that will allow builders to construct more attainable housing.” “An uptick in housing affordability in the first quarter of 2023 corresponds to a rise in builder sentiment over the same period as well as an increase in single-family permits,” said NAHB chairman Alicia Huey. “And while buyer conditions improved at the beginning of the year, builders continue to wrestle with a host of affordability challenges. These include a shortage of distribution transformers and concrete that are delaying housing projects and raising construction costs, a lack of skilled workers, and tightening credit conditions.”  They are under serious pressure.

The stock market is growing more sanguine about US regional banks, but the lenders still face serious pressure. A credit “contraction is invariably coming,” Soros Fund Management Chief Executive Officer Dawn Fitzpatrick said at this week’s Bloomberg Invest conference, adding that additional banks will fail because “there are more problems under the surface.” One further source of trouble for the industry will be commercial real estate, an area that in recent years smaller and regional banks have become a bigger force in. Working from home has cut into office values and almost $1.5 trillion of commercial property debt is due for repayment before the end of 2025. Meanwhile, rising interest rates have made many properties less valuable. “US banks have become much more vulnerable to a decline in commercial real estate prices,” Torsten Slok, chief economist at Apollo Global Management Inc., wrote in an email to clients this week. The upshot is that 700 US banks now exceed the Federal Deposit Insurance. Corp.’s guidance from 2006 on commercial real estate loan concentration, he calculated. Two years ago, it was less than half that number. There were about 4,700 FDIC insured US banks as of the end of March. The guidelines were introduced in 2006 to address loan concentration and risk management deficiencies among banks in relation to commercial property loans. Those who exceed them are potentially subject to greater supervisory scrutiny, including higher capital levels and heightened risk management practices. The FDIC declined to comment. Its chairman Martin Gruenberg said last month that potential problems with property portfolios will be a matter of “ongoing supervisory attention” and that “despite the recent period of stress, the banking industry has proven to be quite resilient.” Small minnows Some banks are already shrinking their exposure to commercial real estate. PacWest Bancorp, one of the US lenders engulfed in the commotion, is selling a $2.6 billion portfolio of real estate construction loans to shore up liquidity. “The small minnows” have the “lion’s share of the exposure,” Monsur Hussain, head of research for global financial institutions at Fitch Ratings, said on a webinar this week. “They have approximately 14% of their total assets in CRE exposures, but it can be as high as over 40% of their total assets.” Any further regional bank failures would likely make credit even more difficult to access for property developers and landlords, especially those who are smaller or lower quality. The headwinds mean office values are now down 27% on average from their recent peak after falling further in the past month, according to Green Street. The average commercial property is down 15%. “There’s not much transacting these days because buyers and sellers can’t seem to agree on pricing,” Peter Rothemund, co-head of strategic research at the firm, said in a report this week. “These situations eventually resolve themselves, and usually it’s in favor of the buyers.” The trouble is also beginning to feed through to the commercial mortgage-backed securities market where about $140 billion of the assets are due to mature this year. In recent years, an increasing portion of the loans that were packaged into CMBS were interest only, according to data compiled by Trepp. More than 4% of office loans packaged into the securities were at least 30 days in arrears as of May, according to a recent report by the real estate data firm. That’s the highest level since 2018. “We expect commercial real estate more broadly to remain under pressure given the immediacy of the maturity wall at a time where the single-largest lender – regional banks – is experiencing an elevated rate of scrutiny,” Morgan Stanley analysts including Jay Bacow wrote this week.  Monthly increase signals possibility of continued heightened activity.

The US housing market saw heightened foreclosure activity in May, as widely anticipated, according to ATTOM’s latest report. Foreclosure filings (default notices, scheduled auctions, or bank repossessions) surged 7% from April and were up 14% from a year ago to 35,196 properties across the country. Of that figure, lenders repossessed 4,020 properties through completed foreclosures (REOs) in May, a 38% increase from the previous month and up 41% from May 2022. “The recent increase in foreclosure filings nationwide indicates a trend that has been observed throughout the year and what we have expected to occur,” said Rob Barber, CEO at ATTOM. “This upward trajectory suggests the possibility of continued heightened activity, and with foreclosure completions seeing the largest monthly increase this year, we will continue to monitor the potential impacts this may have on the housing market.” According to the report, one in every 3,967 housing units had a foreclosure filing in May. States with the highest foreclosure rates were Illinois (one in every 2,144 housing units with a foreclosure filing), Maryland (one in every 2,203 housing units), New Jersey (one in every 2,257 housing units), Florida (one in every 2,470 housing units), and Ohio (one in every 2,478 housing units). Foreclosure starts increased 4% month over month and 5% year over year to 23,245 properties in May. Florida had the greatest number of foreclosure starts (2,901 foreclosure starts), followed by California (2,451 foreclosure starts), Texas (2,286 foreclosure starts), Illinois (1,358 foreclosure starts), and New York (1,287 foreclosure starts).  Tenants are canceling or not renewing their leases.

Near-empty office buildings, already a problem plaguing US cities, are becoming a worry for mortgage bondholders as landlords fall behind on repayments at the fastest rate in five years and the difficulty of refinancing the loans grows. The work-from-home phenomenon spawned by the COVID-19 pandemic and a slowing economy are pushing tenants to cancel or not renew leases, making building owners miss loan payments. More than 4% of office loans packaged into securities were at least 30 days in arrears as of May, the highest level since 2018, according to a recent report from real estate data firm Trepp. The rise in delinquencies is leading some investors to avoid commercial mortgage-backed securities with too much exposure to office buildings, in turn causing some CMBS yields to spike. Slack demand may make matters worse for real estate borrowers who anticipated refinancing almost a quarter of mortgages on office buildings this year. “This is just the tip of the iceberg for office delinquencies as $35 billion in CMBS office loans are scheduled to mature this year and the refinancing market is effectively shut to this asset class,” said Dan McNamara, founder of Polpo Capital Management. Polpo is betting against securities backed by office loans. Brookfield Corp. and a Pacific Investment Management Co. office landlord are among major institutional owners that have defaulted on large office mortgages this year. A venture started by WeWork Inc. and Rhone Group defaulted on a loan for a San Francisco office tower. The loan defaults raise the specter of missed payments to holders of commercial mortgage bonds. Delinquencies for all loans in commercial real estate securities jumped the most last month in almost three years, according to Trepp. In May, Kroll Bond Rating Agency said it is looking at downgrading securities tied to 11 commercial mortgage bonds, because the bonds are backed at least in part by office properties that are weakening. Should Kroll decide to cut its rating on all the debt, it would be its biggest such action since July 2020, early in the pandemic. For their part, CMBS investors say the shaky loan environment is pushing them to buy only deals backed by high-quality loans. The dropoff in demand all but shuttered the new-issue market earlier this year, and debt sales are down by almost 80% from this time last year, according to Bloomberg data. Several recent deals were noticeable for the relatively small number of big office building loans in the pool of mortgages being packaged for sale. Also, borrowers and underwriters have become more flexible in tailoring new issues to meet investor concerns, said John Kerschner, head of US securitized products at Janus Henderson Group, in an interview. “Office exposure in conduit deals has gone down this year, and if bond buyers are uncomfortable with specific loans and the issuer wants to get the deal done, they may very well take it out of the pool,” Kerschner said. Conduit transactions repackage different types of mortgages, including offices. Existing debt that rebundles a variety of commercial real estate loans is yielding among the most in over a decade in the secondary markets, over 5.5% in recent trading sessions, according to one measure. “Most of the risk is already priced in,” Kerschner said. “Investors who worried about offices left the market earlier and the rest is moving up the capital stack in general, looking for the investment-grade portions of the bonds.”  Applications fall again as homebuyers grapple with steep rates.

Mortgage demand cooled for the fourth week in a row as interest rates hover near record highs, according to the Mortgage Bankers Association. Mortgage application volume was down 1.4% during the week ending June 2 – seasonally adjusted for the Memorial Day holiday. When unadjusted, applications plunged 12% week over week. Demand for home loans declined despite a drop in rates, MBA deputy chief economist Joel Kan noted. “The 30-year fixed rate dipped to 6.81%, 10 basis points lower than last week but still the second highest rate of 2023,” Kan said in MBA’s news release. “Overall applications were more than 30% lower than a year ago, as borrowers continue to grapple with the higher rate environment.” MBA’s refinance index decreased 1%, and the purchase index decreased 2% from the previous week. On the other hand, the refinance share of mortgage activity increased six basis points to 27.3% of total applications. Applications for FHA loans increased to 13.2% from 12.7% the week before. The VA share rose to 12.5% from 12.1%, while the portion of USDA loan applications slipped to 0.4% from 0.5% the week prior. “Purchase activity is constrained by reduced purchasing power from higher rates and the ongoing lack of for-sale inventory in the market, while there continues to be very little rate incentive for refinance borrowers,” Kan said. “There was less of a decline in government purchase applications last week, which was consistent with a growing share of first-time home buyers in the market.”  It's another blow for a struggling downtown.

Park Hotels & Resorts Inc. has stopped making payments on a loan tied to the Hilton San Francisco Union Square and the Parc 55 San Francisco, two of the city’s largest hotels, dealing another blow to a downtown struggling with remote work and mounting public safety concerns. Park is working with servicers on the $725 million loan to determine the best path forward for the 1,921-room Hilton property and the 1,024-room Parc 55 hotel, according to a statement Monday. The company expects that it will eventually remove the hotels from its portfolio. “Now more than ever, we believe San Francisco’s path to recovery remains clouded and elongated by major challenges,” chief executive officer Thomas Baltimore said in the statement. The city faces “record high office vacancy; concerns over street conditions; lower return to office than peer cities; and a weaker-than-expected citywide convention calendar through 2027.” The last few years have been tumultuous for hotels, which were battered by early Covid lockdowns. While leisure travel has enjoyed a robust rebound, business trips have been slower to recover, putting stress on big properties in urban areas. San Francisco hotels have been especially vulnerable. The city’s office market has seen occupancies plummet, as tech employers embrace work-from-anywhere models and cut back on office space, and startups started worrying about their ability to raise new money. The city itself is facing worsening budget challenges, with the majority of residents saying San Francisco is on the wrong track. The San Francisco Travel Association estimates that the area will get 23.9 million visitors this year, down from 26.2 million in 2019. That’s led to falling demand for hotels. Occupancy rates for San Francisco hotels were just under 70% in the first four weeks of May, according to lodging data provider STR. By comparison, New York City hotels were 86% full during the same period. In the case of the Park properties, stopping payments on the non-recourse loan, which was funded through the commercial mortgage-backed securities market and matures in November, will remove a drag on the company’s balance sheet and operating performance, according to the statement. |

|

- iMove Chicago

- Real Estate School

-

Laws

-

CRLTO

>

- 5-12-010 Title, Purpose And Scope.

- 5-12-020 Exclusions.

- 5-12-030 Definitions.

- 5-12-040 Tenant Responsibilities.

- 5-12-050 Landlord’s Right Of Access.

- 5-12-060 Remedies For Improper Denial Of Access.

- 5-12-070 Landlord’s Responsibility To Maintain.

- 5-12-080 Security Deposits.

- 5-12-081 Interest Rate On Security Deposits.

- 5-12-082 Interest Rate Notification.

- 5-12-090 Identification Of Owner And Agents.

- 5-12-095 Tenants’ Notification of Foreclosure Action.

- 5-12-100 Notice Of Conditions Affecting Habitability.

- 5-12-110 Tenant Remedies.

- 5-12-120 Subleases.

- 5-12-130 Landlord Remedies.

- 5-12-140 Rental Agreement.

- 5-12-150 Prohibition On Retaliatory Conduct By Landlord.

- 5-12-160 Prohibition On Interruption Of Tenant Occupancy By Landlord.

- 5-12-170 Summary Of Ordinance Attached To Rental Agreement.

- 5-12-180 Attorney’s Fees.

- 5-12-190 Rights And Remedies Under Other Laws.

- 5-12-200 Severability.

- Illinois Eviction Law (Forcible Entry And Detainer)

- Illinois Security Deposit Return Act

-

CRLTO

>

- Today's Cool Thing

- Social Media