Home renovations – leave the drama for the screen.

When a homebuyer is focused on watching a home renovation show, are their eyes really open to everything that goes into homeownership? Jason Smith (pictured), head of revenue at Cloudvirga, knows his way around the mortgage game. But he too has been caught off-guard with the realities of homeownership. Smith recently made the move from Missouri to northeast Florida, and with the warmer weather, came new realities of living in the tropics that he had never had to contend with before. He moved into a new build and shortly after arriving, “We’re looking at a filtration system and a water softener,” an investment of nearly $7,000. “Frankly, it’s a necessity. But it’s another cost. I didn’t think that within the first week I would be spending this much money,” for such a device. Another Florida reality was a type of mosquito he had never dealt with before. “I like to think I’m educated,” he said. “I’ve been in the industry for a long time. I’ve owned a home before. But there are inherent differences associated with moving to a different region.” Water softeners and paying to get rid of mosquitos had not crossed his mind. The machinery and contracted bug services are now installed at his house, but Smith knows that others are not as lucky as he is to absorb such a cost. And it helped him better see the blind spots that might go into home buying and renovations. “We tend to think that it is a Millennial thing,” he said, “but it’s not. If you’re not working with a true partner, and you’re not getting educated as far as everything that’s included in (the purchase), even things as simple as the cost of utilities, can be detrimental to the bottom line. People don’t think about that when you get an older house. Your utilities are going to be twice as much as they are with a new house - because you’re not going to have the insulation. You’re not going to have the windows or the efficiencies that have developed in the last few years. Old houses cost more in every way.” Another cost that can be overlooked are HOA fees or development fees, which can add up. A monthly $600 fee can add more than $100,000 on to the price over time. And don’t forget about special assessments, everyone’s favourite when the condo needs a new roof, or the community rec room needs a new water heater, “or the neighbourhood needs new pool bathrooms because the teenage hoodlums have somehow lit them on fire – yeah, that happened,” he said. Renovation realities So what about fixer-uppers? Like many people, Smith has watched his share of home renovation shows on TV, where an old eyesore is turned into a home with impressive curb appeal in 30 minutes. “I’m a total DIY guy,” said Smith with a grin. “I have every kind of tool you can imagine,” having learned a lot from his dad. But watching those shows “always cracks me up,” when someone who has never swung a hammer before is suddenly, in the next scene, helping pull down a wall. Most viewers know that editing and some Hollywood magic is at play on these shows. But when it is your home renovation, on your budget, reality comes into play. “Your idea is that I’m going to make this home what I want it to be in three months,” working on it every weekend, for example, which may not be realistic. “It’s really interesting how a lot of those people are buying in areas without necessarily thinking where it’s going to be, in a few years, or where it is now.” He joked that people like to buy in up-and-coming areas – but don’t think about the years it takes for the area to up-and-come, and those intervening years can cause extreme “buyer’s remorse.” He worries that the reality show effect creates “false hope and false understanding… they don’t realize how much psychological and emotional pressure that puts on you.” This is where lenders and brokers can help mitigate a client’s expectations about a Fix and Flip. During a home refinance, Smith was finishing up some paperwork with a couple to help them access some money to pay off some debt. Looking at how much money they were saving, one of the duo looked at their spouse and said: “I can go shopping again!” Smith used this as a learning opportunity and politely but firmly told them, “I’ll see you again in 12 months, which I really didn’t want to do.” He believes that brokers and agents need to be a “true advocate” for their clients, even if it means being frank. “I have long said that the wrong person, the wrong lender, will bury you in whatever house that you want,” Smith said. “And that’s a matter of folks overstepping their boundaries because, even if you go by Fannie Mae, Freddie Mac, DTI guidelines, and if you have good credit, and if you have good assets, you can get buried into, frankly, anything.” Just because a home may fall within your financial threshold “doesn’t necessarily mean that it’s the smartest move for you.” Balancing realities with fantasies, when people “get really excited about the possibilities as opposed to the realities,” puts brokers and agents in a necessary and important place in the conversation: The Realistic Voice. Education conversation “Our responsibility is to make sure they’re seeing the realities of the situation as well as the dream,” he said. While some churches require a marriage preparation course before a couple ties the knot, and new drivers need to pass a driving test, most conventional home buying “does not require any sort of education.” There are exceptions, with some states that offer downpayment assistance which typically require some education. There are anti-steering laws, and professional guardrails, but for homebuyers, “The people they rely on most are going to be the real estate agent and their mortgage person, their bank, as far as education,” he said. “What we can do is create real education for them.” Rather than just showing a client how much they can afford, the education can extend to rehabbing your home, future costs, maintenance, unexpected costs, etc. “It’s going to set you up as an advocate for your borrower or your realtor partners,” he said. “And it’s going to get you more business and it’s going to give you more meaningful relationships that are going to help grow your business. But it’s also going to help start to create better generational borrowers.” He added that “as an industry, it behooves us to be proactive in that Reality Education process. Sometimes building trust is simply pointing out Reality, not simply agreeing. And building trust leads to retaining clients.”

0 Comments

Deceptive mortgage ads have led to a $1 million fine and a permanent ban on the company.

The Consumer Financial Protection Bureau (CFPB) has dealt a decisive blow to RMK Financial Corporation (dba Majestic Home Loans) by permanently banning it from the mortgage lending industry. The ban comes after RMK repeatedly engaged in deceptive advertising practices that targeted military families, falsely implying an affiliation with the US government. In 2015, the CFPB issued an agency order against RMK for misleading advertisements to military families that implied the company was affiliated with the United States government. Despite the order, RMK engaged in a series of repeat offenses, including sending millions of mortgage advertisements to military families that deceptively used fake US Department of Veterans Affairs (V.A.) seals, the Federal Housing Administration (FHA) logo, and other language or design elements to falsely imply government affiliation. The penalty includes a $1 million fine, which RMK must pay to the CFPB’s victims relief fund. RMK is also permanently banned from engaging in any mortgage lending activities, including advertising, marketing, promoting, offering, providing, originating, administering, servicing, selling mortgage loans, or even assisting others in doing so. “Even after the 2015 law enforcement order, RMK continued to lie to military families by falsely implying government endorsement of its home loans,” CFPB director Rohit Chopra said in a statement. “Our action reflects our commitment to weed out repeat offenders, and we are shutting down this outfit for good.” RMK is a privately held corporation licensed as a mortgage broker or lender in at least 30 states and Puerto Rico, originating consumer mortgages, including VA-guaranteed and FHA-insured mortgages. However, RMK is affiliated with neither government agency.  Freddie Mac points to reasons behind the increase.

Freddie Mac’s Primary Mortgage Market Survey has revealed a rise in mortgage rates, with the 30-year fixed-rate mortgage averaging 6.50% as of February 23, 2023. This represents a notable increase from the previous week’s average of 6.32% and a significant jump from the 3.89% recorded at the same time last year. The 15-year fixed-rate mortgage has also seen an uptick, averaging 5.76%, up from last week’s 5.51%. Sam Khater, chief economist of Freddie Mac, said interest rates are repricing to account for the stronger-than-expected economic growth, tight labor market, and the threat of inflation. Khater recommends that homebuyers shop around among lenders to save on their mortgage. “Our research shows that rate dispersion increases as mortgage rates trend up,” he said. “This means homebuyers can potentially save $600 to $1,200 annually by taking the time to shop among lenders to find a better rate.” Homebuyer affordability declined in January, according to the Mortgage Bankers Association. The national median payment applied for by purchase applicants rose 2.3% to $1,964.  Given inflation, 'subdued sentiment' abounds. CBRE’s 2023 US Investor Intentions Survey released on Thursday reveals “subdued sentiment” among commercial real estate investors – with nearly 60% expected to purchase less real estate this year and just 15% planning to buy more. “Almost half of respondents expect to decrease purchasing by more than 10%,” researchers wrote. “Investors are also hesitant to sell assets as market pricing falls. Sixty per cent (60%) say they will either sell less or not sell at all, while only 27% expect to sell the same amount as last year.” Sentiment among lenders has soured as well, the survey found. The survey found nearly 60% of respondents expect to decrease lending activity this year. However, just 10% plan to meaningfully reduce their allocation to real estate, while 67% said they will either maintain or increase capital availability for the sector. “CBRE expects that the slowdown in investment and lending activity in the first half of the year will lower total investment volume in 2023 by approximately 15% from 2022,” the authors wrote. “However, as Federal Reserve policy and economic conditions become more predictable around midyear, we expect investment and lending activity to recover.” When will inflation come down in 2023?The key considerations for buying and lending expectations this year are when inflation will peak and where interest rates will end up, according to the survey. About 50% of investors believe inflation will peak in Q1 or Q2, while 35% believe it has already peaked. Along with high inflation, most investors expect higher borrowing costs. More than 70% of surveyed investors believe the 10-year Treasury rate will exceed 3.75% at year-end 2023. Lenders shared a similar outlook on inflation, with 48% of those surveyed believing it will peak in Q1 or Q2 and 33% believing it has already peaked. Lenders also expect higher borrowing costs, but to a lesser degree than many investors. More than 50% of surveyed lenders believe the 10-year Treasury rate will exceed 3.75% by year-end, while 43% believe it will finish the year between 3.00% and 3.75%. Both investors and lenders highlighted rising interest rates as a key challenge for commercial real estate activity in 2023. Uncertainty about the direction of interest rates will limit real estate investment activity, particularly in the first half of the year. Nevertheless, CBRE believes that inflation and borrowing costs will not be as high as many investors and lenders expect. We forecast that the 10-year Treasury rate and inflation (CPI) will end the year at 3.2% and 4.0%, respectively. What is the most profitable sector of real estate?

Where is the best place to invest in 2023? Both investors and lenders indicated a strong preference for fast-growing secondary markets, particularly in the Sun Belt, including Austin, Texas; Atlanta; Miami; Nashville, Tenn.; Charlotte, N.C.; San Diego, Calif.; and Raleigh, N.C. Many investors expect these markets to outperform in 2023. Other preferred markets included Los Angeles and Dallas/Fort Worth.   If you thought the increases were over, think again...

Federal Reserve officials continued to anticipate further increases in borrowing costs would be necessary to bring inflation down to their 2% target when they met earlier this month, though almost all supported a step down in the pace of hikes. “Participants observed that a restrictive policy stance would need to be maintained until the incoming data provided confidence that inflation was on a sustained downward path to 2%, which was likely to take some time,” according to the minutes of the Jan. 31-Feb. 1 gathering released in Washington on Wednesday. The minutes also said “almost all” officials agreed it was appropriate to raise interest rates by 25 basis points at the meeting, while “a few” favored or could have supported a bigger 50 basis-point hike. US central bankers raised interest rates by a quarter-point, moderating their action after a half-point hike in December and four consecutive jumbo-sized 75 basis-point increases. The move lifted the benchmark policy rate into a range of 4.5% to 4.75%. Both Chair Jerome Powell and the minutes indicated that officials are prepared to raise rates further to produce a broader slowdown in the economy that tamps down inflation. “Participants generally noted that upside risks to the inflation outlook remained a key factor shaping the policy outlook, and that maintaining a restrictive policy stance until inflation is clearly on a path toward 2% is appropriate from a risk-management perspective,” the minutes said. A number of officials said that an “insufficiently restrictive” policy stance could stall recent progress on moderating inflation pressures, according to the minutes. The economy exited 2022 “with more momentum in the labor market and risks around inflation” than Fed officials likely expected, said Michael Gapen, head of US economics at Bank of America Securities. “We need to see broad-based disinflation, and we didn’t get that in recent data.” Gapen’s forecast is for the Fed to continue tightening to a range of 5.25% to 5.5%, one hike above the 5.1% median officials forecast in December. Bets tempered Going into the meeting, money markets forecast interest-rate cuts in the back half of 2023. They have since tempered bets on the likelihood that the Fed will reverse course and start cutting rates before the end of this year. Kathy Bostjancic, chief economist at Nationwide Life Insurance Co., said she raised her forecast for the peak federal funds rate to a range of 5.25% to 5.5% given the strong employment and inflation data for January. Payrolls increased 517,000 that month, while the consumer price index, excluding food and energy prices, rose 5.6% from a year earlier. Following the release of the minutes, swaps traders kept steady their conviction that the Fed will keep pushing rates higher, with the market indicating that 25 basis-point hikes are likely coming at the March, May and June meetings. Investors lifted expectations for where rates will peak to around 5.36%. Treasury yields fluctuated while remaining lower on the day while the S&P 500 index closed slightly lower and the dollar remained higher. The shift in sentiment has also helped tighten financial conditions somewhat — potentially aiding the central bank as it fights to bring inflation under control amid a tight job market. In the minutes Wednesday, Fed officials said that it was important “that overall financial conditions be consistent with the degree of policy restraint that the Committee is putting into place in order to bring inflation back to the 2% goal.” Cleveland Fed President Loretta Mester said last Thursday that she had seen a “compelling” economic case for a half-point increase during the last meeting, a view echoed later that day by St. Louis Fed chief James Bullard. Neither official votes on policy decisions this year.  It's a 12th straight monthly hit.

Sales of previously owned US homes unexpectedly declined for a 12th-straight month in January, extending a record decline and underscoring how high mortgage rates continue to stifle housing activity. Contract closings slipped 0.7% at the start of the year to an annualized pace of 4 million, according to data from the National Association of Realtors on Tuesday. The pace of purchases, which was the weakest since 2010, fell short of the median projection of 4.1 million in a Bloomberg survey of economists. Still, the pace of monthly sales declines has slowed. Houses are also sitting on the market for longer, leading some sellers to accept lower prices. That, in turn, could help alleviate the affordability challenges stemming from the Federal Reserve’s rapid increase in interest rates. “Home sales are bottoming out,” Lawrence Yun, NAR’s chief economist, said in a statement. “Inventory remains low, but buyers are beginning to have better negotiating power.” “Homes sitting on the market for more than 60 days can be purchased for around 10% less than the original list price,” Yun said. Properties remained on the market for 33 days on average at the start of the year, up from 19 days a year earlier. That’s helping to put downward pressure on home prices. The median selling price was up just 1.3% from a year earlier, the smallest annual gain in home prices in nearly 11 years, to $359,000. Some 54% of homes sold were on the market for less than a month. The number of homes for sale edged up to 980,000 in the month, the NAR data showed. It would take 2.9 months to sell all the homes on the market, unchanged from a month earlier. Realtors see anything below five months of supply as indicative of a tight market. Homebuilder sentiment has also begun to improve, which may point to a pickup in new-housing inventory in the months ahead. Mortgage rates have also eased from their highs last year, further aiding affordability. Digging deeper

Sharp drop in mortgage applications attributed to the sudden surge in mortgage rates.

Mortgage applications plummeted by 13.3% from the prior week, with purchase applications reaching their lowest level since 1995, according to the latest data from the Mortgage Bankers Association’s weekly survey. The decline comes as the 30-year fixed rate soared to 6.62% - its highest rate since November 2022. The refinance index posted a 2% decrease from the previous week and was 72% lower than the same week one year ago. Meanwhile, seasonally adjusted purchase applications decreased by 18% from the previous week, and the unadjusted purchase index decreased by 4% compared to the previous week. “This time of the year is typically when purchase activity ramps up, but over the past two weeks, rates have increased significantly as financial markets digest data on inflation cooling at a slower pace than expected,” said MBA deputy chief economist Joel Kan. “The increase in mortgage rates has put many homebuyers back on the sidelines once again, especially first-time homebuyers who are most sensitive to affordability challenges and the impact of higher rates.” The refinance share of mortgage activity increased to 32.5% of total applications from 32% the previous week. The adjustable-rate mortgage (ARM) share of activity increased to 7.6% of total applications. Overall, Kan anticipates that refinance activity will remain depressed for some time, given that rates are over 2.5 percentage points higher than a year ago. The report also showed a decline in the FHA share of total applications, which decreased to 12.1% from 12.6% the week prior. The VA share of total applications fell to 12% from 12.6% the previous week, and the USDA share of total applications remained unchanged at 0.6%.  One key risk is to blame.

US homes in areas prone to floods may be currently overvalued in the range of $121 billion to $237 billion, according to a report published Thursday in the journal Nature Climate Change. Roughly, that number is derived by looking at how much homes are selling for now and subtracting the estimated average annual losses that they will incur from flooding over the next 30 years (the average length of a mortgage in the US), as determined by the First Street Foundation, a non-profit that seeks to improve awareness of climate change-related risks like increased flooding. The report was authored by researchers from First Street, the Environmental Defense Fund and Resources for the Future, among others. The discrepancy in value was particularly significant in counties along the coasts in places where disclosure of flood risk isn’t required in real estate transactions, the study found. Although high-value homes along Florida’s Gold Coast accounted for the largest part of the absolute amount of valuation differential, low-income households stand at risk of losing the largest share of home value. “The consequence of this financial risk and how the housing market responds really depend on policy choice on who bears the cost of climate change,” said Jesse Gourevitch, a fellow with the Environmental Defense Fund and the lead author of the report. “It is really critical that flood risk is better communicated to property owners.” It has long been understood that flood risk is not adequately priced into homes or flood insurance . In many cases, buyers are simply not aware, since federal government maps outlining risk zones are outdated and difficult to access. Moreover, state laws vary on how much flood-disclosure risk is required when homes are sold. In addition, lower costs in the short run tend to sway buyers to underestimate the likelihood and severity of flooding over time. Historically, the federal government has aided and abetted this risky decision-making with subsidized flood insurance. First Street tried to make the risks more transparent in 2020 by publishing its own analysis of flood risk for every property in the lower 48 states. This paper builds on that data by estimating how much of that flood risk is now priced into homes and how much still isn’t. Researchers found that the market has absorbed some of the risk, but up to $237 billion is still outstanding, much of it in states like Florida, which have not only rising risk of flooding as the climate warms but also don’t generally mandate that sellers share flood risks with potential buyers. The distribution of overvaluation is highly skewed to expensive properties — 11% of properties contribute to 80% of overvaluation. And a large portion of overvaluation is driven by properties that are not covered by severe flood zones specifically designated by the government, the researchers found. While a few expensive properties bear great risk, the study found that among census tracts in the lowest quintile of household median income, higher percentages of properties are overvalued compared to their flood risk. If they were devalued to match the real risk, homeowners could lose up to 10% of their homes’ value.  Uptick spurred by increase in consumer spending as US economy bounces back.

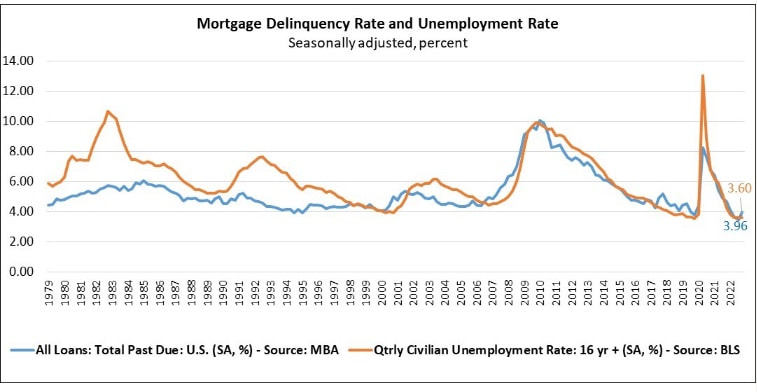

Freddie Mac’s latest survey has shown that the 30-year fixed-rate mortgage increased for the second week in a row, now averaging 6.32%. This marks a 20-basis point jump from 6.12% last week and above the 3.92% average a year ago at this time. The 15-year fixed mortgage rate climbed to 5.51% from 5.25% the previous week. A year ago, it was 3.15%. “Mortgage rates moved up for the second consecutive week,” said Sam Khater, Freddie Mac’s chief economist. “The economy is showing signs of resilience, mainly due to consumer spending, and rates are increasing. Overall housing costs are also increasing and therefore impacting inflation, which continues to persist.” Consequentially, home loan applications fell 7.7% week over week, according to the Mortgage Bankers Association. Refinance applications were down 13%, and purchase activity declined 5% compared to the prior week. “Mortgage rates increased across the board last week, pushed higher by market expectations that inflation will persist, thus requiring the Federal Reserve to keep monetary policy restrictive for a longer time,” said MBA deputy chief economist Joel Kan. “Mortgage applications decreased for the second time in three weeks because of these higher rates. Refinance borrowers, both rate/term and cash-out, remain on the sidelines as current rates provide little financial incentive to act.”  However, foreclosure starts were down despite ongoing economic challenges. The delinquency rates for loans on residential properties increased at the end of 2022 amid economic headwinds and inflationary pressures, the Mortgage Bankers Association reported Thursday. Mortgage delinquency rates rose to a seasonally adjusted rate of 3.96% in the fourth quarter, up 51 basis points from the third quarter but still down 69 basis points from a year ago. The share of loans on which foreclosure actions were started in Q4 dropped by one basis point to 0.14%.  “As expected, the overall national mortgage delinquency rate increased in the fourth quarter of 2022 from its previous quarterly survey low,” said Marina Walsh, vice president of industry analysis at MBA. “The weaker economy and ongoing inflationary pressures contributed to the uptick in delinquencies. The delinquency rate – while still low – increased from the previous quarter across all loan types and across all stages of delinquency.”

Walsh noted that, for the last 15 years, mortgage delinquencies have tracked very closely with employment conditions. The Bureau of Labor and Statistics’ latest report showed 517,000 jobs added in January, with the unemployment rate hovering at 3.4%. However, despite indicators of a resilient labor market, MBA still expects slower hiring and rising unemployment, with the rate growing to 5.2% by the end of the year. “This will mean further increases in mortgage delinquencies,” the trade association said in a statement. “Notwithstanding the fourth-quarter increase in mortgage delinquencies, the foreclosure starts rate of 0.14% was well below the historical quarterly average of 0.40%,” Walsh added. “Many distressed homeowners have loss mitigation options available to them and have accumulated home equity, which can ease financial hardship and avert foreclosure actions.” |

|

- iMove Chicago

- Real Estate School

-

Laws

-

CRLTO

>

- 5-12-010 Title, Purpose And Scope.

- 5-12-020 Exclusions.

- 5-12-030 Definitions.

- 5-12-040 Tenant Responsibilities.

- 5-12-050 Landlord’s Right Of Access.

- 5-12-060 Remedies For Improper Denial Of Access.

- 5-12-070 Landlord’s Responsibility To Maintain.

- 5-12-080 Security Deposits.

- 5-12-081 Interest Rate On Security Deposits.

- 5-12-082 Interest Rate Notification.

- 5-12-090 Identification Of Owner And Agents.

- 5-12-095 Tenants’ Notification of Foreclosure Action.

- 5-12-100 Notice Of Conditions Affecting Habitability.

- 5-12-110 Tenant Remedies.

- 5-12-120 Subleases.

- 5-12-130 Landlord Remedies.

- 5-12-140 Rental Agreement.

- 5-12-150 Prohibition On Retaliatory Conduct By Landlord.

- 5-12-160 Prohibition On Interruption Of Tenant Occupancy By Landlord.

- 5-12-170 Summary Of Ordinance Attached To Rental Agreement.

- 5-12-180 Attorney’s Fees.

- 5-12-190 Rights And Remedies Under Other Laws.

- 5-12-200 Severability.

- Illinois Eviction Law (Forcible Entry And Detainer)

- Illinois Security Deposit Return Act

-

CRLTO

>

- Today's Cool Thing

- Social Media