With work-from-home becoming the new normal thanks to the COVID-19 pandemic, more residents in expensive coastal cities like San Francisco and New York are looking to move to cheaper inland areas – accelerating a trend that has been going on for at least five years.

According to proptech firm Redfin, 27.8% of its users looked to move to another metro area in July – up from 27.4% in the second quarter and 25.2% in July 2019. And their destinations of choice: Sacramento, Phoenix, and Las Vegas. Veronica Clyatt, a Redfin agent in Pleasanton, a city just outside San Francisco, said that a lot of people moving away from the Bay Area have “had it in the pipeline for a while, and remote work is accelerating the process.” “People who can work remotely are re-examining where they want to live, and for most of them that means they're looking at places that are less expensive,” said Clyatt. “I've had buyers drop out of their search in the Bay Area because they're moving to Sacramento or Texas, and I've had people moving over to Pleasanton because it's less expensive than San Francisco.” Meanwhile, Marco Di Pasqualucci, a Redfin agent in Las Vegas, said that the city’s current market is experiencing a “feeding frenzy,” with low inventory and no shortage of interested buyers. “We're seeing mass migration of people from other states moving into Nevada,” said Di Pasqualucci. “The lack of state income tax, warm climate and the relatively low cost of housing – you can buy a nice home for around $300,000 – make Las Vegas an attractive place for people looking to move away from expensive areas.” On the other end of the spectrum, the top five places with Redfin identified as having the biggest net outflow in July were New York, San Francisco, Los Angeles, Washington DC, and Chicago.

0 Comments

Yesterday, ATTOM Data Solutions released its Vacant Property and Zombie Foreclosure Report for the third quarter of 2020, finding that just over 1.5 million U.S. residential properties, or 1.6 percent of all homes in the country, are currently sitting vacant.

That many empty homes at a time when supply levels are painfully low is problematic in its own right. But what happens when a vacant or abandoned property also faces the risk of foreclosure? ATTOM discovered that of the almost 216,000 properties involved in foreclosure proceedings in the third quarter, 7,961, or three percent of them, are vacant. While that is a small portion of the country’s housing stock, the number of properties that have been abandoned and deemed ‘zombie foreclosures’ has risen three percent since the second quarter. “Abandoned homes in foreclosure remain little more than a spot on the radar screen in most parts of the United States, posing few, if any, problems from neighborhood to neighborhood,” said ATTOM’s chief product officer, Todd Teta. But Teta conceded that the increase in zombie foreclosures “throw a small potential red flag into the air.” The rise in abandoned properties signals a variety of potential causes, none of them good. First, it’s safe to assume the owners of these homes are suffering financial distress so acute that they are willing to walk away from their properties, and future borrowing opportunities, completely. Second, abandoning a property at a time when homeowners have been permitted the opportunity to delay their mortgage payments implies that they may not have been made aware of their forbearance options. Finally, and related to the first point, these homeowners may be so despondent and disheartened by their country or state’s inability to help them and their family through the COVID-19 crisis that they’ve allowed hopelessness or nihilism to determine what could be the most damaging financial decision of their lives. But zombie foreclosures aren’t just an effect. By slowing the foreclosure process, they also cause practical problems of their own. “The longer a foreclosure process takes, the more likely it is that the home will be abandoned, and vacant homes are even more of a safety hazard than usual during a global pandemic,” Rick Sharga, executive vice president of RealtyTrac, told Mortgage Professional America. Sharga feels its imperative that abandoned properties are processed and sold as quickly as possible to avoid blight and provide housing supply at a time when the country desperately needs it. “As Federal, State, and local governments and industry regulators consider extending their foreclosure moratoria, it would be prudent for them to consider simultaneously allowing for the accelerated processing of vacant and abandoned foreclosure properties,” he said. ATTOM found that zombie foreclosure rates rose from Q2 to Q3 in every state but Hawaii. (The district of Columbia also experienced a decline.) The states with the largest increases were Kansas, Missouri, Georgia, Kentucky and Nebraska. Each state saw its proportion of zombie foreclosures rise to at least 10 percent. The most affected metropolitan areas in Q3 were Peoria, Kansas City (MO), Omaha, and Cleveland. Those with the lowest zombie foreclosure rates include Austin, Philadelphia, Los Angeles, Charlotte, and San Francisco.  The coronavirus pandemic has thrust millions of American small businesses into crisis mode, as they scramble for the cash they need to get through to more normal times. One way Congress can help: Protect them from predators looking to take their money and leave them bankrupt.

Bloomberg News has reported extensively on the “merchant cash advance” companies that prey on plumbers, pizzerias, nail salons and other small businesses across the country. They skirt lending laws by structuring their products as advances against future revenue. They employ bucket-shop marketing tactics, offering seemingly sweet deals that obscure outrageous fees and interest rates sometimes exceeding 400%. Their collection practices border on extortion, ranging from draining bank accounts without business owners’ knowledge to surprise visits from a guy named Gino. Now, entrepreneurs are particularly vulnerable, as lockdowns slam the economy and federal aid fails to reach many of those most in need. As Federal Trade Commissioner Rohit Chopra put it, “this is opening the door to even more predatory actors looking to profit from the pain of small business owners.” After the Bloomberg News investigation, officials addressed some specific cases and practices. The FTC, the Securities and Exchange Commission and New York’s attorney general sued a number of companies — run by people including a convicted real-estate scammer and a former drug trafficker — for transgressions ranging from threatening kidnapping to overcollecting on debts. And New York legislators shut down a legal loophole that allowed cash-advance companies to use the state’s courts to seize the assets of small businesses nationwide, with no notice or hearing. Yet the predatory behavior will keep coming back in new forms until Congress corrects a major omission: the lack of any consistent rules for lending to small businesses, akin to those that already exist for consumers. These should include clear disclosure of terms and interest rates, accountability for the brokers who sell the loans, and federal constraints on contracts that allow creditors to seize assets unilaterally. Legislators should also designate a federal agency to enforce the rules wherever they should apply. Congresswoman Nydia M. Velázquez, the chairwoman of the House Small Business Committee, has introduced legislation that would do what’s needed and put the Consumer Financial Protection Bureau in charge. Her colleagues across the aisle, who often express admiration for small business, should offer their support. Entrepreneurs should be able to focus on getting through this crisis and doing what they do best, not trying to anticipate the myriad ways in which unscrupulous lenders might deceive them and destroy what they’ve built.  The Federal Housing Finance Agency’s new 50-basis-point fee could cost borrowers an extra $21,000, according to a new analysis by Mortgage Capital Trading (MCT).

The “Adverse Market Refinance Fee” (AMRF) was announced by Fannie Mae and Freddie Mac last week, and will be applied to cash-out and no-cash-out refinances, with the exception of some types of construction conversion mortgages, effective Sept. 1. Fannie Mae cited “market and economic uncertainty” as justification for the fee, but the decision has been widely condemned by industry groups. Now MCT says the new rule will cost borrowers big. “According to data from the MCTLive! Secondary marketing platform, MCT estimates increases in borrower rates of up to 0.375%, leading to the average borrower paying as much as an additional $21,000 over the typical thirty-year loan term,” MCT said in an email to MPA. “These FHFA-directed price adjustments do more than work against the hopeful economic rebound and the original agency charters – they undermine trust and spur uncertainty at a crucial time,” said Phil Rasori, chief operating officer of MCT. “The only way lenders can protect themselves from these risks is to increase margins across the board – according to our analysis, on the order of 75 to 100 basis points in total.” The upshot of these margin increases, exacerbated by the short notice given by the FHFA, will be higher housing costs to borrowers, and a drag on the overall economy, according to MCT’s analysis. “The short notice amounts to effectively no time for lenders and borrowers to react, as the typical thirty-day rate lock and the practice of ‘floating’ a rate both hurt respectively in this case,” MCT said. “Beyond the issue of timing, these actions are perpendicular to the efforts of the Federal Reserve and the administration to assist consumers and stimulate the economy in the face of the COVID-19 pandemic.” According to MCT, the average $280,000 mortgage will cost an additional $58 per month as a result of the new fees – amounting to $2,800 in the first four years and $21,000 over a 30-year term. In California, where the average mortgage is just under $400,000, borrowers could pay almost $30,000 more over the full term. MCT also estimated that the cost increases will be 34% higher than they would have been if the new fees were simply passed through to buyers, “indicating the significant effect of lender uncertainty due to the way the changes were communicated.” “Whether or not economic headwinds justify these ‘adverse market’ fees, their needlessly short-notice implementation introduced ongoing risks and increased negative impacts to borrowers,” said Curtis Richins, president of MCT. “A more traditional 90-day notice would have minimized uncertainty and borrower cost increases with a negligible difference in the long-term capitalization of Fannie Mae and Freddie Mac.”  Federal Housing Administration mortgages -- the affordable path to homeownership for many first-time buyers, minorities and low-income Americans -- now have the highest delinquency rate in at least four decades.

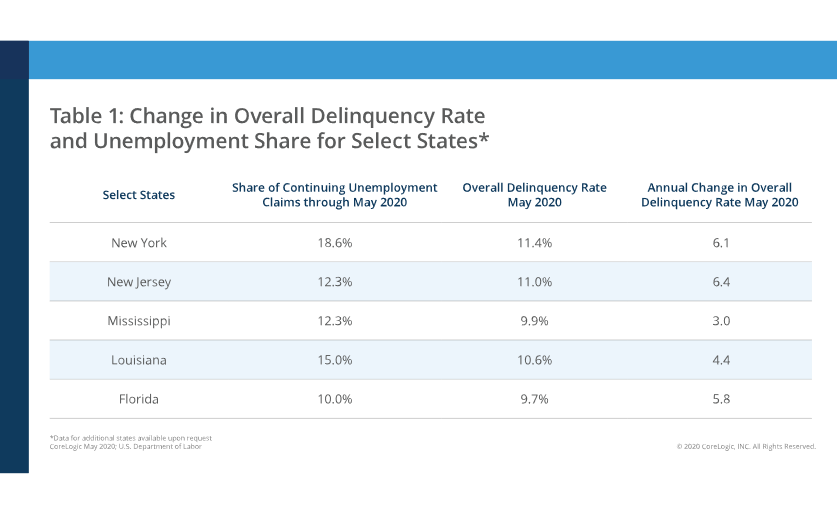

The share of late FHA loans rose to almost 16% in the second quarter, up from about 9.7% in the previous three months and the highest level in records dating back to 1979, the Mortgage Bankers Association said Monday. The delinquency rate for conventional loans, by comparison, was 6.7%. Millions of Americans stopped paying their mortgages after losing jobs in the coronavirus crisis. Those on the lower end of the income scale are most likely to have FHA loans, which allow borrowers with shaky credit to buy homes with small down payments. For now, most of them are protected from foreclosure by the federal forbearance program, in which borrowers with pandemic-related hardships can delay payments for as much as a year without penalty. As of Aug. 9, about 3.6 million homeowners were in forbearance, representing 7.2% of loans, the MBA said in a separate report. The share has decreased for nine straight weeks. Housing has held up better than expected in an otherwise shaky economy, with record-low mortgage rates fueling sales of both new and previously owned houses. With job losses mounting and Congress slow to act on a fresh stimulus package, that momentum could be threatened. New Jersey had the highest FHA delinquency rate, at 20%. The state also had the biggest increase in the overall late-payment rate, jumping to 11% in the second quarter from 4.7%. Following were Nevada, New York, Florida and Hawaii -- all states with a high proportion of leisure and hospitality jobs that were especially hard-hit by the pandemic, the MBA said. But the current spike in delinquencies is different from the Great Recession, thanks in part to years of home-price gains and equity accumulation, according to Marina Walsh, vice president of industry analysis for the bankers group.  With the US unemployment rate still hovering at historically high levels, many homeowners struggled to make their monthly mortgage payments in May. Mortgage delinquency rates continued to climb nationwide, according to CoreLogic's Loan Performance Insights Report. By May, 7.3% of mortgages were in some stage of delinquency (at least 30 days past due, including homes in foreclosure). The May delinquency rate represented a 3.7% uptick compared to the 3.6% a year ago. "The national unemployment rate soared from a 50-year low in February 2020 to an 80-year high in April," said Frank Nothaft, chief economist at CoreLogic. "With the sudden loss of income, many homeowners are struggling to stay on top of their mortgage loans, resulting in a jump in non-payment." The early-stage delinquency rate (30 to 59 days past due) was 3%, up from 1.7% in May 2019. The share of adverse delinquencies (mortgages 60 to 89 days past due) was 2.8%, up from 0.6% the same period last year. The share of mortgages 90 days or more past due, including those in foreclosure, rose from 1.3% in May 2019 to 1.5% in May 2020. This marked the first year-over-year increase in the serious delinquency rate since November 2010, according to the report. However, the foreclosure inventory rate was down from 0.4% a year ago to 0.3% – the second straight month the US foreclosure rate was at its lowest level for any month since at least January 1999.  "Government and industry relief programs have helped to cushion the initial financial blow of the pandemic for millions of US homeowners," said Frank Martell, president and CEO of CoreLogic. "COVID-19 and the resulting pressures continue to influence the economic activity of many households. Barring additional intervention from the Federal and State governments, we are likely to see meaningful spikes in delinquencies over the short to medium term."

Without further government programs and support, CoreLogic forecasted the US serious delinquency rate to quadruple by the end of 2021, pushing 3 million homeowners into serious delinquency.  Broad protections for both renters and multifamily property owners – as opposed to simple eviction moratoriums – are needed to keep people housed as the COVID-19 crisis continues, according to the National Multifamily Housing Council (NMHC). Only 79.3% of apartment households had made a full or partial rent payment by Aug. 6, according to the NMHC’s Rent Payment Tracker. That’s a 1.9-percentage-point drop year over year. The NMHC’s findings come on the heels of an Apartment List study that found that a record number of homeowners and renters had failed to make a full housing payment for August. “We found that 33% of Americans failed to make their full August housing payments on time, the highest non-payment rate since we began running this survey in April,” Chris Salviati, Apartment List housing economist, said in an email to MPA. Still, the damage has not been as severe as it could have been – but that situation could soon change, according to NMHC Chair David Schwartz. “Over the past few months apartment residents have largely been able to meet their housing obligations. In no small part, this is due to the enhanced unemployment benefits enacted under the CARES Act and significant steps by apartment owners and operators to help their residents,” Schwartz said. “These unemployment benefits that have proven so important to so many households have now lapsed, meaning greater financial distress for millions and the potential worsening of America’s housing affordability crisis.” While the Trump administration recently issued executive orders relating to rental assistance, those orders contain no actual strategy to keep people in their homes, and there are legitimate questions about whether the orders are even constitutional. Schwartz said that rather than relying on questionable executive orders, the administration and Congress need to “reach a comprehensive agreement” on a second COVID-19 relief package. “It is critical lawmakers take urgent action to support and protect apartment residents and property owners through an extension of the benefits as well as targeted rental assistance,” he said. “That support, not a broad-based eviction moratorium, will keep families safely and securely housed as the nation continues to recover from the pandemic.” Salviati agreed, with the caveat that a second stimulus might prove a temporary fix. He and Apartment List study co-authors Igor Popov and Rob Warnock found that a stimulus check of $2,000 would be sufficient to meet the unpaid rent bills of 83% of renters currently behind on their payments, and an additional $1,200 payment would alleviate half the nation’s outstanding housing debt. “That said, a one-time payment does little to alleviate the underlying economic crisis causing this problem, so it is likely that housing debt would again accrue as widespread unemployment continues,” they said.  US consumers' home-purchase sentiment dropped in July after two straight months of increases, as more renters and lower-income households impacted by COVID-19 think now is a bad time to buy a home.

The Fannie Mae Home Purchase Sentiment Index (HPSI) dwindled 2.3 points from June to July, down to a 74.2 reading. The HPSI is also 19.5 points lower than this time a year ago. "Following a partial recovery of the HPSI in the previous two months, consumer sentiment toward housing took a slight step back in July amid a rise in coronavirus infections across many parts of the country, including the south and southwest," said Doug Duncan, senior vice president and chief economist of Fannie Mae. "Supply constraints appear to be applying upward pressure to consumers' home price expectations, which in turn has contributed to both a sharp reversal in optimism about whether it is a good time to buy a home and further improvement in home-selling sentiment." Among the respondent groups, more first-time buyers have reported a significantly more pessimistic outlook on purchasing a home in today's housing market environment, according to Duncan. "The July survey was conducted as legislators considered the extension of several provisions in the CARES Act to support household incomes during the pandemic," he said." Not surprisingly – more than any other respondent groups – renters, 18-to-34-year olds, and households earning less than $100,000 think it's a bad time to buy a home, which we believe suggests a less favorable outlook for first-time homebuying activity." Three of the six HPSI components saw monthly decreases, with more consumers leaning towards better selling conditions.

"In the months ahead, we continue to expect consumer sentiment to be closely linked to the country's progress in containing the spread of the virus," Duncan said.  Congratulations to iMove Chicago- Chicago Association of Realtors Top Producer 2019

|

|

- iMove Chicago

- Real Estate School

-

Laws

-

CRLTO

>

- 5-12-010 Title, Purpose And Scope.

- 5-12-020 Exclusions.

- 5-12-030 Definitions.

- 5-12-040 Tenant Responsibilities.

- 5-12-050 Landlord’s Right Of Access.

- 5-12-060 Remedies For Improper Denial Of Access.

- 5-12-070 Landlord’s Responsibility To Maintain.

- 5-12-080 Security Deposits.

- 5-12-081 Interest Rate On Security Deposits.

- 5-12-082 Interest Rate Notification.

- 5-12-090 Identification Of Owner And Agents.

- 5-12-095 Tenants’ Notification of Foreclosure Action.

- 5-12-100 Notice Of Conditions Affecting Habitability.

- 5-12-110 Tenant Remedies.

- 5-12-120 Subleases.

- 5-12-130 Landlord Remedies.

- 5-12-140 Rental Agreement.

- 5-12-150 Prohibition On Retaliatory Conduct By Landlord.

- 5-12-160 Prohibition On Interruption Of Tenant Occupancy By Landlord.

- 5-12-170 Summary Of Ordinance Attached To Rental Agreement.

- 5-12-180 Attorney’s Fees.

- 5-12-190 Rights And Remedies Under Other Laws.

- 5-12-200 Severability.

- Illinois Eviction Law (Forcible Entry And Detainer)

- Illinois Security Deposit Return Act

-

CRLTO

>

- Today's Cool Thing

- Social Media