The looming overhauls arrive amidst ongoing economic uncertainty.

Major banks are facing one of the biggest regulatory overhauls since the financial crisis, setting up a clash over the amount of capital that they have to set aside to weather tumult. The Federal Reserve’s top banking regulator, Michael Barr, said he wants Wall Street banks to start using a standardized approach for estimating credit, operational and trading risks, rather than relying on their own estimates. He added that the Fed’s annual stress tests should be rejiggered to better capture dangers that firms can face. The changes stem from a months-long review to align US rules with a set of international standards known as Basel III. Industry titans have long fought against higher capital requirements, and the issue became a political lightning rod after several lenders including Silicon Valley Bank collapsed this year. Barr said his examination found that the current system was sound, but several changes were needed that will result in banks setting aside more money as a cushion to protect against losses. The announcement arrived just days before the largest banks begin posting their second-quarter results, starting on Friday with JPMorgan Chase & Co., Citigroup Inc. and Wells Fargo & Co. “These changes would increase capital requirements overall, but I want to emphasize that they would principally raise capital requirements for the largest, most complex banks,” he said in a speech at the Bipartisan Policy Center in Washington. “We intend to consider comments carefully and any changes would be implemented with an appropriate phase-in,” he said, adding that most banks already have enough capital to meet the new requirements. Large Banks Since taking the job last year, Barr has signaled that he generally supports tougher restrictions for bigger, systemically important lenders. Faced with that prospect, large banks sounded a relatively cautious approach for announcing payouts after they all passed the Fed’s annual stress test exam last month. Bank stocks were mostly higher on Monday, with the KBW Bank Index rising 0.2% in New York. Analysts such as Kathleen Shanley at Gimme Credit have questioned the usefulness of the current setup of the Fed’s stress tests because most regional banks were exempted and the scenarios were designed before March’s sudden swoon. Some large regionals have already restrained stock buybacks and dividends in anticipation of new capital minimums, she wrote in a note to clients. “The proposed rules would end the practice of relying on banks’ own individual estimates of their own risk and instead use a more transparent and consistent approach,” Barr said of his plans. The largest banks would also have to hold an extra two percentage points of capital — or an extra $2 of capital for every $100 in risk-weighted assets. “We see this as consistent with our view that the proposed changes will result in modestly higher capital requirements,” Jaret Seiberg, a TD Cowen analyst, wrote in a note to clients. Barr said the changes will only take effect if they’re proposed and approved by the Fed, Federal Deposit Insurance Corp. and the Office of the Comptroller of the Currency. An initial plan could be released as soon as this month, but actual changes would not likely take effect for months or years. Industry will also have a chance to weigh in. He added that “enhanced capital rules” should apply to banks and bank holding companies with more than $100 billion in assets. Currently, such restrictions apply to firms that are globally active or have $700 billion or more in assets, he said. “Setting aside more capital is not about smashing anything. It’s about building resilience in the financial system. It enables banks to lend to the economy,” Barr said during the question-and-answer portion of the event. Industry Pushback The long-awaited Basel III reforms to bank capital levels are part of an international overhaul of capital rules that started more than a decade ago in response to the financial crisis of 2008. The issue became more stark — and political — this year with the collapse of several banks. The top US banks are already subject to higher requirements than their European peers, according to the European Central Bank, which oversees lenders in the euro area. Despite that disadvantage, US securities firms were able to win market share from European competitors in previous years. Tim Adams, head of the Institute of International Finance, said that the planned higher capital standards are “puzzling and counterproductive” because they could harm the economy. “The financial system has proven it is resilient and well-capitalized,” he said in a statement. Barr acknowledged concerns that the changes in capital requirements could lead to banks altering their behavior, as well as the way that financial services are provided. But he said most banks already have sufficient capital today to meet new mandates. As for the rest, he estimates that they would be able to build enough capital through retained earnings in less than two years, “even while maintaining their dividends.” That assumes that they earn money at the same rate as in recent years. Although his review began before this March’s banking crisis, Barr said his plans would deal with some of the issues that were exposed by the collapse of Silicon Valley Bank and others. “Some industry representatives have claimed that SVB’s problems were really related to poor management and shortcomings in the Federal Reserve’s supervision,” Barr said. “It is not logical to argue that failings in supervision must mean that SVB was adequately capitalized — it wasn’t — or that supervision by itself can somehow assure safety and soundness throughout the banking system. It is not a choice between supervision and capital regulation — capital is and has always been the foundation of a bank’s safety and soundness.”

0 Comments

Most respondents continue to have doubts about entering the market.

Homebuying sentiment has plateaued at a relatively low level, suggesting that many consumers may be coming to terms with high mortgage rates and home prices, according to Fannie Mae. The June Home Purchase Sentiment Index (HPSI) posted a slight increase of 0.4 points month over month and 1.2 points year over year to 66, with six of the HPSI components showing little change during the period. HPSI component highlights:

"Additionally, consumers' mortgage rate expectations have tempered: A larger share of respondents think mortgage rates will stay the same over the next year, whereas mid-to-late last year, most thought rates would continue going up. This seems to signal that consumers are adapting to the idea that higher mortgage rates will likely stick around for the foreseeable future. "We continue to forecast home sales to slow in the second half of the year, compared to the first half, due to ongoing affordability constraints and lack of housing supply."  Application activity slows as higher interest rates bites.

Mortgage applications fell to their lowest level in a month as interest rates for most loan types rise, the Mortgage Bankers Association reported today. MBA’s Market Composite Index – a measure of loan application volume – ticked down 4.4% on a seasonally adjusted basis and down 6% when unadjusted. Demand weakened as the average contract interest rate for a 30-year mortgage increased 10 basis points for the week ending June 30. “As mortgage Treasury spreads remained wide, the 30-year fixed rate increased to 6.85%, the highest rate since the end of May,” MBA deputy chief economist Joel Kan said. Kan also noted that purchase applications decreased for the first time in a month, down 5% week over week. Refinance application volume declined by 4% from the previous week. “Rates are still over a percentage point higher than a year ago, and housing affordability is still a challenge in many parts of the country,” Kan added. “However, the average loan size for a purchase application declined to $423,500 – its lowest level since January 2023. This was likely driven by reduced purchase activity in some high-price markets and more activity in some of the lower price tiers as buyers searched for more affordable options.” In a separate report, MBA found that homebuyer affordability worsened in May. The median loan payment applied for by purchase loan applicants was up to $2,165, a 2.5% month-over-month increase and a 14.1% spike from May 2022. For borrowers applying for lower-payment mortgages, the national mortgage payment climbed to $1,462 in May.  Affordability just keeps on eroding.

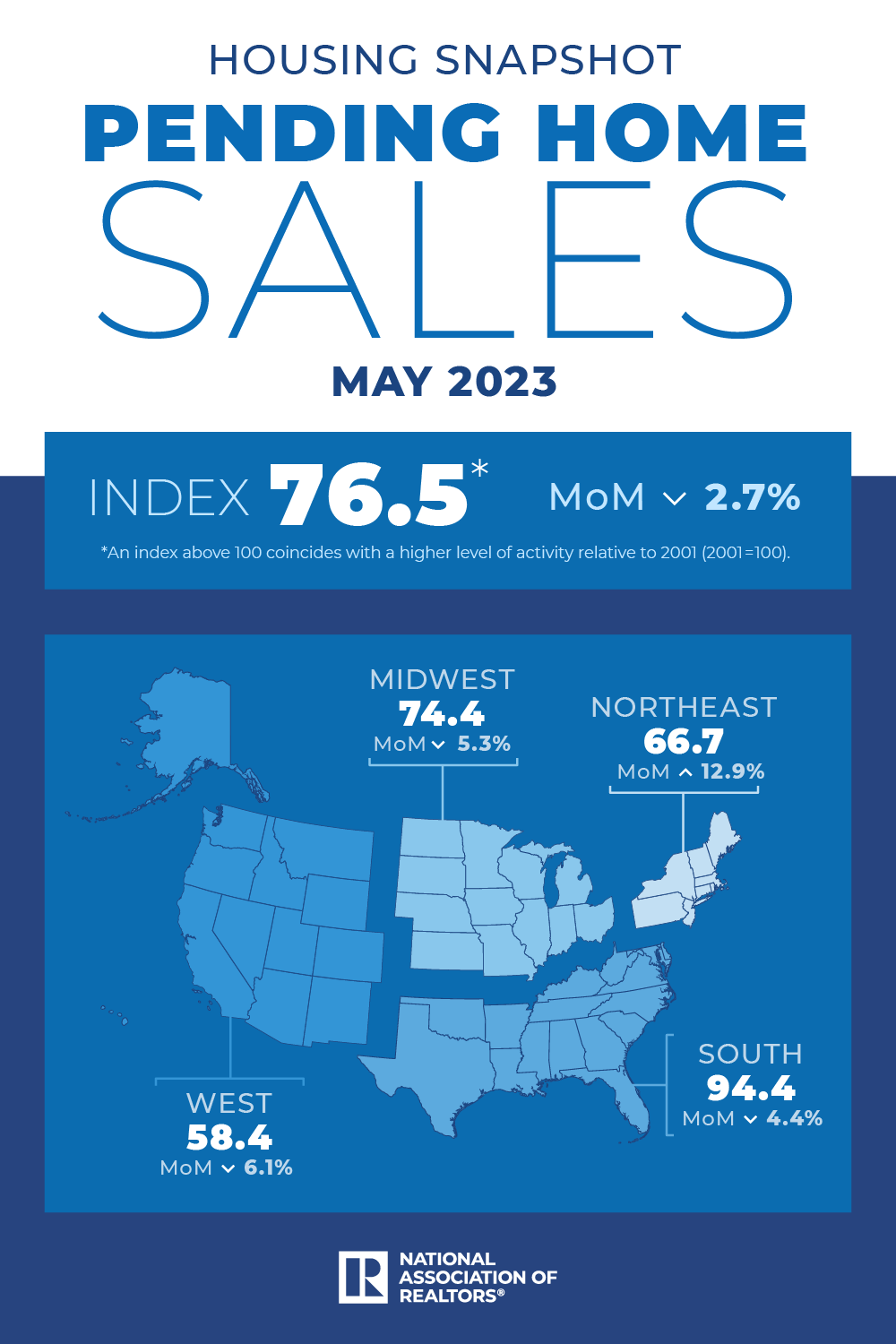

Would-be homebuyers are willing to take on sharply higher mortgage payments, even as home prices have begun to pull back this year. The median monthly payment listed on applications for home purchase loans jumped 14.1% in May from a year earlier to an all-time high $2,165, according to the Mortgage Bankers Association. The May figure also represents a 2.5% increase from April. “Homebuyer affordability eroded further in May as prospective buyers continue to grapple with high interest rates and low housing inventory,” Edward Seiler, the MBA’s associate vice president of housing economics, said in a release last week. The size of the mortgage and the interest rate on the loan influence how large the monthly payment on a 30-year fixed-rate mortgage will be. Those two housing market variables have ballooned in recent years. Home price growth accelerated during the pandemic, fueled by ultra-low mortgage rates and bidding wars as competition for relatively few properties on the market intensified. Even after the market cooled last summer as the Federal Reserve raised interest rates in its bid to slow economic growth and tame inflation, home price appreciation remained resilient until this February, when the median US home price slipped 0.2% from a year earlier -- its first annual decline in 13 years, according to the National Association of Realtors. Home prices have kept falling since, most recently sliding 3.1% in May from a year earlier to a median $396,100, according to the NAR. Still, the national median home price remains nearly 40% higher than it was three years ago. Meanwhile, the average rate on a 30-year home loan climbed to a new high for the year this week at 6.81%, mortgage buyer Freddie Mac said Thursday. That’s more than double what it was two years ago. The combination, along with a stubbornly low level of homes for sale, is driving mortgage payments higher, pushing the limits of what many homebuyers can afford. Consider that two years ago the median national monthly payment on home loan applications was $1,320.48, or 63.4% less than what it was last month. A recent forecast by Realtor.com calls for the average rate on a 30-year mortgage to drop to 6% by the end of the year. Lower rates could motivate some homeowners to sell, adding more sorely needed inventory to the market. However, lower rates could also spur more buyers to come off the sidelines, which would heighten competition and push up prices.  Contract signings remained stalled as buyers wait for new listings in the housing market. Pending home sales remained sluggish in May, hindered by a dearth in housing supply, the National Association of Realtors said Thursday. The pending home sales index fell to 76.5 in May, down 2.7% month over month and 22.2% lower than a year ago, NAR’s latest report revealed. Consensus forecasts expected pending home sales to remain flat. NAR chief economist Lawrence Yun noted that the lack of inventory continued to prevent housing demand from being fully realized.  “It is encouraging that homebuilders have ramped up production, but the supply from new construction takes time and remains insufficient,” Yun said. “There should be more focus on boosting existing-home inventory with temporary tax incentive measures.”

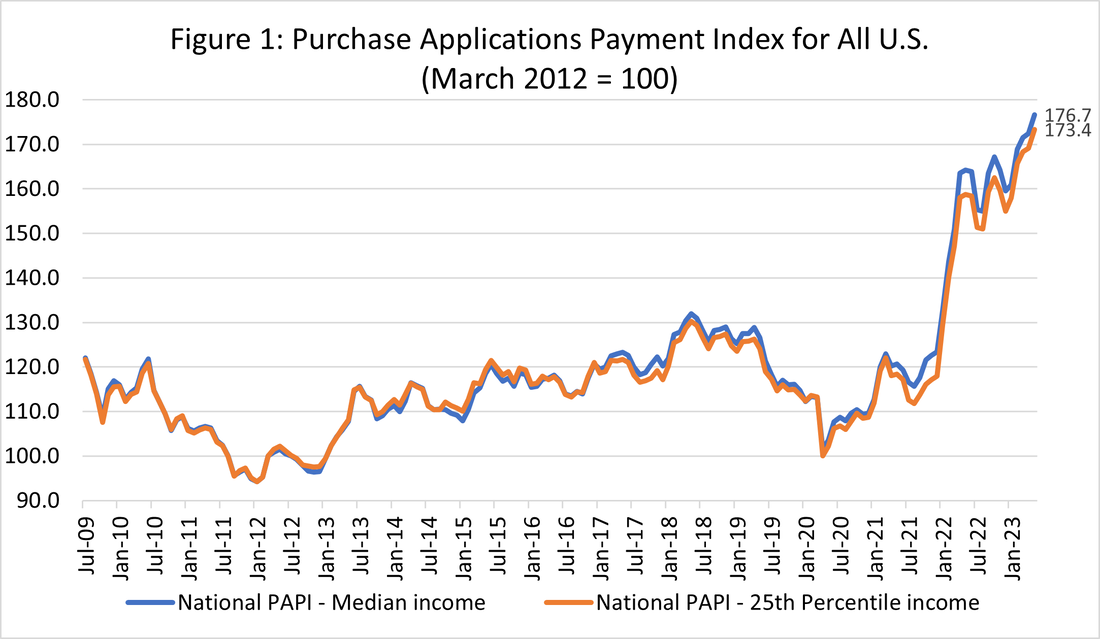

“High hopes that the housing market’s returning to normalcy may be coming down to earth, with May showing a 2.7% decline in pending home sales,” NerdWallet home expert Kate Wood added. “Normally, April to May would see a bump as home buying season really gets underway. One big reason contract signings are stalling? There simply isn’t enough supply. Even as home buyers adjust to the new reality of higher interest rates, their home searches remain stymied by lack of inventory.” Ksenia Potapov, economist at First American Financial, agreed. “The spring home-buying season has struggled to gain momentum. Mortgage rates remain high, reducing house-buying power and keeping existing homeowners rate-locked into their homes. As a result, the inventory of homes for sale, which typically increases throughout the spring and summer months, has remained near winter lows. “The divide between the existing-home and new-home markets continues to grow. While existing-home sales remain muted, multiple leading indicators on the new-home side, including new-home sales, new-home construction, and homebuilder sentiment, have trended higher.” On the bright side, Potapov highlighted that homebuyer demand and the labor market stayed strong, and potential home buyers are ready to jump in. “While limited inventory is likely to hold back sales activity, the housing market remains resilient,” she said.  Homebuyer affordability worsens, but experts find optimism in growing supply. Mortgage borrowers faced more affordability hurdles in May as loan application payments continued to creep higher, according to the Mortgage Bankers Association (MBA). MBA’s Purchase Applications Payment Index (PAPI), a gauge of borrower affordability conditions, hit a new record high of 176.7 in May. The increase indicates a rise in the mortgage payment-to-income ratio (PIR), which occurs when loan application amounts or mortgage rates climb, or earnings decrease.  The PAPI report showed a 2.5% increase in median loan payments applied for by applicants, up to $2,165 from $2,112 in April. It was $268 higher than a year ago, equal to a 14.1% jump.

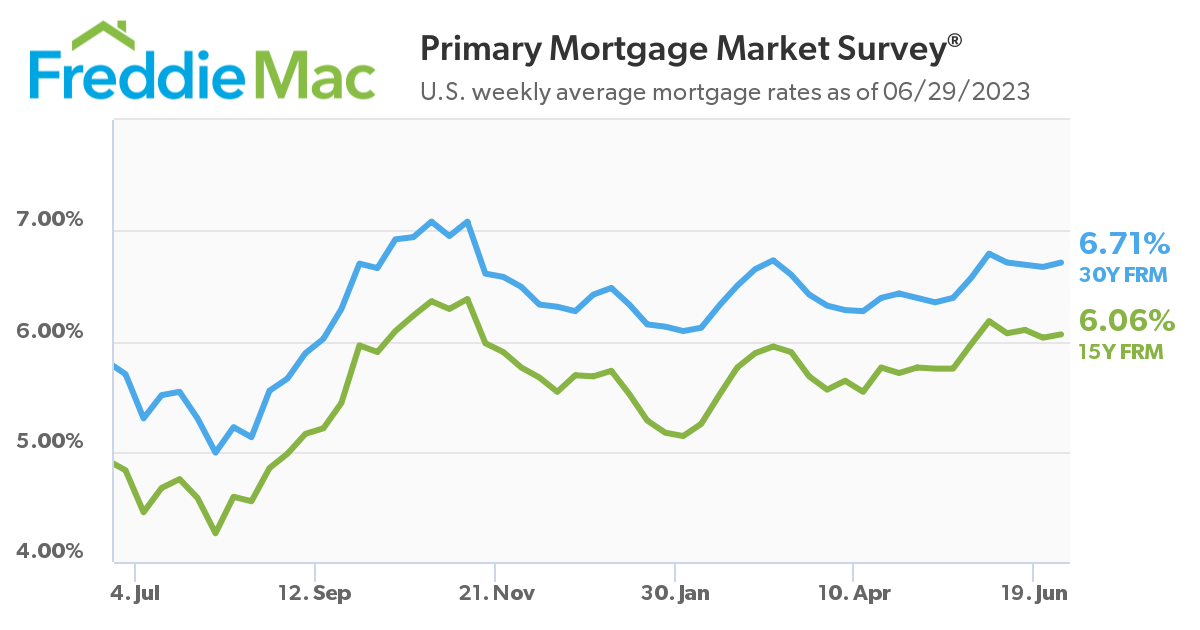

For borrowers applying for lower-payment mortgages, the national mortgage payment increased to $1,462 month over month. “Homebuyer affordability eroded further in May as prospective buyers continue to grapple with high-interest rates and low housing inventory,” said Edward Seiler, associate vice president of housing economics at MBA. “While supply remains low, we do expect that inventory will pick up in the near term, which will provide more opportunities for borrowers to buy a home.” The estimated supply of new homes for sale in May was 428,000, representing a supply of 6.7 months at the current sales pace. Meanwhile, mortgage rates have hovered in the 6-7% range in the first half of the year. Kelly Mangold, principal at RCLCO Real Estate Consulting, commented: “Builder sentiment continues to improve as the number of new homes under construction has increased going into spring and summer homebuying season. Buyer demand remains elevated, and as buyers have begun to prepare for higher payments and adjust expectations, and we are seeing that the market has continued to shift to meet this demand.”  "Homebuyers have adjusted" Freddie Mac has revealed its latest update on long-term mortgage rates, with the benchmark 30-year mortgage rate rising after three weeks of decline. There was a four-basis-point uptick in the 30-year fixed-rate mortgage, which averaged 6.71% as of June 29. The 15-year loan rate inched up three basis points to 6.06% from last week.  affordability headwinds, homebuyers have adjusted and driven new home sales to its highest level in more than a year,” said Freddie Mac chief economist Sam Khater. “New home sales have rebounded more robustly than the resale market due to a marginally greater supply of new construction. The improved demand has led to a firming of prices, which have now increased for several months in a row.”

Mark Fleming, chief economist of First American Financial, believes prices have remained resilient because the relationship between rising mortgage rates and home prices may not be as straightforward as many think. “Even as the Federal Reserve continues to fight inflation with restrictive monetary policy, which will keep upward pressure on mortgage rates, don’t expect house prices to decline dramatically,” Fleming said. “History has shown that higher rates may take the steam out of rising prices, but it doesn’t cause them to collapse entirely. This is especially true in today’s housing market, where the demand for homes continues to outpace supply, keeping the pressure on house prices.”  NAR releases its latest data.

US pending home sales in May fell to the lowest level this year as high mortgage rates and inventory constraints continue to impact sales. The National Association of Realtors’ index of contract signings to purchase previously owned homes dropped 2.7% to 76.5 last month, according to data released Thursday. The decrease was bigger than all but one estimate in a Bloomberg survey of economists. The resale market continues to face headwinds as high borrowing costs and low supply weigh on sales. Many homeowners who locked in lower mortgage rates in the past are reluctant to move, adding to inventory constraints that are pushing many buyers into the new-home market and helping keep existing-home sales subdued. “The lack of housing inventory continues to prevent housing demand from being fully realized,” Lawrence Yun, NAR’s chief economist, said in a statement. “It is encouraging that homebuilders have ramped up production, but the supply from new construction takes time and remains insufficient.” The pending home sales report is often seen as a leading indicator of existing-home sales given homes typically go under contract a month or two before they’re sold. Sales declined in three of four regions, with transactions in the Midwest falling to the lowest level since April 2020. From a year earlier, US home purchases were down nearly 21% on an unadjusted basis.  Uncovering the struggles faced by Americans in achieving homeownership.

According to a survey conducted by Divvy Homes, two out of five Americans believe that winning the lottery is their only chance at becoming homeowners. The survey, conducted among 2,000 current non-homeowners, revealed that only 53% of respondents have any confidence in their ability to own a home in the future. In addition to the 40% who would rely on winning the lottery, 26% feel they would need to inherit money, and 19% believe they would have to marry someone wealthy to reach their dream of homeownership. On average, Americans estimate that it would take them between three to four years to afford a home, while 20% believe that homeownership will never be within their reach. The survey also found that 57% of non-homeowners would struggle to afford a house in their current neighborhood. Despite these challenges, 67% of respondents remain hopeful about the possibility of owning a home, while 12% describe themselves as hopeless, 19% as frustrated, and 11% as desperate. The survey also highlighted the impact of market dynamics and rising interest rates on potential buyers. While 52% perceive the current housing market as unstable, 46% believe it will stabilize within the next two to five years, while 17% think it will never return to a stable and affordable state. Respondents estimate that they would need an average annual income of $76,000 to afford a starter home, with a minimum of $45,000 in savings for the downpayment. The ideal downpayment size, according to respondents, would be 8% of the overall purchase price, making their ideal home worth just under $570,000. To get closer to their homeownership goal, 44% of respondents are willing to take on a second job or side gig. Among those hoping to buy a home in the next few years, affordability of monthly payments (69%), the right size of the home for present and future needs (39%), and an ideal location for their family (37%) are key priorities. However, 56% of respondents believe they would be denied if they applied for a mortgage at present. “Potential buyers are looking for alternatives to traditional mortgage financing or are stuck waiting for a reprieve from the rising rates and prices that keep so many of them renting and locked out of homeownership,” said Adena Hefets, co-founder and CEO of Divvy Homes. “There are so many factors putting downward pressure on a potential homeowner’s buying power - high interest rates, a lack of supply, increasing cost-of-living - that the starter home seems to be on the verge of extinction.” The survey also revealed concerns among renters, with 47% worried about rising home prices before they can afford to buy. Additionally, “throwing money away on rent” (46%), uncertainty about long-term housing stability (41%), and the impact of rising interest rates (34%) were identified as the biggest drawbacks to not owning a home. “The traditional mortgage process was designed in the 1940s when the norm was a single breadwinner with a steady W-2 income. The system hasn’t changed, even though the way we work, live and form families is dramatically different. But today’s younger buyers often lack long periods of income history and are increasingly non-salaried, working as a 1099 contractor, gig worker, or self-employed individual,” Hefets said. “A majority of aspiring homebuyers feel that homeownership is always just beyond their reach, that the ‘American Dream’ of homeownership is slipping away, and that it would take luck, extraordinary circumstances, or a serious change in the mortgage process to make it possible for them to own a home in today’s economic climate.”  People are still deterred from moving.

The number of homes for sale in the US fell to record low levels in May, according to real estate brokerage Redfin Corp., as high mortgage rates continue to deter people from moving. Active listings fell 7.1% on a seasonally adjusted basis in May, and were down 38.6% from pre-pandemic levels, according to Redfin’s Housing Market Tracker. The brokerage said just 1.4 million homes were up for sale in May — lower than any month on its records, which date back to 2012. Many homeowners are opting to stay put as moving means giving up a cheaper mortgage. Rising interest rates pushed the average 30-year-fixed rate to 6.43% in May, Redfin said, up from 5.23% a year earlier, and more than double the 2.65% rate in May 2021. The low number of homes for sale has driven price increases in some markets. Nearly half of Redfin’s offers were met with bidding wars in May, while more than two-thirds of homes sold went for above list price. But new builds could help alleviate those high prices, and the listings scarcity. US housing starts unexpectedly reached their highest level since 2016 in May, according to government data. Existing home sales are set to be announced on Thursday. They likely decreased slightly in May to an annualized pace of 4.25 million, from April’s 4.28 million, according to Bloomberg Economics. |

|

- iMove Chicago

- Real Estate School

-

Laws

-

CRLTO

>

- 5-12-010 Title, Purpose And Scope.

- 5-12-020 Exclusions.

- 5-12-030 Definitions.

- 5-12-040 Tenant Responsibilities.

- 5-12-050 Landlord’s Right Of Access.

- 5-12-060 Remedies For Improper Denial Of Access.

- 5-12-070 Landlord’s Responsibility To Maintain.

- 5-12-080 Security Deposits.

- 5-12-081 Interest Rate On Security Deposits.

- 5-12-082 Interest Rate Notification.

- 5-12-090 Identification Of Owner And Agents.

- 5-12-095 Tenants’ Notification of Foreclosure Action.

- 5-12-100 Notice Of Conditions Affecting Habitability.

- 5-12-110 Tenant Remedies.

- 5-12-120 Subleases.

- 5-12-130 Landlord Remedies.

- 5-12-140 Rental Agreement.

- 5-12-150 Prohibition On Retaliatory Conduct By Landlord.

- 5-12-160 Prohibition On Interruption Of Tenant Occupancy By Landlord.

- 5-12-170 Summary Of Ordinance Attached To Rental Agreement.

- 5-12-180 Attorney’s Fees.

- 5-12-190 Rights And Remedies Under Other Laws.

- 5-12-200 Severability.

- Illinois Eviction Law (Forcible Entry And Detainer)

- Illinois Security Deposit Return Act

-

CRLTO

>

- Today's Cool Thing

- Social Media