Surveyed economists expect credit to crimp by twice as much as Fed chair Powell anticipates.

US bank stress will tighten credit by twice as much as expected by Federal Reserve Chair Jerome Powell, said economists surveyed by Bloomberg, tipping the economy into recession. Almost all of the economists expect the Federal Open Market Committee to hike interest rates another quarter percentage point at its May 2-3 meeting, to a target range of 5% to 5.25%. But the higher borrowing costs will be amplified by the fallout from the March collapse of two US banks, which a majority of the economists found to be equivalent to a Fed hike of about half a percentage point or more. Powell has estimated the impact at roughly a quarter point. “Inflation remains unacceptably high, but banking stresses are leading to a tightening of lending conditions and this will do more to slow the economy than the likely 25 basis-point hike on Wednesday,” said James Knightley, chief international economist at ING, in a survey response. The survey of 46 economists was conducted April 21-26. Fed officials have mostly downplayed the impact on monetary policy from the failures of Silicon Valley Bank and Signature Bank, though they have expressed uncertainly over how evolving credit conditions will affect growth the remainder of the year. In addition to those two failures, First Republic Bank shares plunged this week after encountering huge outflows of deposits. The Fed has made emergency loans to banks and authorities have guaranteed deposits in excess of stated limits to try to stem the crisis. A majority of the economists say the banking woes are mostly over, while another quarter say the crisis is about half over. The resulting credit impact will be significant, the economists found. Almost all of the economists say banks will tighten lending standards, with the biggest impact on commercial real estate loans. A majority see lending standards on real estate loans tightening somewhat and 41% see a considerable impact. Nearly three quarters of the economists expect substantial losses in the office sector. “We expect deposit outflows to continue,” Nomura Securities economists Aichi Amemiya and Jacob Meyer said. “This is likely to be a key cause of reduced bank lending in the coming quarters, which we expect to generate notable economic headwinds.” Views on the impact on monetary policy are diverse, with 43% of the economists estimating it as equivalent to a half-point hike, another 13% seeing it amounting to between a 75 basis-point and 150 basis-point hike, while a quarter agree with Powell in seeing it as a quarter-point impact. The Fed chair, in his press conference in March, emphasized there’s quite a bit of uncertainty about his estimate: “You can think of it as being the equivalent of a rate hike or perhaps more than that; of course, it’s not possible to make that assessment today with any precision whatsoever,” he said. The exact impact may not be easy to calibrate and can be unpredictable, added Julia Coronado, president of MacroPolicy Perspectives LLC and a former Fed economist. “Thinking in terms of rate hike equivalents leads us to think about monetary policy in a dangerously linear way,” she said. “The faster the tightening, the greater the risk of nonlinear financial stability events that can lead to a nonlinear tightening in credit.” The Fed has engaged in the most aggressive interest-rate hiking in 40 years to try to fight persistently high inflation. The upshot: The hiking and the banking crisis will tip the economy into recession within the next 12 months, according to two thirds of the economists. Among those who expect a downturn, four fifths expect it to start in the current quarter or next quarter. “By outsourcing the rest of the fight against inflation to credit tightening by the banks, it has become even more difficult for the Fed to engineer a soft landing,” said Philip Marey, senior US strategist at Rabobank. “Consequently, we think a recession has become more likely.” While FOMC officials haven’t explicitly predicted a recession, the Fed staff at the last meeting forecast a mild recession and policy makers’ forecasts made in March suggest a sharp reduction in growth this year. Half the economists blame the poor oversight on the collapsing banks on the Fed’s supervisory staff and its failure to act promptly in response to institutions’ weaknesses, while a third say the tailoring of regulation by Congress that resulted in lighter supervision of midsized institutions was principally to blame. The Fed plans to release its internal review of the supervision and regulation of failed lender Silicon Valley Bank on Friday at 11 a.m. New York time.

0 Comments

Homeowners are taking a "significant hit" from housing market slowdown.

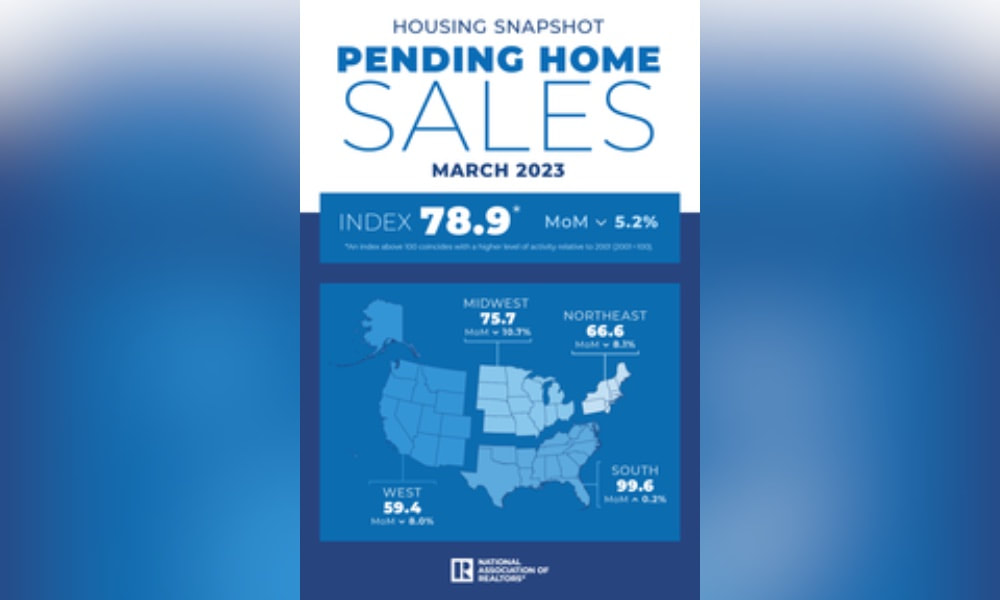

With the benefit of hindsight, millions of US homeowners inclined to sell would have been better off doing it last spring. The average profit margin on the sale of median-priced single-family homes and condos fell to 44% last quarter, from a peak of 56% in the second quarter of 2022, according to data published Thursday by Attom, a real estate analytics firm. The numbers cover homes in metro areas with a population of 200,000 or more. US housing prices have been under pressure as the Federal Reserve jacked up borrowing costs. Benchmark rates for 30-year fixed mortgages have been above 6.5% for most of this year, roughly double what they were at the end of 2021, pushing monthly payments sharply higher. “Homeowners are starting to take a significant hit in the form of lost profits from the recent market slowdown,” said Rob Barber, Attom’s chief executive officer. “Nine months of varying price declines around the country have carved away almost a quarter of the profit margin sellers were enjoying in early 2022. That’s a striking reversal of what we saw for a decade.” Median home prices in the first quarter of 2023 were down from the previous three months, or flat, in 75% of the metro areas analyzed by Attom. Only six of the 139 metro areas saw prices hit a new high. In dollar terms, areas with the most expensive homes are now seeing the biggest profit declines. Sellers of median-priced homes in places like San Francisco, San Diego and Seattle are still posting substantial gains — just not as much as they would’ve gotten last spring. From mid-2008 to early 2014, the typical home seller in a larger US metro area lost money on the sale — with the trough coming in the first quarter of 2009, when the loss reached $46,500, according to Attom data.  "It's not a tremendous surprise". Pending home sales dropped in March, breaking three months of momentum, the National Association of Realtors reported Thursday. NAR's pending home sales index (PHSI), a forward-looking indicator of home sales based on contract signings, fell 5.2% to a 78.9 reading in March. Year over year, pending transactions posted a 23.2% decline.  Kate Wood, home expert at NerdWallet, noted that it's not a tremendous surprise. "Mortgage interest rates rose in March, so it makes sense that fewer buyers signed contracts," she said. "Affordability is already a major challenge due to higher home prices, and every time interest rates increase, the situation gets harder for buyers."

The trade association expects the economy to continue adding jobs, but at a slower pace, and the 30-year mortgage rate will increase to 6% in 2023 and 5.6% in 2024. NAR also forecasts a decline in residential construction, with housing starts falling 7.3% annually this year to 1.44 million units before rising by 6.9% next year to 1.54 million. "The lack of housing inventory is a major constraint to rising sales," said NAR chief economist Lawrence Yun. "Multiple offers are still occurring on about a third of all listings, and 28% of homes are selling above list price. Limited housing supply is simply not meeting demand nationally." With a strong labor market and improving interest rates, NAR anticipates existing-home sales to drop 9.3% from a year ago to 4.56 million before improving by 15.4% in 2024 to 5.26 million units. New home sales will increase 4.5% annually to 670,000 and climb by another 11.9% to 750,000 in 2024. Home prices will also stabilize, according to NAR. The median existing-home price will dip by 1.8% to $379,600 in 2023 and then increase by 2.8% to $390,000 in 2024. New home prices will go down by 1.9% to $449,100, followed by an improvement of 4.2% to $468,000. "Sales in the second half of the year should be notably better than the first half as job gains continue and more favorable mortgage rates are expected," Yun said. "Sales of new homes are already matching 2019 pre-COVID activity and are expected to increase in 2023, largely due to plentiful inventory in this segment of the market."  But Freddie Mac chief economist anticipates rates to "gently decline".

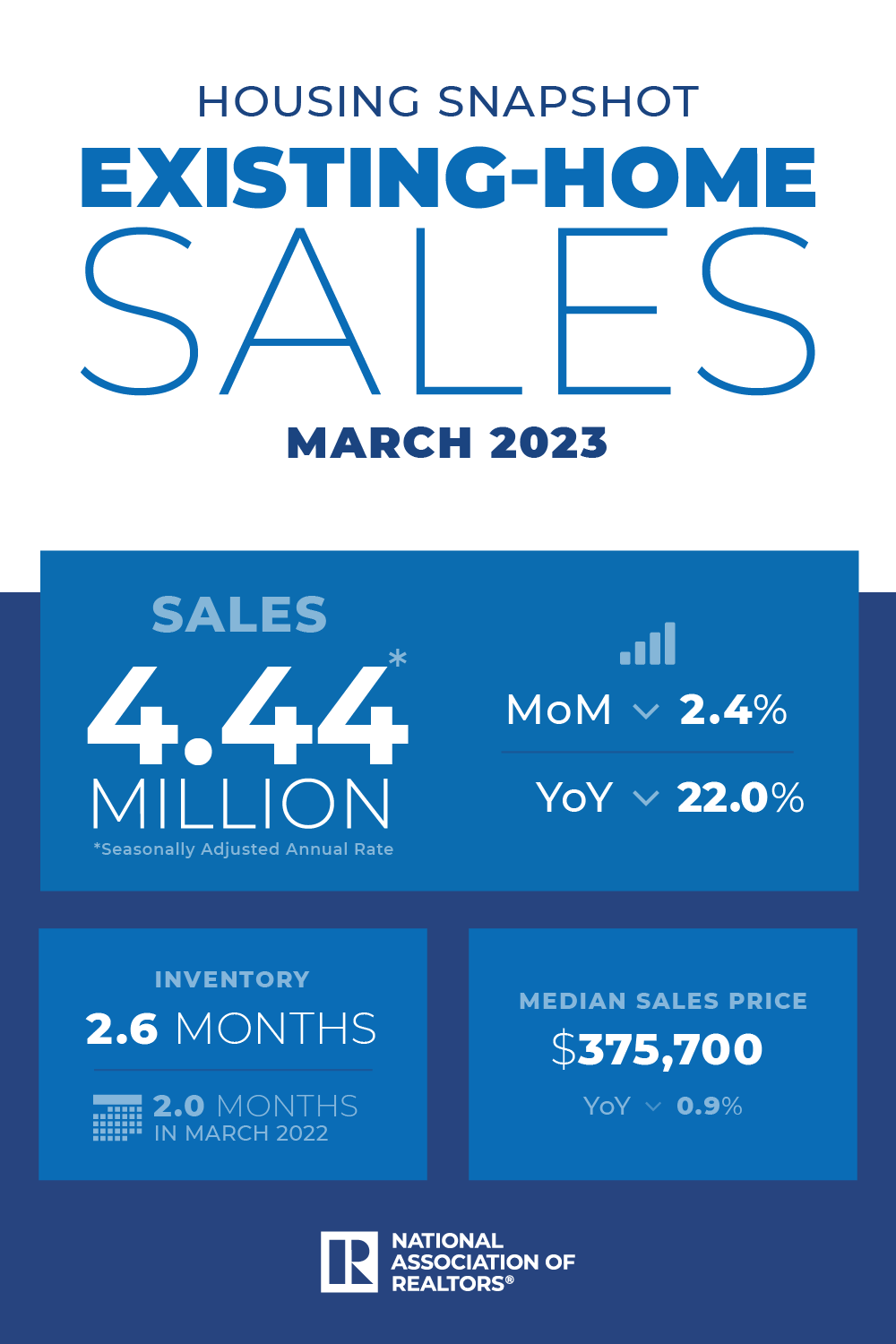

The popular 30-year fixed mortgage rate increased for the second week in a row, but housing industry experts are confident that interest rates will eventually ease this year. Freddie Mac reported Thursday that the average 30-year fixed-rate mortgage rose to 6.43% from 6.39% last week. On the other hand, the 15-year fixed mortgage rate averaged 5.71%, down from 5.76% a week ago. "The 30-year fixed-rate mortgage increased modestly for the second straight week, but with the rate of inflation decelerating, rates should gently decline over the course of 2023," Freddie Mac chief economist Sam Khater said in the company's news release. "Incoming data suggest the housing market has stabilized from a sales and house price perspective. The prospect of lower mortgage rates for the remainder of the year should be welcome news to borrowers who are looking to purchase a home." According to CoreLogic, annual home prices in February posted a 2% annual gain, down from 3.8% in January – marking the 10th consecutive month of decelerating home price growth. "Nevertheless, compared to January, the index posted a first monthly gain in February, after seven months of decline, suggesting that home prices nationally have bottomed out," CoreLogic chief economist Selma Hepp explained. "Even in markets with the largest price drops since last year's peaks, such as San Francisco, home prices picked up pace in February. Still, the housing markets continue to vary across markets and price tiers, but lower mortgage rates and low inventories have been helpful in providing the floor for prices in markets where prices seemed to have nosedived following mortgage rate surge." "The US home buyer remains acutely sensitive to interest rate movements as this latest data point indicates," added Indraneel Karlekar, global head of research and portfolio strategies at Principal Asset Management. "This suggests that the Fed's interest rate tightening is having some impact on consumer behavior." "Although incoming data points to a slowdown in the US economy, markets continue to expect that the Fed will raise short-term rates at its next meeting, which have pushed Treasury yields somewhat higher," said Joel Kan, deputy chief economist of the Mortgage Bankers Association. "As a result of the higher yields, mortgage rates increased for the second straight week to their highest level in over a month, with the 30-year fixed rate now at 6.55%."  Sales of previously owned homes decline in March. Existing-home sales posted a 2.4% month-over-month decline in March as buyers remain sensitive to shifts in mortgage rates. Total existing-home sales waned 2.4% from February to a seasonally adjusted annual rate of 4.44 million in March, the National Association of Realtors reported Thursday. Sales were 22% below last year’s level, down from 5.69 million in March 2022.  NAR chief economist Lawrence Yun noted that home prices continued to rise in regions where jobs are being added, and housing is relatively affordable. “However, the more expensive areas of the country are adjusting to lower prices.”

The median price of previously owned homes slid 0.9% from $379,300 a year ago to $375,700 in March. Meanwhile, housing inventory increased 1% month over month and 5.4% year over year to 980,000 units in March. Unsold inventory remained flat at a 2.6-month supply. “Home sales are trying to recover and are highly sensitive to changes in mortgage rates,” said Yun. “Yet, at the same time, multiple offers on starter homes are quite common, implying more supply is needed to fully satisfy demand. It’s a unique housing market.” After consecutive weeks of decline, the 30-year fixed mortgage rate averaged 6.27% as of April 13. That’s down from 6.28% from the previous week, according to data from Freddie Mac. Holden Lewis, home and mortgage expert at NerdWallet, believes homebuyers are growing accustomed to higher mortgage rates. “Most analysts compare the year-over-year numbers when looking at home sales and prices. But it’s also informative to compare the month-over-month numbers. From February to March, the typical home price went up $12,100. This illustrates that home buyers are satisfying their pent-up demand for homeownership despite a limited number of homes for sale. Furthermore, home buyers are growing accustomed to higher mortgage rates: The average rate on a 30-year mortgage was about one-quarter of a percentage point higher in March than in February, yet home sales rose by 91,000.” “With overall consumer price inflation calming and rents expected to decelerate from robust apartment construction, the Federal Reserve’s monetary policy will surely shift from tightening to neutral to possibly loosening over the next 12 months,” Yun added. “Therefore, home sales will steadily rebound despite several months of fluctuations.”  Demand takes another blow.

US mortgage rates increased last week by the most in two months to 6.43%, denting already sluggish demand. The contract rate on a 30-year fixed mortgage rose 13 basis points, abruptly ending a five-week slide in borrowing costs, Mortgage Bankers Association data showed Wednesday. The group’s index of mortgage applications for home purchases dropped 10% in the week ended April 14, the steepest decline in two months. High borrowing costs — now even higher — have not only stifled buyer activity over the past year but also discouraged many Americans from listing their homes in the first place, straining inventory and further limiting sales. With the Federal Reserve set on taming inflation, and potentially raising interest rates even higher, it’s not clear when the housing market will manage to regain momentum. The MBA’s index of refinancing applications also declined to the lowest level since early March. The MBA survey, which has been conducted weekly since 1990, uses responses from mortgage bankers, commercial banks and thrifts. The data cover more than 75% of all retail residential mortgage applications in the US.  Big default shows loan pressures as rates rise.

A recent foreclosure of four Houston apartment complexes highlights the impact of rising interest rates on the multitrillion-dollar rental-housing market. Applesway Investment Group, which borrowed nearly $230 million to acquire the buildings during the pandemic, defaulted on its loans, leading Arbor Realty Trust to foreclose on the properties. New York-based Fundamental Partners purchased the Houston properties for an undisclosed sum. Arbor Realty Trust is a listed specialist multifamily and commercial direct lender based in Uniondale, NY. With a portfolio of around $28 billion, it earns around $115 million a year, and saw nearly $11 billion in originations last year, a drop from its 2021 numbers. With a structured loan book that is 97% floating rate, its clients will be suffering as rates have jumped over the last year. The turbulence in commercial real estate is now affecting rental apartments, beyond urban offices and older shopping centers. The multifamily sector has been viewed as a relatively safe investment, particularly due to increased home prices during the pandemic that pushed many potential buyers to continue renting. Landlords have enjoyed rising apartment rents and affordable debt, driving property values to record levels. However, the recent uptick in interest rates has dampened the apartment sector's appeal. Property values have declined by more than 20%, according to Green Street, a real estate analytics firm, and rent growth is decelerating. As a result, some buildings with significant floating-rate mortgages no longer generate sufficient profits to cover debt payments. Applesway's experience serves as a warning for commercial property investors who sought substantial returns by purchasing modestly-priced buildings and increasing rents following renovations. As interest rates rise and hedging contracts expire, foreclosures like Applesway's could become increasingly common. Trepp data shows that a record $151.8 billion in US mortgages backed by rental apartment buildings will mature this year, with $940.1 billion set to expire over the next five years.  Despite strong performance, commercial and multifamily volume drops annually.

Commercial real estate (CRE) mortgage originations totaled $816 billion in 2022, the second-highest level on record. While borrowing and lending activity remained strong last year, commercial loan volume was down 8% from the all-time high of $891 billion in 2021, according to the Mortgage Bankers Association (MBA). Compared to 2020, CRE origination volume was up 33% from $614 billion. “Borrowing and lending backed by commercial and multifamily properties started 2022 strong but then dropped off because of rising interest rates, uncertainty about property values, and increased questions about the economy and some property fundamentals,” said Jamie Woodwell, head of commercial real estate research. “Despite the 8% annual decline, the $816 billion total volume was still the second highest on record. Bank lending ran against the trend, increasing by 12% to $409 billion.” Commercial and multifamily mortgage bankers – excluding activity from smaller and mid-sized depositories not directly captured in MBA’s survey – financed $595 billion of loans in 2022. That’s 13% less than the $683.2 billion reported last year. Multifamily properties posted the highest volume last year at $437 billion of the total lending figure and $333 billion of mortgage bankers’ originations. First liens comprised 93% of the mortgage bankers’ dollar volume closed. Among capital sources, depositories were the largest funder, accounting for $408 billion of total commercial and multifamily lending in 2022 and $189 billion of mortgage bankers’ originations. Government-sponsored enterprises Fannie Mae and Freddie Mac were the second-highest with a total volume of $128 billion, followed by life insurance company and pension funds, private label CMBS, and investor-driven lenders. “A key question for 2023 is when the market will have stabilized enough for the logjam in new deal activity to break,” Woodwell said.  Demand has held up across the country, report says.

Multifamily rents climbed month over month in March as strong demand offset economic challenges, data from Yardi Matrix’s latest National Multifamily report showed. The average asking rent increased by $3 last month to $1,706. However, national rent growth declined to 4% annually – the lowest level since rents started an unprecedented rise in April 2021. “The first quarter produced no gains for multifamily rents for the first time in a decade, but the results come as somewhat of a relief,” Yardi Matrix experts wrote in the report. “Multifamily demand held up well despite the attention given to the Federal Reserve-induced economic slowdown, bank failures, and the deceleration from the outsize rent gains of the last two years. Rents and occupancy are stable as the market heads into the growth season.” Single-family rent growth rose to $2,079 in March, a $5 gain from the previous month. Year over year, single-family rental rates plunged by 80 basis points to 2.8%. The national occupancy rate was virtually flat during the first quarter, down 10 basis points to 95.1% in March. “With affordability a growing concern and consumers constrained by high inflation, it is likely that rent growth in 2023 will be modest,” Yardi said. “Yet a multifamily hard landing is not yet in the cards, since household formation is still boosted by the tight job market, high single-family home prices, and mortgage rates are keeping homeownership out of reach for some renters, and consumer balance sheets remain strong (for now). The big question continues to be how the economy will react to sharp interest rate increases.”  Rise was spurred by an increase in the balance of delinquent office property loans.

Commercial/multifamily delinquency rates rose for the second quarter in a row, according to the Mortgage Bankers Association’s latest commercial real estate finance (CREF) survey. The balance of commercial and multifamily mortgages that were current dropped from 98% to 97.8% through the first quarter. “The rise was led by a 110-basis-point increase in the share of office loan balances that are 30 days or more past due,” said Jamie Woodwell, head of commercial real estate research at MBA. “At the same time, pandemic-fueled delinquency rates for retail and hotel loans continued to tick down.” About 1.7% of commercial/multifamily properties were 90+ days delinquent or in REO in Q1, up from 1.6% in Q4. Mortgages that were 60-90 days delinquent grew from 0.1% to 0.2% quarter over quarter, while those that were 30-60 days delinquent remained unchanged at 0.3%. The survey showed that loans backed by lodging and retail properties continued to see the greatest stress. However, both saw declines in delinquency rates, with the balance of lodging loans that were 30 days or more delinquent down five basis points to 5.6%, and delinquent retail loans decreased eight basis points to 4.6%. “Higher and volatile interest rates, coupled with uncertainty about property values and some property fundamentals, are suppressing sales transaction and mortgage origination volumes,” Woodwell said. “Some loans maturing into these conditions are likely to face increased frictions, which is likely to push further on delinquency rates in coming quarters.” Other key findings of the CREF survey include:

|

|

- iMove Chicago

- Real Estate School

-

Laws

-

CRLTO

>

- 5-12-010 Title, Purpose And Scope.

- 5-12-020 Exclusions.

- 5-12-030 Definitions.

- 5-12-040 Tenant Responsibilities.

- 5-12-050 Landlord’s Right Of Access.

- 5-12-060 Remedies For Improper Denial Of Access.

- 5-12-070 Landlord’s Responsibility To Maintain.

- 5-12-080 Security Deposits.

- 5-12-081 Interest Rate On Security Deposits.

- 5-12-082 Interest Rate Notification.

- 5-12-090 Identification Of Owner And Agents.

- 5-12-095 Tenants’ Notification of Foreclosure Action.

- 5-12-100 Notice Of Conditions Affecting Habitability.

- 5-12-110 Tenant Remedies.

- 5-12-120 Subleases.

- 5-12-130 Landlord Remedies.

- 5-12-140 Rental Agreement.

- 5-12-150 Prohibition On Retaliatory Conduct By Landlord.

- 5-12-160 Prohibition On Interruption Of Tenant Occupancy By Landlord.

- 5-12-170 Summary Of Ordinance Attached To Rental Agreement.

- 5-12-180 Attorney’s Fees.

- 5-12-190 Rights And Remedies Under Other Laws.

- 5-12-200 Severability.

- Illinois Eviction Law (Forcible Entry And Detainer)

- Illinois Security Deposit Return Act

-

CRLTO

>

- Today's Cool Thing

- Social Media