Applications drop to one-month low.

Mortgage demand from homebuyers dwindled for the week ending July 21 as borrowers backed off amid a housing market that remains unaffordable for many. The Market Composite Index – a measure of mortgage application volume – was down 1.8% on a seasonally adjusted basis from a week ago, the Mortgage Bankers Association said today. When unadjusted, the index was down 1.5% compared with the previous week. “Mortgage rates were essentially flat last week but remained high, with the 30-year fixed staying at 6.87% and contributing to a pullback in mortgage applications,” said Joel Kan, MBA’s deputy chief economist. MBA’s refinance index slipped 0.4% from the prior week. The seasonally adjusted purchase index fell 3% to its lowest level in over a month. Kan said the decline in purchase activity was partly driven by a 10% decrease in FHA applications, which decreased nine basis points to 12.7%. “The decrease in FHA purchase applications contributed to an increase in the overall average purchase loan size to $432,700, its highest level since the end of this May,” he added. “Refinance applications remained lackluster, running 30% behind year-ago levels. Many borrowers remain on the sidelines given current rates and persistent affordability challenges.”

0 Comments

They surpass the usual real estate laggards.

About $24.8 billion of US office buildings were in distress at the end of the second quarter, surpassing previous leading commercial real estate laggards — hotels and retail properties. The total value of offices that were financially troubled or already repossessed by lenders shot up about 36% from the first quarter, MSCI Real Assets reported Wednesday. At the end of June, $22.7 billion of retail properties — including malls — and $13.5 billion of hotels were in distress. The total for all troubled commercial properties was almost $72 billion, up 13% from the first quarter. “The office sector was responsible for the largest share of marketwide distress,” according to the report, based on filings for bankruptcies, defaults and other publicly reported property issues. “It’s the first time since 2018 that neither the retail nor hotel sector was the biggest contributor.” It’s likely to get worse for offices. “The things needed to slow the pace aren’t happening,” Jim Costello, an MSCI economist and a co-author of the report, said in an interview. “Investors are putting a low probability on debt becoming cheap and everybody being back in the office like they were before.” MSCI identified an additional $162 billion of properties in potential distress, with problems such as delinquent loan payments, high vacancies or maturing debt. US offices face higher stress than other real estate sectors because of weak demand as remote work gains widespread acceptance. Office use in 10 major US cities is at about half of its pre-pandemic rate on average, according to badge-swipe data from Kastle Systems Inc. More than 20% of US office space was vacant as of June 30, brokerage Jones Lang LaSalle Inc. reported. Prices for office buildings fell 27% in the year through June, compared with a 12% decline for all commercial-property types, according to real estate analytics firm Green Street. Corporate landlords such as Blackstone Inc., Brookfield Asset Management Ltd. and Starwood Capital Group have stopped payments on office buildings they’ve deemed to be money losers. Office properties with maturing debt are among the most vulnerable to stress because the cost of borrowing has soared since the Federal Reserve started raising interest rates last year to try to cool inflation. About $189 billion of debt on office buildings is estimated to mature in 2023 with an additional $117 billion due in 2024, according to the Mortgage Bankers Association.  Elevated mortgage rates and affordability issues could throttle builder momentum, experts say.

US housing starts slowed in June as higher mortgage rates continued to make it harder for eager homebuyers to purchase and for builders to meet pent-up demand. New residential construction came in below expectations at a seasonally adjusted annual rate of 1.43 million, 8% below the downward revised May estimate of 1.56 million, the Census Bureau said Wednesday. Within this figure, single-family production declined after four straight monthly gains, down 7% month over month to a 935,000 rate. Multifamily starts also declined in June, down 9.9% to an annualized 482,000 pace. Overall permits fell 3.7% to a seasonally adjusted annual rate of 1.44 million, with single-family authorizations coming in at 922,000 (+2.2%) and multifamily permits at 467,000 (-12.8%). Builders completed 1.47 million units in June – 3.3% below the annualized revised May estimate of 1.52 million. Single‐family housing completions were 986,000, while the rate for units in buildings with five units or more was 476,000. Despite the lower June reading, several factors paint a promising picture for overall construction activity, according to NerdWallet home expert Holden Lewis. “Homebuilders started construction on fewer dwellings in June than in May,” Lewis said. “Looking at the bigger picture, construction activity is strong. We’ve seen a two-month surge in construction of single-family houses, which are in short supply. At the same time, builders are breaking ground on fewer apartments.” Kelly Mangold, principal at RCLCO Real Estate Consulting, highlighted a more positive builder sentiment, which inched higher in July to the highest level since June 2022. “There are many factors that point towards the housing market moving into recovery as builder sentiment continues to improve,” she said. “Builders are benefitting from the lack of resale inventory, but higher mortgage rates pose a threat. Reduced affordability alongside ongoing supply-side challenges and tighter lending standards for acquisition, development and construction (AD&C) loans could throttle builder momentum.” Danushka Nanayakkara-Skillington, NAHB’s assistant vice president for forecasting and analysis, added that a projected easing in mortgage rates later this year can help improve affordability issues. “We anticipate mortgage rates will stabilize later this year in anticipation of the end of Federal Reserve’s tightening cycle,” Nanayakkara-Skillington said. “In turn, this could bring home buyers back to the market as affordability conditions improve.”  High mortgage rates are causing homeowners to stay in place.

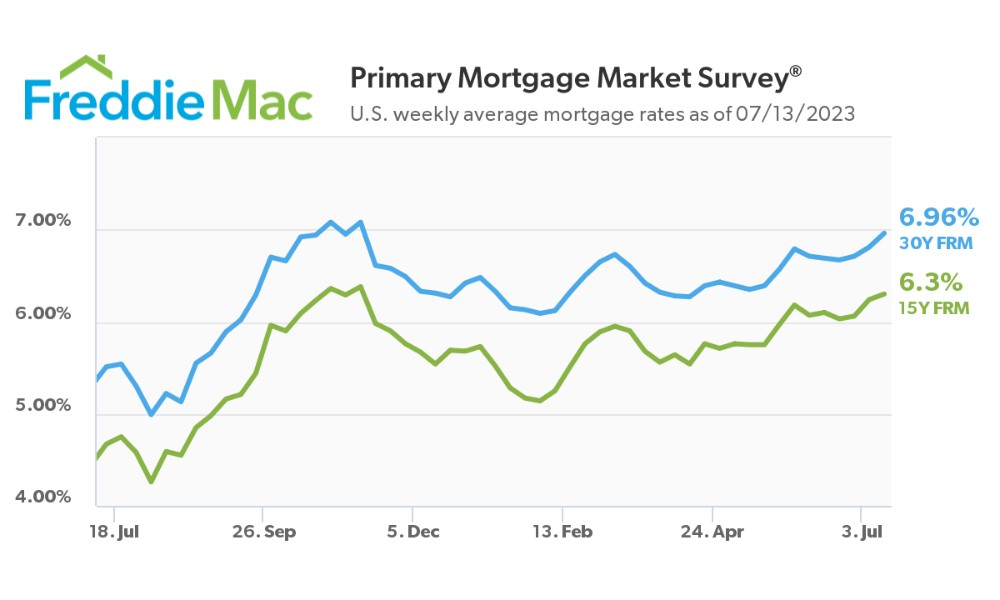

The US home turnover rate in the first half of 2023 has fallen to the lowest in at least a decade as high mortgage rates compel owners to stay put, Redfin Corp. said. About 14 out of every 1,000 US homes changed hands during this period, down from 19 in the same period during 2019, according to the real estate brokerage’s report examining housing turnover since the pandemic. California, and specifically the San Francisco Bay Area, had the least housing availability out of any state, the report said. The brokerage said only 6 out of 1,000 San Jose homes changed hands this year. From 2019 to 2023, California turnover dropped 30% in the metros of Oakland, San Diego, Los Angeles, Sacramento and Anaheim. “The quick increase in mortgage rates created an uphill battle for many Americans who want to buy a home by locking up inventory and making the homes that do hit the market too expensive,” Redfin Deputy Chief Economist Taylor Marr said in a statement. The highest turnover rate was in Newark, New Jersey, with 24 of every 1,000 homes changing hands. Nashville and Austin follow closely behind. Redfin’s report examined turnover rates in the 50 most populous metropolitan divisions in the US. The analysis was based on data, county records and the Department of Housing and Urban Development’s urbanization perceptions small area index.  The benchmark 30-year home loan rate climbs near 7%. The average 30-year mortgage rate hit its highest level since November 2022, the last time it broke 7%, according to Freddie Mac. Freddie Mac reported Thursday that the 30-year fixed-rate mortgage spiked 15 basis points to 6.96%, while the 15-year loan posted a six-basis-point increase to 6.30%.  “Incoming data suggest that inflation is softening, falling to its lowest annual rate in more than two years,” Freddie Mac chief economist Sam Khater said. “However, increases in housing costs, which account for a large share of inflation, remain stubbornly high, mainly due to low inventory relative to demand.”

Erin Sykes, chief economist at Nest Seekers International, commented: “The 30-year mortgage has hovered right around 7% for about nine months despite the Fed continuing to hike rates. My expectation is that it stays there for the foreseeable future with minor fluctuations higher/lower. This is in line with the 50-year average of 7.77%.” “The Fed understands that fighting inflation is a bit like fighting a fire,” added Marty Green, principal at mortgage law firm Polunsky Beitel Green. “Just because the flames have calmed down, for now, doesn’t mean the ingredients for a flare-up aren’t still there. But the continued progress on the inflation front should relieve the pressure on the Federal Reserve to tighten interest rates further after the July increase, which should, in turn, have a positive impact on mortgage rates.”  New report shows why those all-important numbers are slipping for some.

Credit reporting company TransUnion has just released a report with a dull title “Score Migration Impact to the Credit Ecosystem,” but some interesting observations – it appears that we are seeing a nationwide drop in credit scores. The study reveals that although clients’ credit scores experienced a significant boost during the initial stages of the COVID-19 pandemic, thanks to government assistance programs, reduced credit usage, and forbearance options for loan payments, some of those consumers who transitioned to higher credit score ranges are now facing higher delinquency rates compared to historical data for those risk tiers. The rise in credit scores can be attributed to two key factors. Firstly, individuals benefited from lower credit balances and utilization due to reduced spending during the lockdown and surplus funds provided by government assistance. Secondly, lower delinquencies were observed as a result of payment forbearance programs and increased liquidity, allowing consumers to stay current on their payments. During the pandemic, with many activities and travel plans put on hold, consumers utilized their savings, along with additional relief funds from the government, to pay off their credit balances. This led to decreased balances, making it easier for consumers to stay up to date with their payments and resulting in lower delinquency rates. Consequently, credit scores improved, granting individuals greater access to credit. Median credit scores experienced a significant surge during the pandemic and have remained elevated since then. However, as government assistance programs came to an end and inflation started to rise in mid-2021, consumer demand for credit increased. Products such as credit cards and personal loans, which offer immediate liquidity, saw particularly high demand. Lenders also became more willing to provide these credit products, leading to a 58.8% increase in credit card originations and a 54.3% increase in unsecured personal loan originations in 2022 compared to the previous year. The study also highlighted a concerning trend among borrowers who had recently transitioned to a higher credit risk range. Many of these borrowers began reverting to their previous credit behaviors, resulting in delinquency rates similar to those with lower credit scores prior to the pandemic. For instance, the delinquency rate of a sub-segment of new unsecured personal loan borrowers in Q3 2021, who had recently migrated to a higher credit score, resembled the delinquency rates of borrowers with credit scores 25 points lower before the pandemic. Michele Raneri, the vice president and head of US research and consulting at TransUnion, emphasized the importance of lenders taking a comprehensive approach to assessing credit score migrators. By analyzing additional trended credit behaviors, lenders can better identify borrowers who are likely to maintain their improved credit positions and those who may perform more in line with their prior score levels. Raneri stated: “Credit scores continue to perform extremely well at their intended role of rank ordering borrower risk. That said, the temporary benefits brought on by pandemic-era government relief programs, and resulting consumer credit behaviors during that time, led to a rise in scores for many consumers, particularly those who previously had lower scores due to delinquent accounts and/or high credit utilization.” So what effect did a rising tide of credit scores have? While clients might have been pleased to see their numbers climb, as the saying goes, “a rising tide floats all boats” and a universal hike in credit scores means that, well, that increased score just ain’t what it used to be. TransUnion’s figures show that a 625 post pandemic is ‘worth’ a pre-pandemic 600 for bankcard and UPL. Looking at auto? 610 now is ‘worth’ a pre-COVID 600.  They are edging closer to levels not seen for decades.

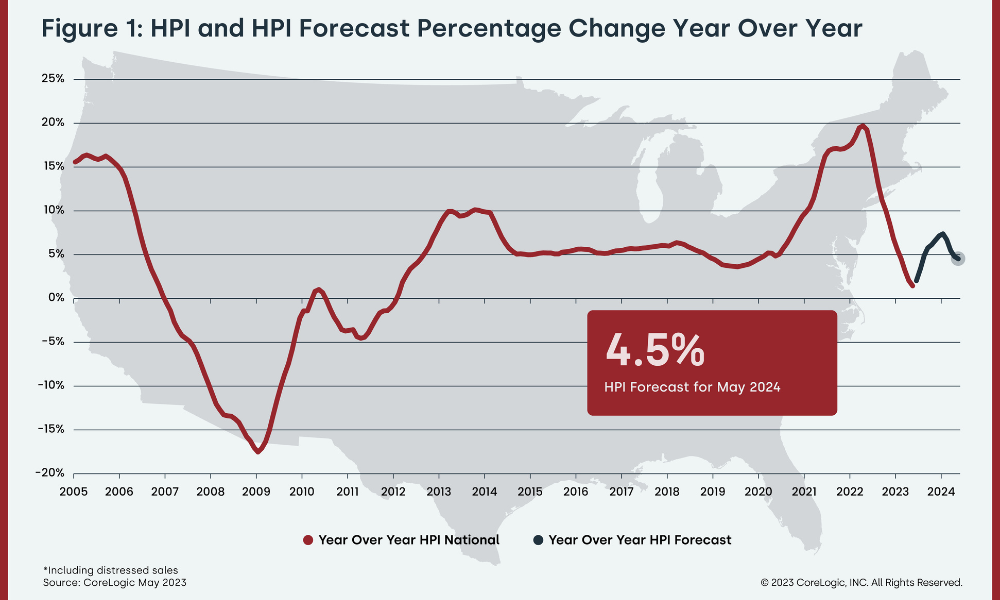

US mortgage rates rose last week to the highest since November, edging close to levels last seen more than two decades ago. The contract rate on a 30-year fixed mortgage increased 22 basis points to 7.07% in the week ended July 7, according to Mortgage Bankers Association data out Wednesday. The weekly jump during the period that included the Fourth of July holiday was also among the biggest since late last year. Treasuries sold off last week after a slew of reports showed the labor market, while cooling somewhat, remains largely resilient, bolstering bets that the Federal Reserve will resume raising interest rates this month. Wednesday’s release of the June consumer price index will likely solidify those expectations, meaning mortgage rates risk rising further along with other borrowing costs. The MBA’s index of refinancing applications declined a seasonally adjusted 1.3% from the prior week. However, the home-purchase gauge rose, contributing to an advance in the overall measure of mortgage applications. The survey, which has been conducted weekly since 1990, uses responses from mortgage bankers, commercial banks and thrifts. The data cover more than 75% of all retail residential mortgage applications in the US.  Several states even recorded annual home price losses. CoreLogic’s Home Price Index fell for the 12th consecutive month in May as rising mortgage rates continue to deter aspiring homebuyers. Single-family home price growth slowed to a 1.4% year-over-year pace in May, according to CoreLogic, but appreciation remained positive for the 136th straight month. The last time the index saw annual growth decline to less than 2% was 11 years ago.  “After peaking in the spring of 2022, annual home price deceleration continued in May,” CoreLogic chief economist Selma Hepp said. “Despite slowing year-over-year price growth, the recent momentum in monthly price gains continues in the face of recent mortgage rate increases.”

The annual price growth of attached properties (2.7%) was 1.7 percentage points higher than that of detached properties (1%). CoreLogic’s HPI Forecast showed annual home price gains bouncing back to 4.5% by May 2024. “Nevertheless, following a cumulative increase of almost 4% in home prices between February and April of 2023, elevated mortgage rates and high home prices are putting pressure on potential buyers,” Hepp added. “These dynamics are cooling recent month-over-month home price growth, which began to taper and is returning to the pre-pandemic average, with a 0.9% increase from April to May.” Among states, Maine posted the highest annual home price gain in May (+7.2%), followed by New Jersey (+7.1%) and Indiana (+6.9%). Meanwhile, 11 states and one district recorded annual home price losses: Idaho (-8%), Washington (-7.5%), Nevada (-5.6%), Montana (-5.3%), Utah (-4.3%), Arizona (-4.2%), California (-3.5%), Oregon (-3.1%), Colorado (-2.7%), South Dakota (-1.3%), New York (-0.3%) and the District of Columbia (-0.1%). “Following recent trends, a significant number of Western states saw prices decline in May from the same time in 2022, reflecting out-migration from less-urban locations where people moved during the height of the pandemic and the significant loss of affordability due to those resulting home price surges,” CoreLogic explained in its report. “Northeastern states and Southeastern metro areas continue to see larger home price gains compared with other areas of the country, due to both workers slowly moving back to job centers in some areas of the country and settling in relatively affordable places in others.”  The looming overhauls arrive amidst ongoing economic uncertainty.

Major banks are facing one of the biggest regulatory overhauls since the financial crisis, setting up a clash over the amount of capital that they have to set aside to weather tumult. The Federal Reserve’s top banking regulator, Michael Barr, said he wants Wall Street banks to start using a standardized approach for estimating credit, operational and trading risks, rather than relying on their own estimates. He added that the Fed’s annual stress tests should be rejiggered to better capture dangers that firms can face. The changes stem from a months-long review to align US rules with a set of international standards known as Basel III. Industry titans have long fought against higher capital requirements, and the issue became a political lightning rod after several lenders including Silicon Valley Bank collapsed this year. Barr said his examination found that the current system was sound, but several changes were needed that will result in banks setting aside more money as a cushion to protect against losses. The announcement arrived just days before the largest banks begin posting their second-quarter results, starting on Friday with JPMorgan Chase & Co., Citigroup Inc. and Wells Fargo & Co. “These changes would increase capital requirements overall, but I want to emphasize that they would principally raise capital requirements for the largest, most complex banks,” he said in a speech at the Bipartisan Policy Center in Washington. “We intend to consider comments carefully and any changes would be implemented with an appropriate phase-in,” he said, adding that most banks already have enough capital to meet the new requirements. Large Banks Since taking the job last year, Barr has signaled that he generally supports tougher restrictions for bigger, systemically important lenders. Faced with that prospect, large banks sounded a relatively cautious approach for announcing payouts after they all passed the Fed’s annual stress test exam last month. Bank stocks were mostly higher on Monday, with the KBW Bank Index rising 0.2% in New York. Analysts such as Kathleen Shanley at Gimme Credit have questioned the usefulness of the current setup of the Fed’s stress tests because most regional banks were exempted and the scenarios were designed before March’s sudden swoon. Some large regionals have already restrained stock buybacks and dividends in anticipation of new capital minimums, she wrote in a note to clients. “The proposed rules would end the practice of relying on banks’ own individual estimates of their own risk and instead use a more transparent and consistent approach,” Barr said of his plans. The largest banks would also have to hold an extra two percentage points of capital — or an extra $2 of capital for every $100 in risk-weighted assets. “We see this as consistent with our view that the proposed changes will result in modestly higher capital requirements,” Jaret Seiberg, a TD Cowen analyst, wrote in a note to clients. Barr said the changes will only take effect if they’re proposed and approved by the Fed, Federal Deposit Insurance Corp. and the Office of the Comptroller of the Currency. An initial plan could be released as soon as this month, but actual changes would not likely take effect for months or years. Industry will also have a chance to weigh in. He added that “enhanced capital rules” should apply to banks and bank holding companies with more than $100 billion in assets. Currently, such restrictions apply to firms that are globally active or have $700 billion or more in assets, he said. “Setting aside more capital is not about smashing anything. It’s about building resilience in the financial system. It enables banks to lend to the economy,” Barr said during the question-and-answer portion of the event. Industry Pushback The long-awaited Basel III reforms to bank capital levels are part of an international overhaul of capital rules that started more than a decade ago in response to the financial crisis of 2008. The issue became more stark — and political — this year with the collapse of several banks. The top US banks are already subject to higher requirements than their European peers, according to the European Central Bank, which oversees lenders in the euro area. Despite that disadvantage, US securities firms were able to win market share from European competitors in previous years. Tim Adams, head of the Institute of International Finance, said that the planned higher capital standards are “puzzling and counterproductive” because they could harm the economy. “The financial system has proven it is resilient and well-capitalized,” he said in a statement. Barr acknowledged concerns that the changes in capital requirements could lead to banks altering their behavior, as well as the way that financial services are provided. But he said most banks already have sufficient capital today to meet new mandates. As for the rest, he estimates that they would be able to build enough capital through retained earnings in less than two years, “even while maintaining their dividends.” That assumes that they earn money at the same rate as in recent years. Although his review began before this March’s banking crisis, Barr said his plans would deal with some of the issues that were exposed by the collapse of Silicon Valley Bank and others. “Some industry representatives have claimed that SVB’s problems were really related to poor management and shortcomings in the Federal Reserve’s supervision,” Barr said. “It is not logical to argue that failings in supervision must mean that SVB was adequately capitalized — it wasn’t — or that supervision by itself can somehow assure safety and soundness throughout the banking system. It is not a choice between supervision and capital regulation — capital is and has always been the foundation of a bank’s safety and soundness.”  Most respondents continue to have doubts about entering the market.

Homebuying sentiment has plateaued at a relatively low level, suggesting that many consumers may be coming to terms with high mortgage rates and home prices, according to Fannie Mae. The June Home Purchase Sentiment Index (HPSI) posted a slight increase of 0.4 points month over month and 1.2 points year over year to 66, with six of the HPSI components showing little change during the period. HPSI component highlights:

"Additionally, consumers' mortgage rate expectations have tempered: A larger share of respondents think mortgage rates will stay the same over the next year, whereas mid-to-late last year, most thought rates would continue going up. This seems to signal that consumers are adapting to the idea that higher mortgage rates will likely stick around for the foreseeable future. "We continue to forecast home sales to slow in the second half of the year, compared to the first half, due to ongoing affordability constraints and lack of housing supply." |

|

- iMove Chicago

- Real Estate School

-

Laws

-

CRLTO

>

- 5-12-010 Title, Purpose And Scope.

- 5-12-020 Exclusions.

- 5-12-030 Definitions.

- 5-12-040 Tenant Responsibilities.

- 5-12-050 Landlord’s Right Of Access.

- 5-12-060 Remedies For Improper Denial Of Access.

- 5-12-070 Landlord’s Responsibility To Maintain.

- 5-12-080 Security Deposits.

- 5-12-081 Interest Rate On Security Deposits.

- 5-12-082 Interest Rate Notification.

- 5-12-090 Identification Of Owner And Agents.

- 5-12-095 Tenants’ Notification of Foreclosure Action.

- 5-12-100 Notice Of Conditions Affecting Habitability.

- 5-12-110 Tenant Remedies.

- 5-12-120 Subleases.

- 5-12-130 Landlord Remedies.

- 5-12-140 Rental Agreement.

- 5-12-150 Prohibition On Retaliatory Conduct By Landlord.

- 5-12-160 Prohibition On Interruption Of Tenant Occupancy By Landlord.

- 5-12-170 Summary Of Ordinance Attached To Rental Agreement.

- 5-12-180 Attorney’s Fees.

- 5-12-190 Rights And Remedies Under Other Laws.

- 5-12-200 Severability.

- Illinois Eviction Law (Forcible Entry And Detainer)

- Illinois Security Deposit Return Act

-

CRLTO

>

- Today's Cool Thing

- Social Media