Clearly, these are not the same as your grandfather's bank runs.

There’s a pivotal scene in the holiday classic film “It’s a Wonderful Life” when panicked depositors at the Bedford Falls Building & Loan swarm en masse to withdraw their funds. Protagonist George Bailey averts a bank run by explaining fundamentals: “You're thinking of this place all wrong, as if I had the money back in a safe. The money's not here. Your money's in Joe's house, right next to yours, and in the Kennedy house, and Mrs. Macklin's house, and a hundred others.” That was then. As the recent rash of bank closures have shown – including the collapse of Silvergate Capital Inc. and Silicon Valley Bank, both of California, followed by that of New York City-based Signature Bank – failures are immediate, with an acceleration largely fueled by digitization. It’s clear that no elegant, Great Depression-era soliloquy appealing to a sense of community would have helped avert a bank run in the real world today. How digitization is changing finance In a recent telephone interview with Mortgage Professional America, Emmanuel Daniel detailed differences from the past that allow for bank failures to occur at stunning speed and shock-and-awe spectacle. His new book, “The Great Transition: The Personalization of Finance is Here,” has garnered rave reviews for its prescient insights on the personalization of finance and its attendant perils. “What has changed – and is changing – the nature of banking of the US and globally is driven by several new factors,” Daniel said. “The first factor is because of the digitization of finance, a bank run is instantaneous, immediate and ruthless. In the old days, a bank run used to be thousands of people queuing up in front of the bank, and the bank still closing on time at 5 p.m.,” he said. Even after the bank closed, it would be days before the dust settled to assess the level of deposits left intact, he added. “Today every customer can just go online and demand to have their deposits withdrawn. Technology itself is a dimension that affects how banks respond and the options that are open to them.” How do banks measure liquidity? Then there’s the matter of liquidity that adds to the sheer spectacle of collapse: “The amount of liquidity the central bank has passed into the system and then the COVID recovery program and so on resulted in an incredible accumulation of deposits in the banking system,” Daniel said. “In the past, when a bank had access to an incredible volume of deposits, it actually worked well for the banks. In the US system, there is a history of banks having redeployed the assets they receive into high-yielding assets,” he said, pointing to Treasury bonds and mortgage-backed securities as examples. Ironically, the recently failed banks had been largely following the same tactics, Daniel added: “In one sense, what the banks had been doing is no different than what they have always been doing.” But the old template – the “balance sheet of traditional banks,” – may no longer apply, Daniel suggested: “Having access to cheap sources of deposit was an incredibly powerful proposition for banks,” he said. “It meant there were many things they could do with cheap sources of funding. But now the balance sheet is starting to change, and it has called into question some of the regulations that have been put in place after the 2008 crisis.” The upshot: “Regulators will now need to look back to the balance sheet of a bank and say, ‘What do we allow banks to do going forward?’ And I think that’s going to be a long, long haul because the nature of the securities that the banking industry invests in has new risks that didn’t exist before.” A global entrepreneur, Daniel is the founder of platforms such as The Asian Banker and Wealth and Society, through which he has had extensive contact with leaders in banking and finance around the world. Given the banking turmoil that has recently unfolded, the insights from his book are suffused with a measure of prescience. He suggested as much himself: “I actually predicted that the next crisis which is underway at the moment will be predicated not by any underlying asset on the balance sheet of a bank but on the perception of its ability to meet its obligation.” The breadth of insight presented in his book has drawn praise from business and political leaders:

0 Comments

A survey of economists reveals heightened expectations of a downturn

Odds of the US economy backsliding into a recession are higher now than a month ago after steady interest-rate hikes by the Federal Reserve and growing risks of tighter credit conditions in the wake of several bank failures. The probability of a downturn in the next 12 months stands at 65%, up from 60% odds in February, according to the latest Bloomberg monthly survey of economists. The poll was conducted March 20-27, in the aftermath of several bank closures that included Silicon Valley Bank, with 48 economists responding about the odds of a recession. After the Fed last week raised rates a quarter percentage point to the highest since 2007, economists worry not only about the impact on demand but the effect on the banking system. The collapse of SVB was precipitated by higher interest rates that reduced the value of the firm’s holdings of Treasuries. Financial institutions risk becoming more guarded in their lending approach, restricting access to capital needed by businesses to expand and consumers to buy homes, cars and other big-ticket items. “Even if the problem seems to have been contained so far, the full impact of recent events is still to unfold,” said James Knightley, chief international economist at ING. “Higher borrowing costs and reduced access to credit, resulting from banking stresses, mean a greater chance of a hard landing for the US economy.” Economists in the Bloomberg monthly survey maintained their expectations of another 25 basis-points increase in the Fed’s benchmark rate to a range of 5%-5.25% at the May meeting. They see the fed funds rate holding there through the rest of the year as the central bank tries to tamp down inflation. At the same time, forecasters also boosted their projections for the Fed’s preferred inflation gauge — the personal consumption expenditures price index — for every quarter through the third quarter of 2024. The metric is now seen averaging 3.9% in 2023 on an annual basis, up from last month’s projection of 3.4% and about double the Fed’s target. Respondents also boosted their expectations for the consumer price index for this year and the next. Fed officials have doubled down on the resilient labor market as one of the reasons why inflation has remained sticky, with strong wage gains helping fuel price pressures. Economists now forecast a delayed downturn in the job market and see the unemployment rate averaging 3.9% in 2023 compared with 4% last month. They expect it to climb to a peak of 4.7% in the second quarter of next year. Meantime, the median estimates see gross domestic product averaging 1% in both 2023 and 2024. Consumer spending, which accounts for about two-thirds of GDP, is projected to rise 1.4% this year, despite a sharp deceleration in the upcoming quarters.  The home price index has now fallen by 3% since June.

The US housing slump stretched into a seventh month in January. Home prices nationally fell 0.2% from December, according to seasonally adjusted data from S&P CoreLogic Case-Shiller. The index is now down 3% from its record high, reached in June. Prices have continued to soften as seller discounts become more common in a market where buyer demand has been sagging for months. Toward the end of 2022 and into January, mortgage rates eased slightly from the peak in November, giving some house hunters incentive to negotiate a deal. While prices in January were still higher than they were a year earlier, the pace of gains has cooled. The national index was up 3.8% annually, down from the 5.6% gain in December, non-seasonally adjusted data show. Despite turmoil in the banking industry “the Federal Reserve remains focused on its inflation-reduction targets, which suggest that rates may remain elevated in the near-term,” Craig Lazzara, managing director at S&P Dow Jones Indices, said in a statement Tuesday. “Mortgage financing and the prospect of economic weakness are therefore likely to remain a headwind for housing prices for at least the next several months.” The housing market is now in what’s traditionally its busiest season, when families rush to settle into new homes before the next school year starts. But higher borrowing costs and uncertainty over the economy are likely to continue to limit demand this spring, according to Hannah Jones, economic data analyst at Realtor.com. In addition, Fed Chair Jerome Powell signaled last week that the regional banking crisis may lead to stricter lending requirements, which in turn could make getting a mortgage more difficult. “This spring’s sales pace is expected to remain lower than last year,” Jones said. “Many sellers will feel the pressure to list their home for a lower price to ensure sufficient buyer attention and a quick sale.”  "Many prospective homebuyers continue to feel this affordability squeeze".

Homebuyer affordability continued to suffer in February due to the uptick in mortgage rates and high prices, according to the Mortgage Bankers Association's latest Purchase Applications Payment Index (PAPI). Nationwide, the index hit a new record high of 169.7 in February, up 4.9% month over month, indicating poorer borrower affordability conditions. The national median payment applied for by purchase applicants rose to $2,061 from $1,964 in January. The mortgage payment for borrowers applying for lower-payment loans grew to $1,391 from $1,322 the previous month. Additionally, the median mortgage payment for purchase loans climbed to $2,492 last month, MBA's Builders' Purchase Application Payment Index revealed. "Higher mortgage rates and home prices led to continued erosion in homebuyer affordability in February," said Edward Seiler, MBA's associate vice president of housing economics. "Many prospective homebuyers continue to feel this affordability squeeze, with the typical purchase application loan amount increasing $8,003 over the month to $320,003." Other key findings were:

"The results on mortgage performance are welcome news"

Mortgage forbearances were down across the board in February, with the total number of loans currently in forbearance plans declining four basis points from January, according to the Mortgage Bankers Association. MBA reported Monday that 300,000 homeowners are in forbearance plans, representing 0.60% of servicers’ portfolio volume as of February 28. The improvement comes as the national delinquency rate jumped 51 basis points to 3.69% in the fourth quarter of 2022. “The February results on mortgage performance is welcome news, given recent increases in delinquencies for other credit types such as credit cards and auto loans,” said Marina Walsh, MBA’s vice president of industry analysis. “However, with the possibility of a recession this year, we may see some deterioration in performance – particularly for government loans.” The percentage of Fannie Mae and Freddie Mac loans in forbearance dropped two basis points to 0.28%, while Ginnie Mae loans in forbearance fell nine basis points to 1.28%. The forbearance share for portfolio loans and private-label securities (PLS) edged down five basis points to 0.78%. “The forbearance rate decreased for both independent mortgage bank and depository servicers across all investor types in February,” Walsh said in a statement. “Even with the fewer days in the month – which often causes a drop in timely monthly payments – overall servicing portfolio performance declined only slightly to 95.8%, while performance of post forbearance workouts stayed essentially flat at 76%.”  It all came from 11 days of turmoil.

The speed with which four banks collapsed — and one continues to struggle — has left investors reeling. While the failures came in the span of just 11 days, the scenarios that brought them down were each unique. Here’s how the companies’ turmoil played out, and how regulators responded, amid concern the crisis might still spread: Silvergate Silvergate Capital Corp. was the first US bank to collapse, done in by its exposure to the crypto industry’s meltdown. With authorization from the Federal Reserve, the Federal Deposit Insurance Corp. had tried to step in, discussing with management ways to avoid a shutdown. But the La Jolla, California-based company couldn’t recover amid scrutiny from regulators and a criminal investigation by the Justice Department’s fraud unit into dealings with Sam Bankman-Fried’s fallen crypto giants FTX and Alameda Research. Though no wrongdoing was asserted, Silvergate’s woes deepened as the bank sold off assets at a loss to cover withdrawals by its spooked customers. It announced plans on March 8 to wind down its operations and liquidate its bank. Silicon Valley Bank With Silvergate’s obituary mostly written, investors and depositors in SVB Financial Group’s Silicon Valley Bank were already on edge when the company on March 8 announced a plan to sell $2.25 billion of shares — as well as significant losses on its investment portfolio. Shares of the company sank 60% the next day on the news, and it collapsed into FDIC receivership the following day. US regulators moved toward a breakup of the bank when they failed to line up a suitable buyer. But more hopeful news emerged on Monday, when the FDIC extended the bidding process after receiving “substantial interest” from multiple potential buyers. First Citizens BancShares Inc., one of the biggest buyers of failed US lenders, is still hoping to strike a deal for all of Silicon Valley Bank, Bloomberg News reported Monday, citing people familiar with the matter. Signature Bank Signature Bank became the third-largest bank failure in US history on March 12, following a surge in customer withdrawals that totaled about 20% of the company’s deposits. Silvergate’s implosion four days earlier had left clients skittish about keeping their deposits at Signature Bank, despite its much smaller exposure to crypto. Federal regulators said they lost faith in the company’s leadership, and they swept the bank into receivership. Both insured and uninsured customers were given access to all their deposits, under a provision regulators tapped known as the “systemic risk exemption.” Signature Bank’s deposits and some of its loans were taken over by New York Community Bancorp’s Flagstar Bank late Sunday. The acquirer agreed to purchase $38 billion of assets, including $25 billion in cash and about $13 billion in loans, from the FDIC. It also assumed liabilities of about $36 billion, including $34 billion in deposits. Signature’s branches will now operate as Flagstar locations. Credit Suisse Credit Suisse Group AG fell Sunday when Swiss officials brokered a deal with UBS Group AG for a 3 billion-franc ($3.2 billion) acquisition aimed at avoiding a broader financial crisis. The only other option under consideration was full or partial nationalization. The end of the 166-year-old Swiss institution followed Chief Executive Officer Ulrich Koerner’s attempt to save the bank with a massive outreach to clients, who had pulled an unprecedented amount of funds from the bank last year. The attempt ultimately wasn’t enough to counter multiple scandals and multibillion-dollar losses on Credit Suisse’s dealings with disgraced financier Lex Greensill and failed investment firm Archegos Capital Management. On March 9, the US Securities and Exchange Commission queried the bank’s annual report, forcing it to delay its publication. Panic spread after the failure of US regional lenders, and the chairman of the bank’s largest shareholder, Saudi National Bank, ruled out investing any more in the company. First RepublicFirst Republic Bank has fallen victim to the same customer flight that ultimately sank three of its US rivals, with one estimate of potential deposit outflows pegging the figure at $89 billion. Eleven US lenders tried to prop up First Republic Bank with a $30 billion cash infusion last week. But the San Francisco-based company, which caters to the personal-banking needs of tech’s elite and other wealthy individuals, has nonetheless dropped to an all-time low amid multiple credit-rating downgrades. JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon has hatched a new plan to aid First Republic that would convert some or all of the 11 banks’ $30 billion deposit injection into a capital infusion, Bloomberg reported Monday, citing people familiar with the situation.  Shrinking capacity caused by volatile rate environment.

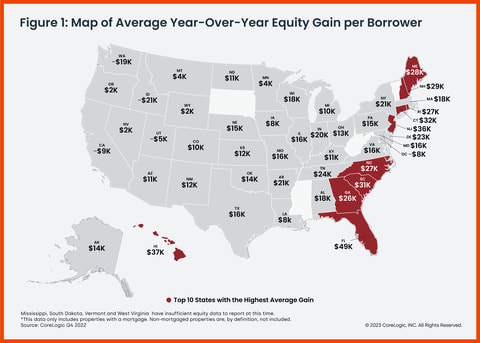

Mortgage credit availability fell to a decade-low in February, a decline that may be driven by the pressure of high interest rates. The Mortgage Bankers Association reported Tuesday that its mortgage credit availability index (MCAI) – benchmarked to 100 – decreased by 3% to a reading of 100.1 in February. The drop in the MCAI indicates that lending standards are tightening. "Mortgage credit availability decreased to its lowest level since January 2013, with all loan types seeing declines in availability over the month," said Joel Kan, MBA's vice president and deputy chief economist. Kan pointed out that the conventional subindex decreased by 4.3% to its lowest level in the survey, which goes back to 2011. The government index dipped 1.6%, while conventional MCAI and its jumbo subindex both edged down 4.4% in February. "This decline was driven by the ongoing trend of shrinking industry capacity as mortgage rates stayed significantly higher than a year ago," Kan said. "Additionally, in this volatile rate environment and potentially weakening economy, there was also a reduction in refinance programs offered for low credit score and high-LTV borrowers." According to MBA, the average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $726,200) rose five basis points to 6.49% for the week ending March 3.  Home equity trends follow steady decline in home price growth. Annual home equity growth continued to cool as the decline in home prices persisted in the fourth quarter of 2022, CoreLogic reported Thursday. Homeowners saw their equity grow by 7.3% year over year, marking a collective gain of $1 trillion. The average mortgage borrower earned about $14,300 in equity, compared with the $63,100 increase in the first quarter of 2022. "While equity gains contracted in late 2022 due to home price declines in some regions, U.S. homeowners on average still have about $270,000 in equity more than they had at the onset of the pandemic," said CoreLogic chief economist Selma Hepp. CoreLogic's home price index slowed to a 5.5% annual rate in January – the lowest recorded since June 2020. CoreLogic estimates that 145,000 homes would regain equity if prices rose by 5%. However, if prices fall by 5%, 215,000 properties would fall underwater. Negative equity, also known as underwater mortgages, increased 6% in Q4 to 1.2 million homes from the previous quarter but was down 2% year over year.  "Nevertheless, with 66,000 borrowers entering negative equity in the fourth quarter, the total number of underwater properties is now approaching levels seen at the end of 2021, which was the lowest since the Great Recession," Hepp said.

"The new hot spots for equity declines are largely markets that have seen the most significant home price deceleration, including Boise, Idaho; the San Francisco Bay Area; cities in Utah; Phoenix and Austin, Texas."  More aggressive Fed rate hikes could spell trouble for mortgage market.

Long-term US mortgage rates increased for the fifth week in a row as the Federal Reserve prepares for higher and possibly faster rate hikes in coming months. According to Freddie Mac, the average 30-year fixed-rate mortgage climbed from 6.65% last week to 6.73% as of March 9. The 15-year fixed rate increased from 5.89% to an average of 5.95% over the week. Freddie Mac chief economist Sam Khater said the continued rise in home loan rates comes "as the Federal Reserve signals a more aggressive stance on monetary policy." "Overall, consumers are spending in sectors that are not interest rate sensitive, such as travel and dining out. However, rate-sensitive sectors, such as housing, continue to be adversely affected," he continued. "As a result, would-be homebuyers continue to face the compounding challenges of affordability and low inventory." Marty Green, principal at Polunsky Beitel Green, added that Fed Chair Jerome Powell's testimony on Tuesday made it clear that the hikes are inevitable based on current data. "Chairman Powell's testimony made clear that, much like Sherman's March to the Sea, the Federal Reserve march to higher rates is inevitable based on current data." "The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated," Powell said in his semi-annual testimony before the Senate Banking Committee. "While a quarter-point increase in the Federal Funds rate is still the most likely outcome of the Federal Reserve's March meeting, expect the Fed to adopt a half-point increase in March if data on inflation and labor conditions continue to run hotter than expected," Green said. "Based on Chairman Powell's testimony, neither the risk of higher unemployment nor the risk of tipping the economy into a recession will deter the Fed from raising rates sufficiently to get inflation down closer to its target level. If that means quickening the pace of increases once again, the Federal Reserve is prepared to do so. "In response to the testimony, mortgage rates have once again increased to over 7%, a more than a 50-basis point increase in less than a month. These elevated rates are likely to cool the Spring housing market just as it was about to get into full swing. Potential buyers would be well served to lock their interest rates, if possible, rather than face the uncertainty that higher rates might bring."  Black Knight Mortgage Monitor report shows market volatility exacerbated by inventory challenges.

Rising mortgage rates and weakening demand continued to deter many potential sellers from putting their properties on the market, exacerbating the national housing supply crisis. About 90% of US markets faced growing inventory shortages in January, according to the findings of Black Knight’s latest Mortgage Monitor report. For-sale inventory in January decreased for the fourth month after seeing strong improvement early last year. Months of supply have stagnated at 3.1 in recent months due to cooling homebuyer demand and a weakening inflow of new listings. New listings have run at a deficit from pre-pandemic averages for 25 consecutive months now. Andy Walden, Black Knight’s VP of enterprise research, explained that inventory shortages keep home prices higher than they would be given current affordability constraints as rising rates continue to prevent potential sellers from putting their homes on the market. “The interplay between inventory, home prices and interest rates has been the defining characteristic of the housing market for the last two years, and this continues to be the case,” Walden said. “Today, we see buyer demand dampened under pressure from rising rates and their impact on affordability, with purchase rate-lock volumes cooling in late February. However, when rates ticked down closer to 6% early in the month, we saw a rebound in buy-side demand. “On the other side of the equation, we’ve seen a consistent theme of potential sellers – many with first-lien rates a full three percentage points below today’s offerings – pulling back from putting their homes on the market. In fact, January marked the fourth consecutive monthly decline in overall for-sale inventory, according to our collateral analytics data, with the primary driver being a 25-month stretch of new listing volumes running below pre-pandemic averages. While demand remains weak, faltering supply has resulted in months of available inventory stagnating near 3.1 in recent months.” Home prices continue to moderate, according to Black Knight, but at a slower pace than in recent months. Prices fell for the seventh consecutive month to 5.5% in January, down 24 basis points from December and 13 basis points on a seasonally adjusted basis – the smallest yet during that period. The annual home price growth rate (now at 3.4%) is on pace to fall below 0% by March or April. “Sharply rising 30-year rates in February have weakened home affordability, with nearly all major US markets remaining unaffordable as compared to their own long-run averages,” Walden said. “With 30-year rates at 6.5% in late February, it took 33.2% of the median household income to make the monthly principal and interest payments on the average home purchase. That’s up from January’s 32.4% and significantly above the 30-year average of ~24%, but still, 3.5 percentage points below the 37% level reached in October 2022 when affordability hit a more than 35-year low. “Between escalating inventory challenges and worsening affordability, we’re seeing some volatility in the market – just not in the form of widespread, steep price corrections.” |

|

- iMove Chicago

- Real Estate School

-

Laws

-

CRLTO

>

- 5-12-010 Title, Purpose And Scope.

- 5-12-020 Exclusions.

- 5-12-030 Definitions.

- 5-12-040 Tenant Responsibilities.

- 5-12-050 Landlord’s Right Of Access.

- 5-12-060 Remedies For Improper Denial Of Access.

- 5-12-070 Landlord’s Responsibility To Maintain.

- 5-12-080 Security Deposits.

- 5-12-081 Interest Rate On Security Deposits.

- 5-12-082 Interest Rate Notification.

- 5-12-090 Identification Of Owner And Agents.

- 5-12-095 Tenants’ Notification of Foreclosure Action.

- 5-12-100 Notice Of Conditions Affecting Habitability.

- 5-12-110 Tenant Remedies.

- 5-12-120 Subleases.

- 5-12-130 Landlord Remedies.

- 5-12-140 Rental Agreement.

- 5-12-150 Prohibition On Retaliatory Conduct By Landlord.

- 5-12-160 Prohibition On Interruption Of Tenant Occupancy By Landlord.

- 5-12-170 Summary Of Ordinance Attached To Rental Agreement.

- 5-12-180 Attorney’s Fees.

- 5-12-190 Rights And Remedies Under Other Laws.

- 5-12-200 Severability.

- Illinois Eviction Law (Forcible Entry And Detainer)

- Illinois Security Deposit Return Act

-

CRLTO

>

- Today's Cool Thing

- Social Media