Application activity slows as higher interest rates bites.

Mortgage applications fell to their lowest level in a month as interest rates for most loan types rise, the Mortgage Bankers Association reported today. MBA’s Market Composite Index – a measure of loan application volume – ticked down 4.4% on a seasonally adjusted basis and down 6% when unadjusted. Demand weakened as the average contract interest rate for a 30-year mortgage increased 10 basis points for the week ending June 30. “As mortgage Treasury spreads remained wide, the 30-year fixed rate increased to 6.85%, the highest rate since the end of May,” MBA deputy chief economist Joel Kan said. Kan also noted that purchase applications decreased for the first time in a month, down 5% week over week. Refinance application volume declined by 4% from the previous week. “Rates are still over a percentage point higher than a year ago, and housing affordability is still a challenge in many parts of the country,” Kan added. “However, the average loan size for a purchase application declined to $423,500 – its lowest level since January 2023. This was likely driven by reduced purchase activity in some high-price markets and more activity in some of the lower price tiers as buyers searched for more affordable options.” In a separate report, MBA found that homebuyer affordability worsened in May. The median loan payment applied for by purchase loan applicants was up to $2,165, a 2.5% month-over-month increase and a 14.1% spike from May 2022. For borrowers applying for lower-payment mortgages, the national mortgage payment climbed to $1,462 in May.

0 Comments

Affordability just keeps on eroding.

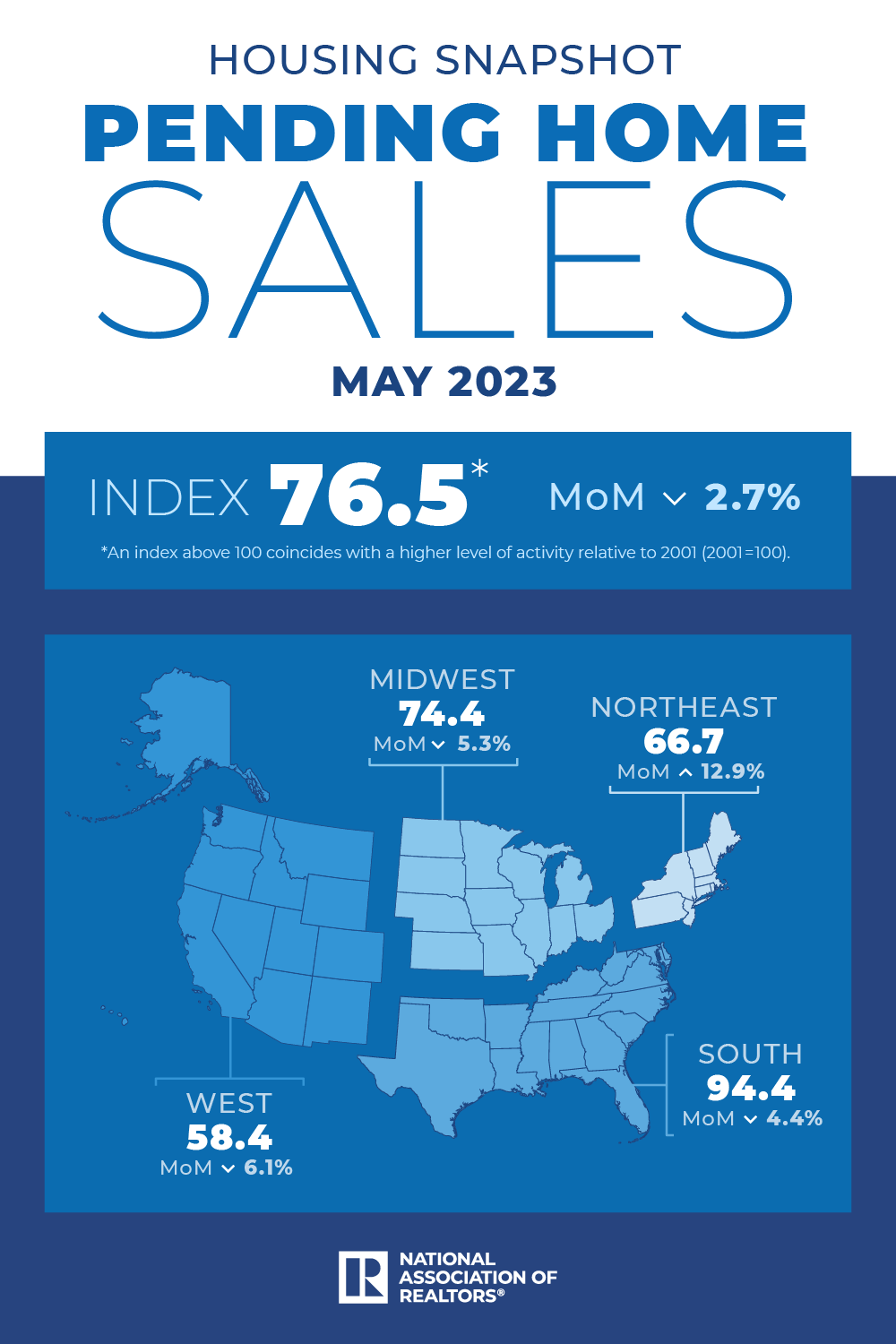

Would-be homebuyers are willing to take on sharply higher mortgage payments, even as home prices have begun to pull back this year. The median monthly payment listed on applications for home purchase loans jumped 14.1% in May from a year earlier to an all-time high $2,165, according to the Mortgage Bankers Association. The May figure also represents a 2.5% increase from April. “Homebuyer affordability eroded further in May as prospective buyers continue to grapple with high interest rates and low housing inventory,” Edward Seiler, the MBA’s associate vice president of housing economics, said in a release last week. The size of the mortgage and the interest rate on the loan influence how large the monthly payment on a 30-year fixed-rate mortgage will be. Those two housing market variables have ballooned in recent years. Home price growth accelerated during the pandemic, fueled by ultra-low mortgage rates and bidding wars as competition for relatively few properties on the market intensified. Even after the market cooled last summer as the Federal Reserve raised interest rates in its bid to slow economic growth and tame inflation, home price appreciation remained resilient until this February, when the median US home price slipped 0.2% from a year earlier -- its first annual decline in 13 years, according to the National Association of Realtors. Home prices have kept falling since, most recently sliding 3.1% in May from a year earlier to a median $396,100, according to the NAR. Still, the national median home price remains nearly 40% higher than it was three years ago. Meanwhile, the average rate on a 30-year home loan climbed to a new high for the year this week at 6.81%, mortgage buyer Freddie Mac said Thursday. That’s more than double what it was two years ago. The combination, along with a stubbornly low level of homes for sale, is driving mortgage payments higher, pushing the limits of what many homebuyers can afford. Consider that two years ago the median national monthly payment on home loan applications was $1,320.48, or 63.4% less than what it was last month. A recent forecast by Realtor.com calls for the average rate on a 30-year mortgage to drop to 6% by the end of the year. Lower rates could motivate some homeowners to sell, adding more sorely needed inventory to the market. However, lower rates could also spur more buyers to come off the sidelines, which would heighten competition and push up prices.  Contract signings remained stalled as buyers wait for new listings in the housing market. Pending home sales remained sluggish in May, hindered by a dearth in housing supply, the National Association of Realtors said Thursday. The pending home sales index fell to 76.5 in May, down 2.7% month over month and 22.2% lower than a year ago, NAR’s latest report revealed. Consensus forecasts expected pending home sales to remain flat. NAR chief economist Lawrence Yun noted that the lack of inventory continued to prevent housing demand from being fully realized.  “It is encouraging that homebuilders have ramped up production, but the supply from new construction takes time and remains insufficient,” Yun said. “There should be more focus on boosting existing-home inventory with temporary tax incentive measures.”

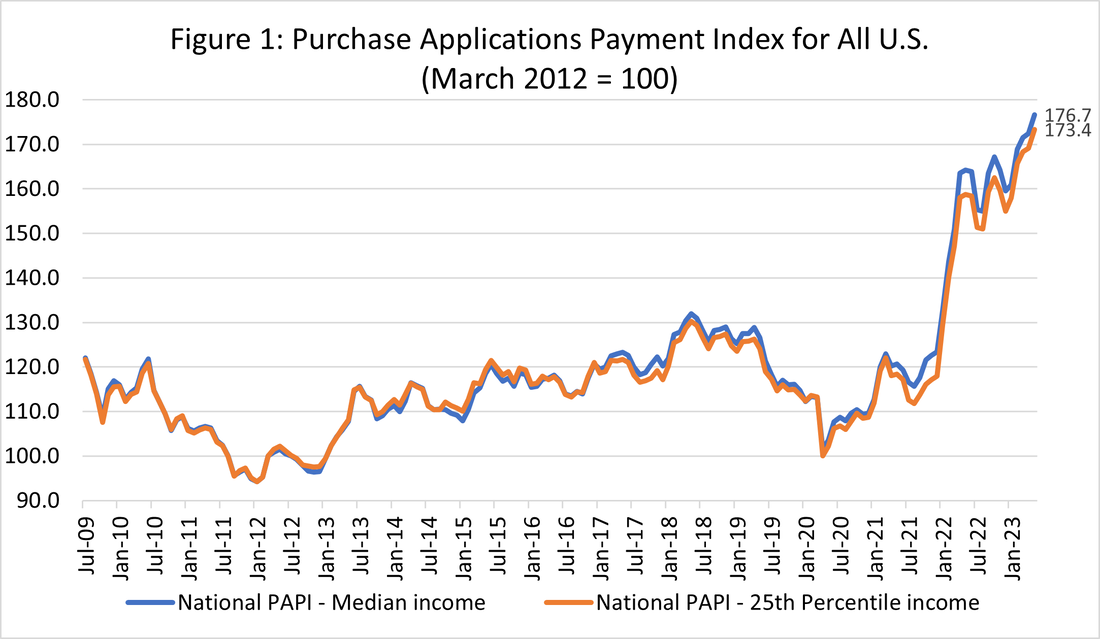

“High hopes that the housing market’s returning to normalcy may be coming down to earth, with May showing a 2.7% decline in pending home sales,” NerdWallet home expert Kate Wood added. “Normally, April to May would see a bump as home buying season really gets underway. One big reason contract signings are stalling? There simply isn’t enough supply. Even as home buyers adjust to the new reality of higher interest rates, their home searches remain stymied by lack of inventory.” Ksenia Potapov, economist at First American Financial, agreed. “The spring home-buying season has struggled to gain momentum. Mortgage rates remain high, reducing house-buying power and keeping existing homeowners rate-locked into their homes. As a result, the inventory of homes for sale, which typically increases throughout the spring and summer months, has remained near winter lows. “The divide between the existing-home and new-home markets continues to grow. While existing-home sales remain muted, multiple leading indicators on the new-home side, including new-home sales, new-home construction, and homebuilder sentiment, have trended higher.” On the bright side, Potapov highlighted that homebuyer demand and the labor market stayed strong, and potential home buyers are ready to jump in. “While limited inventory is likely to hold back sales activity, the housing market remains resilient,” she said.  Homebuyer affordability worsens, but experts find optimism in growing supply. Mortgage borrowers faced more affordability hurdles in May as loan application payments continued to creep higher, according to the Mortgage Bankers Association (MBA). MBA’s Purchase Applications Payment Index (PAPI), a gauge of borrower affordability conditions, hit a new record high of 176.7 in May. The increase indicates a rise in the mortgage payment-to-income ratio (PIR), which occurs when loan application amounts or mortgage rates climb, or earnings decrease.  The PAPI report showed a 2.5% increase in median loan payments applied for by applicants, up to $2,165 from $2,112 in April. It was $268 higher than a year ago, equal to a 14.1% jump.

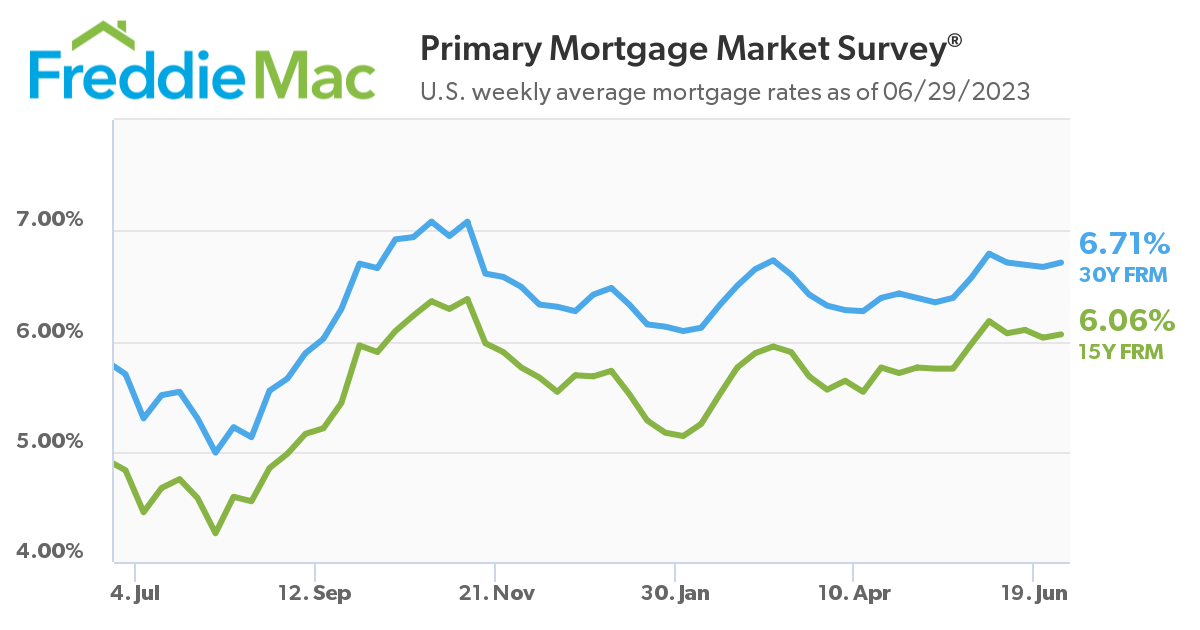

For borrowers applying for lower-payment mortgages, the national mortgage payment increased to $1,462 month over month. “Homebuyer affordability eroded further in May as prospective buyers continue to grapple with high-interest rates and low housing inventory,” said Edward Seiler, associate vice president of housing economics at MBA. “While supply remains low, we do expect that inventory will pick up in the near term, which will provide more opportunities for borrowers to buy a home.” The estimated supply of new homes for sale in May was 428,000, representing a supply of 6.7 months at the current sales pace. Meanwhile, mortgage rates have hovered in the 6-7% range in the first half of the year. Kelly Mangold, principal at RCLCO Real Estate Consulting, commented: “Builder sentiment continues to improve as the number of new homes under construction has increased going into spring and summer homebuying season. Buyer demand remains elevated, and as buyers have begun to prepare for higher payments and adjust expectations, and we are seeing that the market has continued to shift to meet this demand.”  "Homebuyers have adjusted" Freddie Mac has revealed its latest update on long-term mortgage rates, with the benchmark 30-year mortgage rate rising after three weeks of decline. There was a four-basis-point uptick in the 30-year fixed-rate mortgage, which averaged 6.71% as of June 29. The 15-year loan rate inched up three basis points to 6.06% from last week.  affordability headwinds, homebuyers have adjusted and driven new home sales to its highest level in more than a year,” said Freddie Mac chief economist Sam Khater. “New home sales have rebounded more robustly than the resale market due to a marginally greater supply of new construction. The improved demand has led to a firming of prices, which have now increased for several months in a row.”

Mark Fleming, chief economist of First American Financial, believes prices have remained resilient because the relationship between rising mortgage rates and home prices may not be as straightforward as many think. “Even as the Federal Reserve continues to fight inflation with restrictive monetary policy, which will keep upward pressure on mortgage rates, don’t expect house prices to decline dramatically,” Fleming said. “History has shown that higher rates may take the steam out of rising prices, but it doesn’t cause them to collapse entirely. This is especially true in today’s housing market, where the demand for homes continues to outpace supply, keeping the pressure on house prices.” |

|

- iMove Chicago

- Real Estate School

-

Laws

-

CRLTO

>

- 5-12-010 Title, Purpose And Scope.

- 5-12-020 Exclusions.

- 5-12-030 Definitions.

- 5-12-040 Tenant Responsibilities.

- 5-12-050 Landlord’s Right Of Access.

- 5-12-060 Remedies For Improper Denial Of Access.

- 5-12-070 Landlord’s Responsibility To Maintain.

- 5-12-080 Security Deposits.

- 5-12-081 Interest Rate On Security Deposits.

- 5-12-082 Interest Rate Notification.

- 5-12-090 Identification Of Owner And Agents.

- 5-12-095 Tenants’ Notification of Foreclosure Action.

- 5-12-100 Notice Of Conditions Affecting Habitability.

- 5-12-110 Tenant Remedies.

- 5-12-120 Subleases.

- 5-12-130 Landlord Remedies.

- 5-12-140 Rental Agreement.

- 5-12-150 Prohibition On Retaliatory Conduct By Landlord.

- 5-12-160 Prohibition On Interruption Of Tenant Occupancy By Landlord.

- 5-12-170 Summary Of Ordinance Attached To Rental Agreement.

- 5-12-180 Attorney’s Fees.

- 5-12-190 Rights And Remedies Under Other Laws.

- 5-12-200 Severability.

- Illinois Eviction Law (Forcible Entry And Detainer)

- Illinois Security Deposit Return Act

-

CRLTO

>

- Today's Cool Thing

- Social Media