But strong mortgage demand continues to push prices up.

Single-family home prices cooled in the first quarter, but pent-up mortgage demand continued to drive price growth. Annual price growth of single-family properties rose at a pace of 4.7% in Q1 2023, down from the revised annual growth rate of 8.6% in Q4 2022, according to Fannie Mae’s latest Home Price Index (HPI). Quarter over quarter, home prices ticked up 1% in the first quarter after seeing a 0.0% change in the previous quarter. “As expected, the annual rate of increase in home prices has slowed dramatically in response to the rapid and significant increase in interest rates,” said Doug Duncan, senior vice president and chief economist of Fannie Mae. “Still, the fact that prices rose slightly in the first quarter is evidence of significant pent-up mortgage demand, despite ongoing affordability constraints. “Even though mortgage rates remain elevated compared to the previous few years, the acute lack of housing supply remains supportive of home prices. Of course, the shortage of homes for sale is currently being exacerbated by the so-called ‘lock-in effect,’ which continues to disincentivize huge numbers of households with low mortgage rates from listing their homes.” Fannie Mae’s HPI consists of seasonally adjusted and non-seasonally adjusted national indices designed to serve as indicators of general single-family home price trends. The index, first produced in 1975, is publicly available at the national level and is published mid-month during the first month of each new quarter.

0 Comments

Decline triggered first-time homebuyers to pull back.

Mortgage applications fell 8.8%, prompting a pullback in application activity, according to the Mortgage Bankers Association’s latest survey for the week ending April 14. Home loan application volume declined 8.8% on a seasonally adjusted, week-over-week basis. When unadjusted, application activity was down 8% from the previous week. “With more first-time homebuyers in the market, we continue to see increased sensitivity to rate changes. The 30-year fixed rate increased 13 basis points to 6.43%, which led to purchase applications declining 10%,” noted Joel Kan, MBA’s vice president and chief economist. “Affordability challenges persist, and there is limited for-sale inventory in many markets across the country, so buyers remain selective on when they act.” Applications for mortgage refinances dropped 6%, and purchase activity plummeted 10% from one week earlier. Refinances accounted for just over a quarter (27.6%) of total applications, as rates remained more than a full percentage point above the same week a year ago. “This leaves very little refinance incentive for most homeowners,” Kan said. The FHA share of total application volume grew four basis points to 12.7%. VA loans made up 11.7%, and USDA loans comprised 0.5% of the overall application figure. “The 10% drop in FHA purchase applications, and the increase in the average purchase loan size to its highest level in a month, are other indications that first-time buyers have pulled back,” Kan said. “The spread between the jumbo and conforming 30-year fixed rates widened slightly last week to 15 basis points, but this was a much tighter spread compared to the past year. As banks reduce their willingness to hold jumbo loans, we expect this narrowing trend to continue.”  "It remains unclear how much recent banking turmoil and tighter credit affected these data".

New housing starts decreased in March after a rebound in February, but single-family production showed signs of a gradual upturn as mortgage rates stabilized. Overall residential construction dropped to a seasonally adjusted annual rate of 1.42 million units in March, the Census Bureau reported. The March reading was 0.8% below the revised February estimate of 1.43 million and 17.2% below the March 2022 rate of 1.72 million units. “March had its fair share of economic uncertainty with news of failing banks, which may have spooked some buyers,” said Kelly Mangold, principal of RCLCO Real Estate Consulting. “As spring is a historically popular time for sales, builders may still look to increase their inventory in the coming months to hopefully capture buyers who may have been sidelined over the past year but are looking to finally enter the market.” Fannie Mae chief economist Doug Duncan said the latest reading puts first-quarter construction moderately above their forecast as demand for housing proves to be more resilient than they had previously expected. “The supply of existing homes remains constrained both because of a decade of underbuilding following the Great Financial Crisis and, more recently, the lock-in effect discouraging current homeowners from listing their homes for sale (and thus giving up their low mortgage rate),” Duncan explained. “As such, in light of an extremely limited supply of existing homes for sale, many homebuyers are turning to new homes. This phenomenon coincides with lower building materials costs compared to a year ago, which allows homebuilders to offer stronger concessions and rate buy-downs while maintaining profit margins.” Within the overall figure, single-family housing starts rose 2.7% to an 861,000 annualized rate. However, this remains 27.7% lower than a year ago. Multifamily production, while still at historically high levels, gave back part of its early-year surge with a 5.9% decline to a SAAR of 559,000, Duncan noted. “It remains unclear how much, if at all, recent banking turmoil and tighter credit conditions affected these data,” he said. “On one hand, mortgage rates pulled back, which could spur some additional single-family demand. However, tighter credit conditions would result in homebuilders having a harder time financing new projects, which would weigh on future construction activity.” Overall permits fell 8.8% to a 1.41 million pace in March. Single-family permits were up 4.1% to an 818,000 unit rate but down 29.7% compared to a year ago. Multifamily permits plunged 22.1% to an annualized 595,000 pace. The number of single-family homes under construction fell for the 10th consecutive month in March to 716,000. Builders completed 15,000 more homes than began construction, resulting in a decline for the construction pipeline, according to the National Association of Home Builders. “With builder sentiment climbing for four consecutive months and single-family starts continuing to move gradually higher from low levels since the beginning of the year, this indicates that a turning point for single-family construction will occur later this year after declines in 2022,” said NAHB chairman Alicia Huey. “However, builders are still challenged by ongoing supply-chain issues and a skilled labor shortage.” “We expect choppiness for single-family construction in the months ahead, with the 2023 data posting significant year-over-year weakness before improving on a sustained basis,” said NAHB chief economist Robert Dietz. “The multifamily market softened in March, and we anticipate ongoing declines for apartment construction in the months ahead due to tighter lending conditions in the commercial real estate sector.”  Properties values have been hit.

Brookfield Corp. funds have defaulted on a $161.4 million mortgage for a dozen office buildings, mostly around Washington, DC, as rising vacancies hit property values. The loan transferred to a special servicer who is working with “the borrower to execute a pre-negotiation agreement and to determine the path forward,” according to a filing on the commercial mortgage-backed security. Some landlords are defaulting on debt as borrowing costs surge and the prospects of filling up office towers wanes given the rise in remote and hybrid work. Those trends have weighed on values, with prices on high-quality office properties falling about 25% in the past year, according to Green Street. About 4.8% of office properties with CMBS were managed by special servicers in March, up from 3.2% a year ago, according to Trepp. Brookfield, a major office owner, previously defaulted on debt tied to two Los Angeles buildings, the Gas Company Tower and the 777 Tower. Landlords including Columbia Property Trust, owned by funds managed by Pacific Investment Management Co., and a venture started by WeWork Inc. and Rhone Group have also defaulted on office debt. Another Brookfield office property in Los Angeles, 725 South Figueroa St., was transferred to a special servicer and placed on watch by Kroll Bond Rating Agency, according to a note Tuesday. “We have always focused on quality, so 95% of what we own are trophy and Class A buildings that continue to see strong demand globally and benefit from the flight to quality,” Brookfield spokesperson Kerrie McHugh said in an emailed statement. “While the pandemic has posed challenges to traditional office in some parts of the US market, this represents a very small percentage of our portfolio.” In the Washington metro area, office property values have plunged 36% through March from a year earlier, on par with declines nationwide, according to the Green Street index. About 43% of workers in the region were in the office during the week of April 5 compared with pre-pandemic levels, according to Kastle Systems. That’s lower than cities such as New York, Chicago and Austin, Texas, but higher than some areas in California that have been particularly hit by the pullback from technology firms. Among the dozen buildings in the Brookfield portfolio with the $161.4 million debt, occupancy rates averaged 52% in 2022, down from 79% in 2018 when the debt was underwritten, according to the report. Monthly payments on the mortgage’s floating-rate debt jumped to about $880,000 in April from just over $300,000 a year earlier as the Federal Reserve raised interest rates. Office-related stocks have slumped this year amid concerns about the outlook for the properties. An index of publicly traded office real estate investment trusts dropped 19% this year through Monday’s close. The S&P 500 Index climbed 8% during that time frame.  He is in the spotlight for figures relating to a company that no longer exists.

Supreme Court Justice Clarence Thomas is in the spotlight for allegedly reporting significant sums from a defunct real estate company, The Washington Post reported Monday. In his financial disclosure forms, Thomas reported that he received rental income of between $50,000 and $100,000 annually from a Nebraska real estate firm called Ginger, Ltd., Partnership. The firm, founded in 1982 by Ginni Thomas and her family, was dissolved in 2006. That year, a separate company, Ginger Holdings LLC, was created and took over the closed firm’s land leasing business, according to The Post, citing state incorporation and property records. However, Thomas has continued to report income from the defunct company. The Post acknowledged that the most recent misstatement might be a simple “paperwork error.” “But it is among a series of errors and omissions that Thomas has made on required annual financial disclosure forms over the past several decades, a review of those records show,” The Washington Post wrote. “Together, they have raised questions about how seriously Thomas views his responsibility to accurately report details about his finances to the public.” Thomas faced scrutiny after ProPublica revealed early this month that he accepted lavish annual vacation trips from Texas billionaire Harlan Crow for several years. Thomas did not disclose those trips on the forms, as well as the $133,363 Georgia home Crow bought him, which could be in violation of federal law. Federal Justice disclosure law requires justices to report real estate sales over $1,000 to the public. Thomas said in statements through the years that he has always tried to comply with disclosure guidelines, though he has not commented on the property transactions and vacations.  Big default shows loan pressures as rates rise.

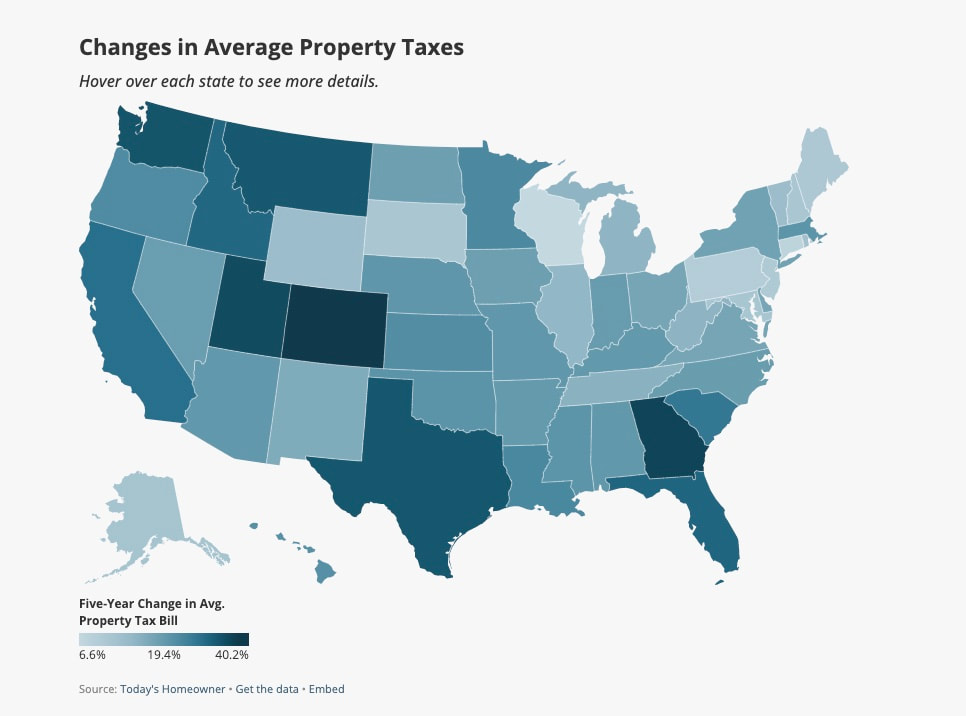

A recent foreclosure of four Houston apartment complexes highlights the impact of rising interest rates on the multitrillion-dollar rental-housing market. Applesway Investment Group, which borrowed nearly $230 million to acquire the buildings during the pandemic, defaulted on its loans, leading Arbor Realty Trust to foreclose on the properties. New York-based Fundamental Partners purchased the Houston properties for an undisclosed sum. Arbor Realty Trust is a listed specialist multifamily and commercial direct lender based in Uniondale, NY. With a portfolio of around $28 billion, it earns around $115 million a year, and saw nearly $11 billion in originations last year, a drop from its 2021 numbers. With a structured loan book that is 97% floating rate, its clients will be suffering as rates have jumped over the last year. The turbulence in commercial real estate is now affecting rental apartments, beyond urban offices and older shopping centers. The multifamily sector has been viewed as a relatively safe investment, particularly due to increased home prices during the pandemic that pushed many potential buyers to continue renting. Landlords have enjoyed rising apartment rents and affordable debt, driving property values to record levels. However, the recent uptick in interest rates has dampened the apartment sector's appeal. Property values have declined by more than 20%, according to Green Street, a real estate analytics firm, and rent growth is decelerating. As a result, some buildings with significant floating-rate mortgages no longer generate sufficient profits to cover debt payments. Applesway's experience serves as a warning for commercial property investors who sought substantial returns by purchasing modestly-priced buildings and increasing rents following renovations. As interest rates rise and hedging contracts expire, foreclosures like Applesway's could become increasingly common. Trepp data shows that a record $151.8 billion in US mortgages backed by rental apartment buildings will mature this year, with $940.1 billion set to expire over the next five years.  Taxes are just now beginning to catch up with soaring home values. In normal times, as a home appreciates in value, its property taxes follow in short order. But these are not normal times: Given the breakneck speed with which the housing market has taken off the last few years, property tax increases could hardly keep up – until now. In 2023, the small reprieve of relatively lower effective property tax rates will end and could yield a measure of sticker shock – especially for recent homebuyers. Researchers at Today’s Homeowner analyzed housing data across 585 cities spread across the country to track the corresponding rise in property taxes as it relates to skyrocketing home values – soaring valuations spurred by the lack of available houses for sale. The results don’t paint a pretty picture. According to the findings, the average property tax bill increased by more than 19% over the last five years -- $2,340 to $2,795. Average property tax bills rose the most in Western states, including Colorado (40.2%), Utah (34.7%) and Washington (33.2%), according to the report. Although property tax bills rose in nearly 97% of cities, the study showed effective property tax rates increased in only about 17% of the cities studied. Mortgage Professional America reached out to Hailey Neff of Today’s Homeowner for additional insight. In many parts of the country, those corrected property tax rates have already taken effect, Neff said. She noted researchers arrived at an effective property tax rate by taking the average property tax bill – how much the typical homeowner is paying every year on property taxes and dividing it by the median home sales in each stat. “It’s really the best way for us to compare different cities and states,” she said. Colorado has the nation’s highest property tax rates Bolstered property taxes are especially pronounced in western states, she noted. “We noticed that average property tax bills rose the most in western states, including Colorado, Utah and Washington,” she said. “People in Colorado are paying 40% more in their property taxes than they did in 2016, which is a huge jump. Housing prices in these western states are going through the roof, and, as home prices go up, you’ve got to pay more property taxes on them.” Other than protesting assessed values to the county tax assessor, Neff said, legislation is seen as the only viable option to help mitigate the hikes. “There’s lots of legislation going on right now,” she said. “I live in Idaho, and in the past legislative session there was a lot of talk about lowering property tax rates. Texas is doing the same.” Texas proposes a $12 billion property tax relief package Indeed, in the Lone Star state, property taxes are the seventh-highest in the US, according to smartasset.com. The average effective property rate in Texas is 1.60% compared to the national average of 0.09%, according to the site. The typical Texas homeowner pays $3,797 annually in property taxes, according to the site’s property tax calculator. On Thursday, the Texas House passed a $12 billion property tax relief package now headed to the Senate toward final passage, as reported by the Texas Tribune. An owner of a $350,000 home would realize more than $1,000 in savings over the course of two years under the relief bill, the news site reported. “There seems to be a lot of buzz about what to do about property taxes,” Neff said. “We want home values to stay high, but we also want people to be able to afford them, and property taxes can really make or break affordability for a lot of people.”  According to the study, all 50 states reported an increase in taxes paid, but the change in average property tax bills varied significantly. The top three states with the biggest increase in property taxes were:

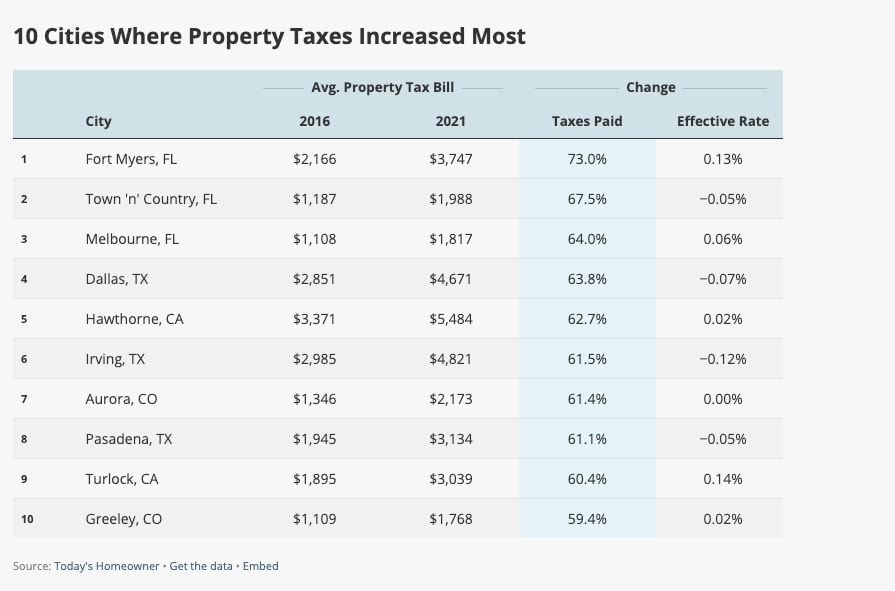

The report found that the top three cities that saw the largest increase in property taxes paid are all in Florida:

Despite the large increases for all three metros, the report found, only Fort Myers saw a significant increase in property tax rates (+0.13%) from 2016 to 2021. Melbourne saw a slight tax rate increase of 0.06%.

Aside from Florida, the top 10 cities that saw the largest increase in property tax bills were located in Texas, California, and Colorado — three states that saw significant increases in home values over the same period as detailed in the report.  Data reveals a 3.5% decline in applications to pick up a home.

The US housing market has been nothing if not unpredictable over the past year, with skyrocketing prices and low inventory leaving many potential buyers feeling discouraged. However, the news of falling mortgage rates may come as a welcome surprise to those looking to enter the market. For the fourth week in a row, the US 30-year fixed mortgage rate has fallen, dropping to a seven-week low of 6.4%. This comes after a period of financial turbulence caused by the collapse of several banks, which helped drive down Treasury yields — a key factor in determining mortgage rates. However, while the falling rates may seem like good news for homebuyers, borrowing costs remain high and housing inventory remains low, both of which are keeping a cap on homebuying activity. In fact, the Mortgage Bankers Association (MBA) reported that applications to buy a home declined for the first time in a month, with their index of mortgage applications to purchase a home decreasing by 3.5%. That being said, the MBA’s index of refinancing applications also fell, dropping by 5.4%. This suggests that while potential buyers may be hesitant to enter the market right now, current homeowners are taking advantage of the lower rates to refinance their existing mortgages. The MBA survey, which has been conducted weekly since 1990, uses responses from mortgage bankers, commercial banks, and thrifts to determine trends in the housing market. The data cover more than 75% of all retail residential mortgage applications in the US, making it a reliable indicator of the health of the housing market.  JP Morgan CEO hits out.

In his annual letter to shareholders, JP Morgan CEO Jamie Dimon didn’t hold back on his thoughts regarding the US banking crisis. According to Dimon, Silicon Valley Bank’s recent blunders were a result of lackluster regulation and oversight by US authorities, going so far as to say they were “hiding in plain sight.” Dimon believes that the crisis is far from over and that it will have lasting effects on the economy for years to come. He does, however, caution against overreacting with more rules and regulations, saying that it was the current regulations that incentivized banks to own low-interest assets that lost value when interest rates rose. He also criticized the Federal Reserve for not stress-testing banks on how they would handle rising interest rates, a factor that played a significant role in Silicon Valley Bank’s downfall. While Dimon didn’t absolve bank management of responsibility, he did point out that this was not the finest hour for many players involved. When uninsured depositors of Silicon Valley Bank realized it was losing money selling securities to keep up with withdrawal requests, they pulled their cash, causing regulators to step in and seize the bank. “This is not to absolve bank management – it’s just to make clear that this wasn’t the finest hour for many players,” he said. “All of these colliding factors became critically important when the marketplace, rating agencies and depositors focused on them.” JPMorgan’s future tied to AI Dimon, the last big-bank CEO still standing from the 2008 financial crisis, has the industry hanging on his every word. According to Dimon, JPMorgan’s future is tied to artificial intelligence, which he called “extraordinary.” He even named ChatGPT, the natural language processing tool, as one of the ways it is looking to “augment and empower employees.” But don’t be fooled, AI isn’t just for marketing and spotting risks; it’s also a key weapon in the fight against fraud and cyberattacks. “Because you can be certain that the bad guys will be using it, too,” Dimon warned. ‘Red-blooded, patriotic, free-enterprise and free-market capitalist’ The JPMorgan CEO also stated that he is still a “red-blooded, patriotic, free-enterprise and free-market capitalist,” despite the bank’s newly stated purpose of “making dreams possible for everyone, everywhere, every day.” Dimon also called on governments to consider using eminent domain to accelerate investments in renewable energy and fossil fuels, as the window for averting the costliest impacts of global climate change is closing. The bank is seeking to reduce the impact of capital-holding regulations by exploring business lines that require little or no capital, such as trading analytics or travel. Dimon also mentioned that the bank is evaluating its clients more rigorously. Complex regulations are pushing banks out of the mortgage business, as the cost of making and servicing loans increases legal liability. JPMorgan is still holding on to this business, but many banks have already exited the market. The 43-page letter also includes an assurance that the board is planning for Dimon’s potential successor, which is discussed during every board meeting. The board members are “on the case” and comfortable with where the bank is headed.  Market Composite Index drops from the previous week.

Spring may be in full swing, but the housing market seems to have missed the memo. According to the latest data from the Mortgage Bankers Association‘s (MBA) Weekly Mortgage Applications Survey, mortgage applications decreased by 4.1% from the previous week, and the Refinance Index decreased by a whopping 59% compared to the same week last year. Mike Fratantoni, the MBA’s SVP and chief economist, had some insight into the current state of the market. “Spring has arrived, but the housing market is missing the customary burst in listings and purchase activity that typically mark the season,” he said. “After four weeks of increasing purchase application activity, volume declined a bit this week even with another small drop in mortgage rates. Additionally, refinance application volume continues to be quite low. Although the mortgage rate for conforming balance loans declined by five basis points over the week to 6.40%, the mortgage rate for jumbo loans increased by nine basis points to 6.36%. While we have seen relative weakness at the high end of the housing market in recent months, the divergence in rates suggests that banks may be tightening credit in response to recent challenges, preserving balance sheet capacity as deposit balances have declined. In recent years, most jumbo loans have been kept on depository balance sheets.” It’s not all doom and gloom, however. Fratantoni predicts that there will be strong demand from first-time homebuyers in the coming years, thanks to a large number of millennials hitting peak first-time homebuyer age. The challenge remains affordability, particularly for those looking to enter the housing market at the entry-level segment. “At the entry-level segment of the market, purchase applications for both FHA and VA loans decreased last week,” he said. “We do expect strong demand from first-time homebuyers over the next several years given a large number of millennials hitting peak first-time homebuyer age, but affordability remains a real challenge in this environment.” The MBA also reported a dip in refinance and adjustable-rate mortgage (ARM) activity, with the refinance share decreasing to 28.6% of total applications and the ARM share dropping to 7.2%. Meanwhile, the FHA and VA share of total applications also decreased, but the USDA share increased slightly. |

|

- iMove Chicago

- Real Estate School

-

Laws

-

CRLTO

>

- 5-12-010 Title, Purpose And Scope.

- 5-12-020 Exclusions.

- 5-12-030 Definitions.

- 5-12-040 Tenant Responsibilities.

- 5-12-050 Landlord’s Right Of Access.

- 5-12-060 Remedies For Improper Denial Of Access.

- 5-12-070 Landlord’s Responsibility To Maintain.

- 5-12-080 Security Deposits.

- 5-12-081 Interest Rate On Security Deposits.

- 5-12-082 Interest Rate Notification.

- 5-12-090 Identification Of Owner And Agents.

- 5-12-095 Tenants’ Notification of Foreclosure Action.

- 5-12-100 Notice Of Conditions Affecting Habitability.

- 5-12-110 Tenant Remedies.

- 5-12-120 Subleases.

- 5-12-130 Landlord Remedies.

- 5-12-140 Rental Agreement.

- 5-12-150 Prohibition On Retaliatory Conduct By Landlord.

- 5-12-160 Prohibition On Interruption Of Tenant Occupancy By Landlord.

- 5-12-170 Summary Of Ordinance Attached To Rental Agreement.

- 5-12-180 Attorney’s Fees.

- 5-12-190 Rights And Remedies Under Other Laws.

- 5-12-200 Severability.

- Illinois Eviction Law (Forcible Entry And Detainer)

- Illinois Security Deposit Return Act

-

CRLTO

>

- Today's Cool Thing

- Social Media