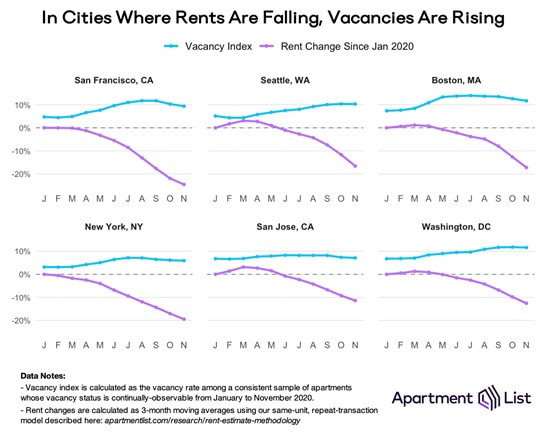

Rental search platform ApartmentList has released their national rent index report. The report, informed by a modified calculation, found rents have fallen 1.3% nationwide year over year. It showed, as well, where rents have fallen most dramatically and which multifamily rental markets have actually seen upswings in the pandemic. Rob Warnock, research associate at ApartmentList, broke down the data in greater detail. He explained that the drops and rise have played out, regionally, as would largely be expected during the pandemic, with major metro areas suffering declining rents and small cities, suburbs, and ex-urbs benefitting from urban flight and the availability of work from home infrastructure. He pointed, however, to a potential plateau in urban vacancy rates that could imply those markets have already hit bottom. He highlighted where, and how, mortgage professionals can position themselves to win out in this environment. “Since we started measuring in 2017, during the summer rents have gone up nationally, on average between two and 3%,” Warnock said when asked to contextualize this 1.3% drop. “We know that those were years where the economy was growing but using other measures we know that rents were going up pretty continuously all the way back to the Great Recession about 12 years ago…This is really the first year since the Great Recession where, during the busy summer months, rents saw the sort of dramatic national drop that we have right now.” That 1.3% drop, Warnock explained, is the composite of a few very expensive cities. Those high-priced rental markets in cities like San Francisco, New York, and Seattle have dropped significantly. Many of the smaller markets, conversely, have not seen much of a drop and some have actually seen a gain during the pandemic. On the top of the small-market growth list is the city of Boise, Idaho where Warnock said rents have grown at a double-digit percentage rate since the start of the pandemic. Boise might be the ideal COVID-19 real estate market. Nestled in the Rockies it has the access to nature many younger renters crave, as a college town it has a young population and an energetic feeling, and it has the benefit of momentum behind it. Warnock said Boise has been growing for a long time already and was top of mind for many city dwellers, especially on the West Coast, when the pandemic hit. As rents have declined in major cities, vacancy rates have gone up. Warnock explained that this measure was in keeping with less attractive multifamily urban centers in these cities. That said, he noted that recently those vacancy rates have begun to plateau and even slowly decline in major cities. He thinks this could mean that these markets have hit bottom and are beginning a slow recovery.  In the meantime, renters, landlords, and mortgage professionals in major urban centers should be ready for renters markets.’ In cities like Boise, mortgage pros can expect landlords to wield much more clout.

“Landlords definitely like don't have leverage in the market that they're used to,” Warnock said. “The relationship between landlords and tenants in cities like San Francisco is really flipped. There's just a lot less demand in the market, and a lot less leverage to command the same rent prices. The opposite is true in some of these smaller more affordable markets where, despite the economic uncertainty that a lot of people are facing, there's still so much demand in the market that landlords and property managers are still able to be picky with who they choose and are still able to leverage the competition in the market to command high rent prices.”

0 Comments

A gauge of contract signings to purchase previously owned US homes unexpectedly declined for a second month in October as higher prices and a limited number of listings impeded momentum in the housing market.

The National Association of Realtors’ index of pending home sales decreased 1.1% to 128.9 from the prior month after a revised 2% decline in September, according to data released Monday. The October drop compared with a median estimate in a Bloomberg survey of economists for a 1% gain. The decline underscores the challenges of further upward momentum in the housing market as the lack of available properties drives up asking prices and impedes demand. At the same time, contract signings are up almost 20% from a year ago on an unadjusted basis, highlighting the strides residential real estate has made amid record-low mortgage rates and buyer preferences for larger homes that double as office space. “The housing market is still hot, but we may be starting to see rising home prices hurting affordability,” Lawrence Yun, chief economist at the NAR, said in a statement. The combination of low rates, lean inventory and “very strong demand has pushed home prices to levels that are making it difficult to save for a down payment, particularly among first-time buyers.” By region, pending home sales declined in two of four major US regions, including a 5.9% decrease in the Northeast and a 0.7% drop in the Midwest. The gauge of contract signings in the South crept up 0.1%, while the index was unchanged for the West. The government’s revised estimate of third-quarter gross domestic product highlighted the recent strength in housing. Residential investment jumped an annualized 62.3% pace, the fastest since 1983, Commerce Department data showed last week. GDP rose at a record 33.1% annualized rate during the period. |

|

- iMove Chicago

- Real Estate School

-

Laws

-

CRLTO

>

- 5-12-010 Title, Purpose And Scope.

- 5-12-020 Exclusions.

- 5-12-030 Definitions.

- 5-12-040 Tenant Responsibilities.

- 5-12-050 Landlord’s Right Of Access.

- 5-12-060 Remedies For Improper Denial Of Access.

- 5-12-070 Landlord’s Responsibility To Maintain.

- 5-12-080 Security Deposits.

- 5-12-081 Interest Rate On Security Deposits.

- 5-12-082 Interest Rate Notification.

- 5-12-090 Identification Of Owner And Agents.

- 5-12-095 Tenants’ Notification of Foreclosure Action.

- 5-12-100 Notice Of Conditions Affecting Habitability.

- 5-12-110 Tenant Remedies.

- 5-12-120 Subleases.

- 5-12-130 Landlord Remedies.

- 5-12-140 Rental Agreement.

- 5-12-150 Prohibition On Retaliatory Conduct By Landlord.

- 5-12-160 Prohibition On Interruption Of Tenant Occupancy By Landlord.

- 5-12-170 Summary Of Ordinance Attached To Rental Agreement.

- 5-12-180 Attorney’s Fees.

- 5-12-190 Rights And Remedies Under Other Laws.

- 5-12-200 Severability.

- Illinois Eviction Law (Forcible Entry And Detainer)

- Illinois Security Deposit Return Act

-

CRLTO

>

- Today's Cool Thing

- Social Media