Tenants are canceling or not renewing their leases.

Near-empty office buildings, already a problem plaguing US cities, are becoming a worry for mortgage bondholders as landlords fall behind on repayments at the fastest rate in five years and the difficulty of refinancing the loans grows. The work-from-home phenomenon spawned by the COVID-19 pandemic and a slowing economy are pushing tenants to cancel or not renew leases, making building owners miss loan payments. More than 4% of office loans packaged into securities were at least 30 days in arrears as of May, the highest level since 2018, according to a recent report from real estate data firm Trepp. The rise in delinquencies is leading some investors to avoid commercial mortgage-backed securities with too much exposure to office buildings, in turn causing some CMBS yields to spike. Slack demand may make matters worse for real estate borrowers who anticipated refinancing almost a quarter of mortgages on office buildings this year. “This is just the tip of the iceberg for office delinquencies as $35 billion in CMBS office loans are scheduled to mature this year and the refinancing market is effectively shut to this asset class,” said Dan McNamara, founder of Polpo Capital Management. Polpo is betting against securities backed by office loans. Brookfield Corp. and a Pacific Investment Management Co. office landlord are among major institutional owners that have defaulted on large office mortgages this year. A venture started by WeWork Inc. and Rhone Group defaulted on a loan for a San Francisco office tower. The loan defaults raise the specter of missed payments to holders of commercial mortgage bonds. Delinquencies for all loans in commercial real estate securities jumped the most last month in almost three years, according to Trepp. In May, Kroll Bond Rating Agency said it is looking at downgrading securities tied to 11 commercial mortgage bonds, because the bonds are backed at least in part by office properties that are weakening. Should Kroll decide to cut its rating on all the debt, it would be its biggest such action since July 2020, early in the pandemic. For their part, CMBS investors say the shaky loan environment is pushing them to buy only deals backed by high-quality loans. The dropoff in demand all but shuttered the new-issue market earlier this year, and debt sales are down by almost 80% from this time last year, according to Bloomberg data. Several recent deals were noticeable for the relatively small number of big office building loans in the pool of mortgages being packaged for sale. Also, borrowers and underwriters have become more flexible in tailoring new issues to meet investor concerns, said John Kerschner, head of US securitized products at Janus Henderson Group, in an interview. “Office exposure in conduit deals has gone down this year, and if bond buyers are uncomfortable with specific loans and the issuer wants to get the deal done, they may very well take it out of the pool,” Kerschner said. Conduit transactions repackage different types of mortgages, including offices. Existing debt that rebundles a variety of commercial real estate loans is yielding among the most in over a decade in the secondary markets, over 5.5% in recent trading sessions, according to one measure. “Most of the risk is already priced in,” Kerschner said. “Investors who worried about offices left the market earlier and the rest is moving up the capital stack in general, looking for the investment-grade portions of the bonds.”

0 Comments

Applications fall again as homebuyers grapple with steep rates.

Mortgage demand cooled for the fourth week in a row as interest rates hover near record highs, according to the Mortgage Bankers Association. Mortgage application volume was down 1.4% during the week ending June 2 – seasonally adjusted for the Memorial Day holiday. When unadjusted, applications plunged 12% week over week. Demand for home loans declined despite a drop in rates, MBA deputy chief economist Joel Kan noted. “The 30-year fixed rate dipped to 6.81%, 10 basis points lower than last week but still the second highest rate of 2023,” Kan said in MBA’s news release. “Overall applications were more than 30% lower than a year ago, as borrowers continue to grapple with the higher rate environment.” MBA’s refinance index decreased 1%, and the purchase index decreased 2% from the previous week. On the other hand, the refinance share of mortgage activity increased six basis points to 27.3% of total applications. Applications for FHA loans increased to 13.2% from 12.7% the week before. The VA share rose to 12.5% from 12.1%, while the portion of USDA loan applications slipped to 0.4% from 0.5% the week prior. “Purchase activity is constrained by reduced purchasing power from higher rates and the ongoing lack of for-sale inventory in the market, while there continues to be very little rate incentive for refinance borrowers,” Kan said. “There was less of a decline in government purchase applications last week, which was consistent with a growing share of first-time home buyers in the market.”  It's another blow for a struggling downtown.

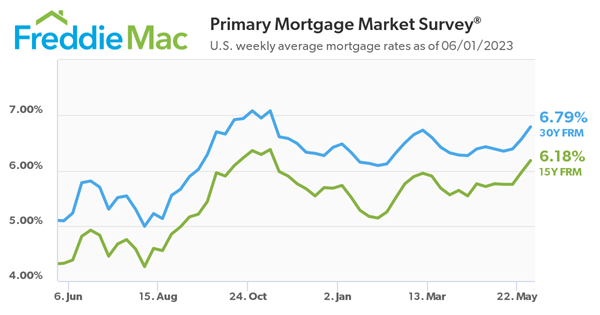

Park Hotels & Resorts Inc. has stopped making payments on a loan tied to the Hilton San Francisco Union Square and the Parc 55 San Francisco, two of the city’s largest hotels, dealing another blow to a downtown struggling with remote work and mounting public safety concerns. Park is working with servicers on the $725 million loan to determine the best path forward for the 1,921-room Hilton property and the 1,024-room Parc 55 hotel, according to a statement Monday. The company expects that it will eventually remove the hotels from its portfolio. “Now more than ever, we believe San Francisco’s path to recovery remains clouded and elongated by major challenges,” chief executive officer Thomas Baltimore said in the statement. The city faces “record high office vacancy; concerns over street conditions; lower return to office than peer cities; and a weaker-than-expected citywide convention calendar through 2027.” The last few years have been tumultuous for hotels, which were battered by early Covid lockdowns. While leisure travel has enjoyed a robust rebound, business trips have been slower to recover, putting stress on big properties in urban areas. San Francisco hotels have been especially vulnerable. The city’s office market has seen occupancies plummet, as tech employers embrace work-from-anywhere models and cut back on office space, and startups started worrying about their ability to raise new money. The city itself is facing worsening budget challenges, with the majority of residents saying San Francisco is on the wrong track. The San Francisco Travel Association estimates that the area will get 23.9 million visitors this year, down from 26.2 million in 2019. That’s led to falling demand for hotels. Occupancy rates for San Francisco hotels were just under 70% in the first four weeks of May, according to lodging data provider STR. By comparison, New York City hotels were 86% full during the same period. In the case of the Park properties, stopping payments on the non-recourse loan, which was funded through the commercial mortgage-backed securities market and matures in November, will remove a drag on the company’s balance sheet and operating performance, according to the statement.  Long-term rates continue upward trend. US mortgage rates edged up this week, according to Freddie Mac, with the 30-year fixed-rate loan creeping closer to the 7% threshold. The benchmark 30-year mortgage rate increased to 6.79%, up from last week’s 6.57%, Freddie Mac’s Primary Mortgage Market Survey showed. The 15-year fixed mortgage averaged 6.18%, a 21-basis-point jump from the previous week.  “Mortgage rates jumped this week, as a buoyant economy has prompted the market to price-in the likelihood of another Federal Reserve rate hike,” Freddie Mac chief economist Sam Khater said. “Although there has been a steady flow of purchase demand around rates in the low to mid 6% range, that demand is likely to weaken as rates approach 7%.”

According to the Mortgage Bankers Association, a higher contract interest rate for the 30-year loan has led to a 3.7% decline in the overall mortgage application volume. Refinance applications fell 7% week over week, and purchase activity dwindled 3%. “Inflation is still running too high, and recent economic data is beginning to convince investors that the Federal Reserve will not be cutting rates anytime soon. Mortgage rates for conforming, balance 30-year loans were being quoted above 7% by some lenders last week, and the weekly average at 6.9% reached the highest level since last November,” said Mike Fratantoni, MBA’s chief economist.  Delinquencies for major investor groups rise as economic stress deals hammer blow to CRE industry.

Commercial and multifamily mortgage delinquency rates climbed in the first quarter as a real estate recession hovers on the horizon. The Mortgage Bankers Association’s new quarterly analysis revealed that delinquency rates increased across the board for five of the largest investor groups: commercial banks and thrifts, commercial mortgage-backed securities (CMBS), life insurance companies, and Fannie Mae and Freddie Mac. These groups hold over 80% of commercial/multifamily mortgage debt outstanding. Based on the unpaid principal balance (UPB) of loans, delinquency rates for banks and thrifts increased to 0.58%. Life company portfolio delinquencies rose to 0.21%, Fannie Mae loan delinquencies edged up to 0.35%, Freddie Mac loan delinquencies were up to 0.13%, and CMBS delinquencies jumped to 3%. MBA’s head of commercial real estate research, Jamie Woodwell, pointed to the economic turmoil squeezing commercial real estate firms as the cause of the delinquency rate uptick. “Ongoing stress caused by higher interest rates, uncertainty around property values, and questions about fundamentals in some property markets are beginning to show up in commercial mortgage delinquency rates,” Woodwell said. “Delinquency rates increased for every major capital source during the first quarter, foreshadowing additional strains that are likely to work their way through the system.”  Agencies seek public comment on proposed rule for quality control of automated valuation models.

The Federal Housing Finance Agency and five other regulatory agencies have proposed a rule requiring originators to adopt quality control standards for automated valuation models (AVMs). The agencies encouraged the public and industry participants to submit their comments on the AVM rule with the goal of combating racial bias in home appraisals. AVMs are software-based pricing models used to determine property value and automate the process. However, an FHFA report in 2022 discovered discriminatory statements in some algorithmic appraisals. The proposed rule would implement policies, practices, procedures, and control systems to ensure that AVMs adhere to quality control standards designed to comply with non-discrimination laws, ensuring fair and accurate appraisals. The six agencies that proposed the rule include the FHFA, the Department of Treasury, the Federal Reserve System, the Federal Deposit Insurance Corporation, the National Credit Union Administration, and the Consumer Financial Protection Bureau. “The proposed standards are designed to ensure a high level of confidence in the estimates produced by AVMs; help protect against the manipulation of data; seek to avoid conflicts of interest; require random sample testing and reviews; and promote compliance with applicable non-discrimination laws,” the FHFA said in its news release. The National Association of Realtors released a statement on Thursday praising the move. “Realtors are dedicated to upholding fair housing laws in all aspects of real estate, including appraisals,” NAR president Kenny Parcell said. “We commend the PAVE task force for making these positive changes, and NAR is proud of our advocacy efforts in pursuing these actions. Over the past year, we have had discussions with the PAVE Task Force on an array of proposed solutions on which the Biden Administration, Realtors, and the broader appraisal industry could work together to address concerns and improve public trust in the appraisal profession. We are pleased to see the positive steps taken to improve the appraisal process and better protect the wealth-building benefits of homeownership for all Americans.”  FDIC releases startling new analysis.

The number of banks with financial, operational or managerial weaknesses increased during the first three months of this year, according to the Federal Deposit Insurance Corp. The FDIC said on Wednesday that the number of lenders on its confidential “Problem Bank List” increased by four to 43 between January and March. The total assets held by those lenders rose to $58 billion from $10.5 billion in the previous period, the regulator said in its Quarterly Banking Profile. Although the number of firms on the FDIC’s list remains relatively low compared with historical highs, it’s a reversal in a trend of several consecutive quarters of declines. Wednesday’s report spans a period in which three US banks buckled, including Silicon Valley Bank and Signature Bank. According to the FDIC, banks are placed on the problem bank list based on a key risk measure known as CAMELS. The score is based on a 1-through-5 scale, with 5 being the worst. Banks that are included have a score of 4 or 5, the regulator said. Still, FDIC Chairman Martin Gruenberg said that the banking system remained strong. “Despite the recent period of stress, the banking industry has proven to be quite resilient,” he said in a statement. “The most lasting effects of the industry’s response to that stress may not become apparent until second quarter results,” he added. In its report, the FDIC said banks had an “elevated level of unrealized losses on investment securities” due to increases in market interest rates. However, those losses on available-for-sale and held-to-maturity securities declined by 16.5% from the prior period to $515.5 billion, the regulator said. The watchdog said it was “closely monitoring liquidity and access to funding across the banking industry.” Overall, banks earned more interest from loans, but they also had to pay more to depositors, which on balance led to a decline in the industry’s net interest margin, according to the regulator. The FDIC said total deposits dropped 2.5% from the fourth quarter of 2022 to $18.7 trillion — it was the largest reduction since the agency began collecting the data in 1984. Silvergate Capital Corp. kicked off a wild three months in the banking sector on March 8 when it announced plans to wind down operations and liquidate its bank. Just two days later, Silicon Valley Bank collapsed into what was then the second-biggest failure in US history. Then on March 12, financial regulators closed Signature Bank and declared it to have failed. The FDIC said that the amount of money in its bedrock insurance fund declined $12.1 billion to $116.1 billion at the end of the first quarter. The regulator dipped into the fund to make all depositors whole at SVB and Signature Bank and has proposed a measure to help replenish the fund by charging banks a special assessment fee.  Demand is stifling.

US mortgage rates surged to the highest level since early November last week, stifling demand for home purchases and refinancings. The contract rate on a 30-year fixed mortgage increased 22 basis points to 6.91% in the week ended May 26, according to Mortgage Bankers Association data out Wednesday. The index for home purchases fell to the lowest level since early March. Refinancing activity was the weakest since late February, the MBA data showed. The survey, which has been conducted weekly since 1990, uses responses from mortgage bankers, commercial banks and thrifts. The data cover more than 75% of all retail residential mortgage applications in the US.  "We will see losses, no question about it," says Wells Fargo CEO.

The commercial real estate migraine ramped up a notch this week when stocks of large and mid-sized banks closed lower on Wednesday, according to a Reuters report. Hurt by concerns about office real estate loans, the S&P 500 Banks index closed down 2% while the benchmark S&P 500 index dropped 0.6%. Investors were rocked by comments from executives during the Sanford C Bernstein conference. Wells Fargo CEO Charlie Scharf warned there will be “losses, no question about it. But in the context of the overall portfolio and the overall size of our loan portfolio with the company, we are not overly concentrated in office (loan space).” Wells Fargo’s outstanding commercial real estate loans were $154.7 billion (16% of total loans), with $35.7 billion in office loans at the end of March. Potential loan defaults and declining values of office properties have posed concerns for some lenders in recent months. Blackstone president Jonathan Gray emphasized the “unprecedented weakness” in older office buildings, which accounts for less than 2% of the firm’s real estate equity portfolio. “Vacancy is 20-plus percent, rents are declining, companies now are obviously thinking about their space needs in light of remote work and the economic climate that’s ahead,” Gray said. “Lenders are reluctant to have exposure to office buildings. Buyers are reluctant. Valuations are going down.” However, the size of losses will be “dramatically different” compared to the housing crisis 15 years ago, according to Gray. Banks have set aside funds to cover potential loan losses for the recession expected to occur in the second half of the year. Mortgage credit supply decreased to a decade-low in April, mirroring the tightening in broader credit conditions after the banking crisis the month before, according to the Mortgage Bankers Association. |

|

- iMove Chicago

- Real Estate School

-

Laws

-

CRLTO

>

- 5-12-010 Title, Purpose And Scope.

- 5-12-020 Exclusions.

- 5-12-030 Definitions.

- 5-12-040 Tenant Responsibilities.

- 5-12-050 Landlord’s Right Of Access.

- 5-12-060 Remedies For Improper Denial Of Access.

- 5-12-070 Landlord’s Responsibility To Maintain.

- 5-12-080 Security Deposits.

- 5-12-081 Interest Rate On Security Deposits.

- 5-12-082 Interest Rate Notification.

- 5-12-090 Identification Of Owner And Agents.

- 5-12-095 Tenants’ Notification of Foreclosure Action.

- 5-12-100 Notice Of Conditions Affecting Habitability.

- 5-12-110 Tenant Remedies.

- 5-12-120 Subleases.

- 5-12-130 Landlord Remedies.

- 5-12-140 Rental Agreement.

- 5-12-150 Prohibition On Retaliatory Conduct By Landlord.

- 5-12-160 Prohibition On Interruption Of Tenant Occupancy By Landlord.

- 5-12-170 Summary Of Ordinance Attached To Rental Agreement.

- 5-12-180 Attorney’s Fees.

- 5-12-190 Rights And Remedies Under Other Laws.

- 5-12-200 Severability.

- Illinois Eviction Law (Forcible Entry And Detainer)

- Illinois Security Deposit Return Act

-

CRLTO

>

- Today's Cool Thing

- Social Media