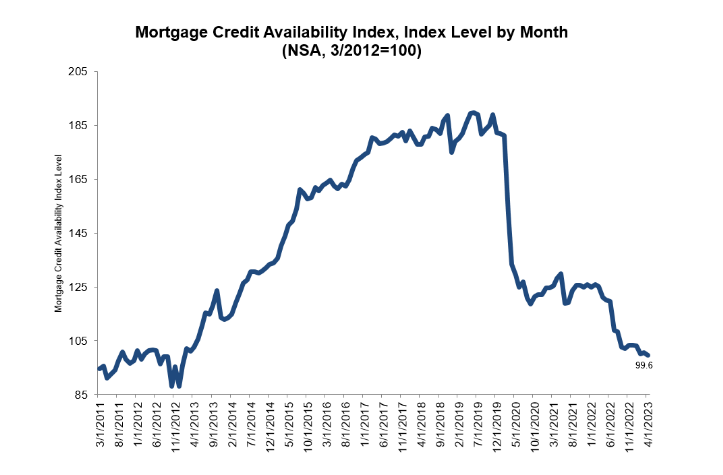

Contraction continues due to economic uncertainty and reduced mortgage demand Mortgage lenders continued to tighten their credit standards in April following the recent bank failures and subsequent market turmoil, the Mortgage Bankers Association reported Tuesday. MBA's Mortgage Credit Availability Index (MCAI) posted a nine-basis-point drop in April to 99.6, the lowest level in a decade.  "Mortgage credit availability declined in April to the lowest level since January 2013, reflecting the tightening in broader credit conditions stemming from recent banking sector challenges and an uncertain economic outlook," said MBA deputy chief economist Joel Kan. "The contraction was driven by reduced demand for loan programs such as certain adjustable-rate mortgage loans, cash-out and streamline refinances, and those with lower credit score requirements."

The index for conventional home loans ticked up 0.5%, while the government MCAI fell 2.1%. Of the component indices of the Conventional index, the jumbo MCAI saw a 1.5% rise, while the Conforming MCAI experienced a 1.1% decline during the period. "Government credit supply decreased for the third consecutive month, as industry capacity continues to adjust to significantly reduced origination volume, along with the expectations of a weakening economy later this year," Kan noted. "Even with high mortgage rates and reduced credit availability, the lack of for-sale inventory continues to be the biggest hurdle to more home purchase growth this year."

0 Comments

"The best of the boom may be behind us".

Almost half of US mortgaged homes were considered equity-rich in the first quarter, according to the findings of ATTOM's new home equity and underwater report. About 47.2% of mortgage residential properties were equity-rich in Q1, slightly down from 48% in Q4 2022. This drop marked the second consecutive quarterly decline in home equity, following 10 straight increases. "The equity downturn, small as it was, stood as the latest indicator of how a decline in home prices across much of the country has started to affect homeowners following a decade-long market boom," CoreLogic noted in the report. "It comes as home-seller profits have slid to their lowest point in two years." Meanwhile, 3% of mortgaged homes, or one in three, were considered seriously underwater in the first quarter. That figure was almost unchanged from 2.9% in the previous quarter and down from 3.2% in the same period a year ago. "Homeowners across the US continue to sit in a far better position than they were just a few years ago, with historically elevated levels of wealth built up in their properties," said Rob Barber, chief executive officer for ATTOM. "However, the recent downturn in the housing market is chipping away at the bounty they reaped from a decade of price surges. Home equity has fallen modestly amid a larger slump in profits homeowners are getting when they sell. It's still too early to call this a long-term trend, and there are reasons to hope for a market turnaround this year. For now, though, various measures suggest that the best of the boom may be behind us."  Conditions worsen due to "diminished economic outlook and elevated cost of debt".

Apartment market conditions continued to worsen in the first quarter as the prospect of slower economic growth weighed heavily on investors' minds, according to the National Multifamily Housing Council (NMHC). The NMHC's quarterly survey showed an across-the-board decrease in apartment market conditions, with all indexes – Market Tightness (31), Sales Volume (26), Equity Financing (23), and Debt Financing (29) – falling below the breakeven level (50). "Apartment operators reported an uptick in vacancies and concessions this quarter," said Caitlin Sugrue Walter, NMHC's vice president of research. "And while some of this softness can be attributed to seasonality, investors remain concerned about the coming wave of supply in some markets and the prospect of slower economic growth in 2023. Only 11% of quarterly survey respondents believe that the Fed will be able to achieve a soft landing this year in its effort to rein in inflation." The market tightness index came in at 31 in the first quarter, indicating looser market conditions. About 51% of the survey respondents reported markets to be looser than three months ago, while only 14% thought markets have become tighter. Meanwhile, 34% thought market conditions held steady over the past three months. The sales volume index reading of 26 marked the fourth straight quarter of decreasing deal flow, with 56% of respondents reporting lower sales volume. The equity financing index also fell for the fifth consecutive quarter to a reading of 23, reflecting views (60%) that equity financing has become less available. The debt financing index posted its seventh quarterly decline to 29. Fifty-three percent (53%) of respondents said debt financing has become less available, nearly a quarter (24%) thought that conditions were unchanged, while 12% reported that now is a better time to borrow than three months ago. "The transaction market, meanwhile, remains at a virtual standstill, with current apartment owners unwilling to offer buyers the lower prices necessary to compensate for both this diminished economic outlook and the elevated cost of debt," Walter added. "The Federal Reserve remains committed to bringing down inflation via tighter monetary policy, thereby raising the prospect of slower economic growth," NMHC wrote in the report. "A majority of quarterly survey respondents (64%) believed that a bumpy landing is the most likely scenario, where growth slows to a below average or negative rate and then rebounds to a sustainable pace. Twenty-one percent (21%) of respondents thought that the Fed's actions will lead to a hard landing, or recession scenario, while just 11% predicted a soft landing, where economic growth simply slows to a more sustainable pace."  MBA also reports reduced lender appetite for jumbo loans.

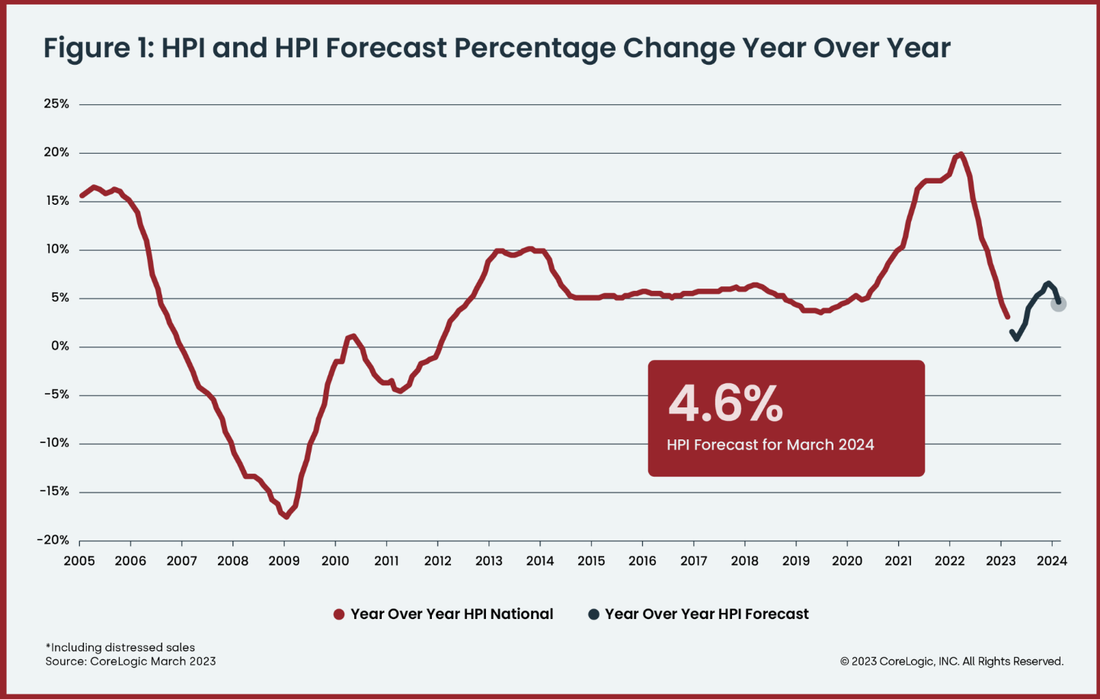

Mortgage application volume dropped last week, despite interest rates declining slightly for the first time in three weeks, the Mortgage Bankers Association reported Wednesday. MBA's Market Composite Index posted a 1.2% seasonally adjusted decrease from the week before and was down 0.4% on an unadjusted basis. The refinance index climbed 1% week over week, while the purchase index dipped 2%. Demand softened despite a five-basis point drop in the 30-year fixed mortgage rate, down to 6.5% last week, according to MBA chief economist Joel Kan. "Elevated rates continue to both impact homebuyer affordability and weaken demand for refinancing," Kan said. "Home purchase activity has been very sensitive to rates and local market trends, including the very low supply of existing-home inventory. However, newly constructed homes account for a growing share of inventory, giving more options for prospective buyers." Kan noted a reduced lender demand for jumbo loans as a fallout of bank failures in recent months. "The jumbo-conforming spread continues to narrow, an indication that there is reduced lender appetite for jumbo loans following the recent turmoil in the banking sector and heightened concerns about liquidity," he said. "The spread was 13 basis points last week, after being as wide as 64 basis points in November 2022." The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances fell to 6.37% from 6.40% the week prior.  Lack of affordability continues to weigh on home price growth. US home price growth has reached its lowest rate in more than a decade, according to CoreLogic's latest home price index (HPI). The annual appreciation of home prices fell to 3.1% in March, the lowest gain since spring 2012. Month-over-month, prices increased by 1.6% compared with February 2023.  "While housing markets across the country continue to send mixed signals, prices in many large metros appeared to have turned the corner, with the US recording a second month of consecutive monthly gains," said CoreLogic chief economist Selma Hepp. "At 1.6%, the month-over-month increase was twice the average seen between 2015 and 2020. The monthly rebound in home prices underscores the lack of inventory in this housing cycle."

Home prices continued to climb in all regions except the West, partially reflecting the region's affordability and inventory challenges. CoreLogic noted in the report that demand for higher-priced homes is weakening compared with median-priced homes, thus pulling appreciation down in that region at a faster pace. "While the lack of affordability generally weighs on home price growth, mobility resulting from remote working conditions appears to be a current driver of home prices in some areas of the country," Hepp said. Some prospective homebuyers remain hesitant due to inflation, slowing job gains and wage growth, and elevated mortgage rates. As a result of these conditions, CoreLogic expects annual home price growth to continue to decline over the spring and early summer before moving back up to 4.6% by March 2024. |

|

- iMove Chicago

- Real Estate School

-

Laws

-

CRLTO

>

- 5-12-010 Title, Purpose And Scope.

- 5-12-020 Exclusions.

- 5-12-030 Definitions.

- 5-12-040 Tenant Responsibilities.

- 5-12-050 Landlord’s Right Of Access.

- 5-12-060 Remedies For Improper Denial Of Access.

- 5-12-070 Landlord’s Responsibility To Maintain.

- 5-12-080 Security Deposits.

- 5-12-081 Interest Rate On Security Deposits.

- 5-12-082 Interest Rate Notification.

- 5-12-090 Identification Of Owner And Agents.

- 5-12-095 Tenants’ Notification of Foreclosure Action.

- 5-12-100 Notice Of Conditions Affecting Habitability.

- 5-12-110 Tenant Remedies.

- 5-12-120 Subleases.

- 5-12-130 Landlord Remedies.

- 5-12-140 Rental Agreement.

- 5-12-150 Prohibition On Retaliatory Conduct By Landlord.

- 5-12-160 Prohibition On Interruption Of Tenant Occupancy By Landlord.

- 5-12-170 Summary Of Ordinance Attached To Rental Agreement.

- 5-12-180 Attorney’s Fees.

- 5-12-190 Rights And Remedies Under Other Laws.

- 5-12-200 Severability.

- Illinois Eviction Law (Forcible Entry And Detainer)

- Illinois Security Deposit Return Act

-

CRLTO

>

- Today's Cool Thing

- Social Media