Applications remain less than a third of the market.

The dollar volume of refinance applications plunged 29.7% for the week ending Dec. 30, according to Fannie Mae’s Refinance Application-Level Index (RALI). On a year-over-year basis, refinance dollar volume was down by 86.2%. Its four-year average fell by 12.6% during the period. “Refinance applications decreased almost 30% as a result of the Christmas holiday-shortened week,” said Fannie Mae chief economist Doug Duncan. “With mortgage rates having moved sharply higher over the year, refinance activity ended 2022 down 86% compared with the end of the prior year.” RALI count decreased 27.2% week over week and was 85% compared to the same week ago. “Refinance applications remain less than a third of the market and are 87% lower than a year ago as rates remained close to double what they were in 2021,” said Joel Kan, deputy chief economist of the Mortgage Bankers Association. “Mortgage rates are lower than October 2022 highs but would have to decline substantially to generate additional refinance activity.” “The housing market remains in the doldrums with declining sales, inventory and prices,” added Sam Khater, chief economist of Freddie Mac. “The declines in sales and deceleration in home prices began swiftly earlier in 2022 but have moderated more recently. While the intensity of weakness is moderating, the market continues to decline and forward leading indicators suggest housing will remain weak throughout the winter.”

0 Comments

Home loan application volume hits 27-year low.

Mortgage applications fell over the past two weeks ago to the lowest level since 1996, according to the Mortgage Bankers Association’s holiday-adjusted report. The market composite index – a measure of mortgage loan application volume – declined 13.2%, while the unadjusted index was down 13.2% from two weeks earlier. MBA deputy chief economist Joel Kan said that the end of the year is typically a slower time for the housing market. Kan also pointed to high mortgage rates and the threat of a looming recession as the other main factors contributing to the decline. Refinance applications decreased by 16.3%, and purchase mortgage applications decreased by 12.2% when adjusted for the holidays. Compared to a year ago, refinance apps were down by 87%, and purchase applications were 42% lower. “Purchase applications have been impacted by slowing home sales in both the new and existing segments of the market,” Kan said. “Even as home-price growth slows in many parts of the country, elevated mortgage rates continue to put a strain on affordability and are keeping prospective homebuyers out of the market. “Refinance applications remain less than a third of the market and were 87% lower than a year ago as rates remained close to double what they were in 2021. Mortgage rates are lower than October 2022 highs but would have to decline substantially to generate additional refinance activity.” MBA noted that while the index changes were calculated relative to two weeks prior, the following compositional and rate measures are presented relative to the previous week only.  We take an in-depth look at the homeowner tax incentive. What is mortgage interest deduction? The mortgage interest deduction is a tax incentive for homeowners on the mortgage interest paid on the first $1 million of mortgage debt. Homeowners can deduct interest on the first $750,000 of the mortgage if they purchased their homes after December 15, 2017. It should be noted that you have to itemize on your tax return in order to claim the mortgage interest deduction. The mortgage interest deduction essentially lets homeowners count interest paid on loans for purchasing, building, or improving their primary home against their taxable income. Ultimately, this lowers the amount of taxes you owe, and, within limits, can be taken on loans for second homes. Since a mortgage interest deduction lets you reduce your taxable income by the amount you have paid in mortgage interest throughout the year, the interest you are paying on your home loan might help cut your tax bill. Mortgage interest deduction limit The mortgage interest deduction limit was signed in 2017, when the Tax Cuts and Jobs Act, or TCJA, lowered the mortgage deduction limit, altering individual income tax, and placing a limit on the amount you may deduct from your home equity loan debt. Prior to the Tax Cuts and Jobs Act, the limit for mortgage interest deduction was $1 million. In 2022, however, the limit dropped to $750,000, meaning that this tax year, married couples filing together and single filers can deduct the interest as high as $750,000. Married taxpayers filing separately can deduct has high as $375,000 each. The exceptions to the mortgage interest deduction limit include: - Mortgages taken out prior to October 13, 1987, are called grandfathered debt and are not limited, meaning all of the interest paid is deductible; - Homes bought after October 13, 1987, and prior to December 16, 2017, are eligible for the previous $1 million limit. If married and filing separately, that number becomes $500,000 each; and - Homes sold prior to April 1, 2018, are still eligible for the $1 million limit—if there was a binding contract signed prior to December 15, 2017, that closed prior to January 1, 2018, and the house was bought prior to April 1, 2018. What qualifies as mortgage interest? What qualifies as deductible mortgage interest includes the following: Interest on the mortgage for your primary home. Your primary home could include an apartment, a condo, a house, a mobile home, a co-op, and a houseboat. Properties that do not qualify as your primary home are properties that don’t have basic living accommodations, such as bathroom, cooking, and sleeping facilities. Additionally, the property must be listed as collateral for the loan you are deducting interest payments from. It also applies if you have a mortgage to buy out an ex-partner’s half of the property following a divorce. Interest on the mortgage for a second home. So long as your second home is listed as collateral for that mortgage, you can use the mortgage interest deduction on a mortgage for a home that is not your primary residence. If you rent out your second home, however, you must live there for more than 14 days, more than 10% of the days you rent it out, or whichever option is longer. You can only deduct the interest from one home if you have more than one second home. Mortgage points you have paid. You might have the option to pay mortgage points when you take out a mortgage, meaning you can pay a portion of your loan interest in advance. Points usually cost roughly 1% of your mortgage amount and can earn you roughly 25% off your mortgage rate. To qualify you for the deduction, mortgage points must be paid at closing and directly to the lender. In some cases, mortgage points can be deducted during the same year they’re paid. How to claim the mortgage interest deduction To claim the mortgage interest deduction, you can take the following steps: Form 1098. In January or early February, your mortgage lender will send you a Form 1098, detailing how much you paid in mortgage interest and points during the tax year. The lender will also send a copy to the IRS to match up what you report on your tax return. Keep records. You might also be able to claim mortgage interest deduction if you were a co-op apartment owner, used a portion of your house as a home office, rented out a portion of your home, the home was a timeshare, or a portion of the home was under construction that year. Other circumstances include the home being destroyed during the year or the homeowner using a portion of the proceeds to pay off debt or invest. Being divorced or separated but having to pay interest on a co-owned home might also qualify an individual for mortgage interest deduction, as well as you and someone who isn’t your spouse not being liable but paying the mortgage interest on your house. Itemize taxes. If you claim the mortgage interest deduction on Schedule A of Form 1040, you will need to itemize rather than take the standard deduction when you file your taxes.  US home price appreciation remains flat nationwide.

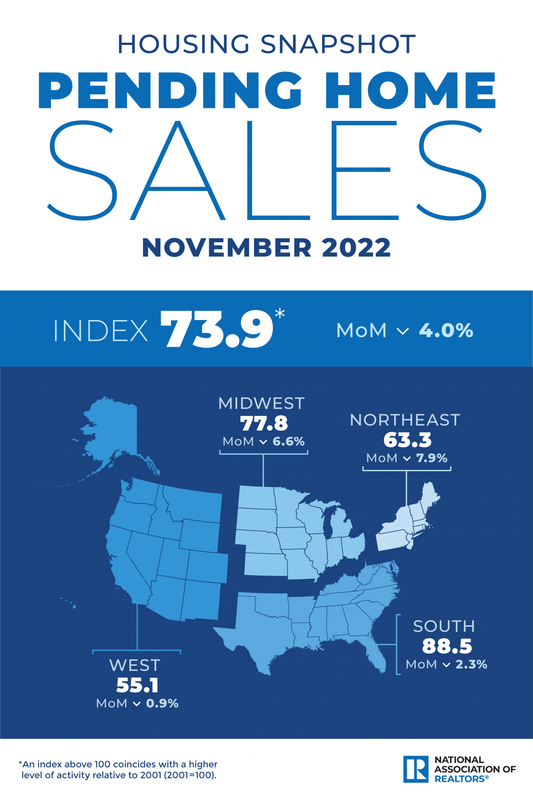

US home prices have finally stalled, posting two straight months of near-zero appreciation. The Federal Housing Finance Agency reported house prices experienced a 0.0% change in October. Price gains began slowing down to a 0.1% pace in September and decelerated to a single-digit rate for the first time in two years (+9.8% year over year in October). “Higher mortgage rates continued to put downward pressure on demand, weakening house price growth,” said Nataliya Polkovnichenko, supervisory economist in FHFA’s research and statistics division. “The US house price index growth decelerated as it posted the first 12-month growth rate below 10% after 24 consecutive months of double-digit appreciation rates.” On a seasonally adjusted basis, month-over-month house price gains in the nine census divisions ranged from -0.9% in the Pacific division to +1.4% in the New England division. Annual price changes were also positive, ranging from +4.5% in the Pacific division to +14.1% in the South Atlantic division. A CoreLogic forecast expects home prices to remain flat in November and climb on a 4.1% year-over-year basis. “Following the recent mortgage rate surge above 7%, real estate activity and consumer sentiment regarding the housing market took a nosedive,” said Selma Hepp, interim lead and deputy chief economist of CoreLogic. “Home price growth continued to approach single digits in October, and it will move in that direction for the rest of the year and into 2023. “However, while some housing markets have seen significant recalibration since the spring price peak and are likely to post losses in 2023, further deteriorating for-sale inventory, some relief in mortgage rate increases and relatively positive economic news may help eventually stabilize home prices.”  Record high-interest rates "drastically cut" into the number of pending home sales. Pending home sales posted the second-lowest monthly reading in two decades amid a high-interest-rate environment, according to the National Association of REALTORS. NAR’s Pending Home Sales Index (PHSI) – a forward-looking indicator of home sales based on contract signings – fell 4% for the sixth straight month to 73.9 in November. Compared to November 2021, contract activity levels were down by 37.8%.  “Pending home sales recorded the second-lowest monthly reading in 20 years as interest rates, which climbed at one of the fastest paces on record this year, drastically cut into the number of contract signings to buy a home,” said NAR chief economist Lawrence Yun. “Falling home sales and construction have hurt broader economic activity.

“The residential investment component of GDP has fallen for six straight quarters. There are approximately two months of lag time between mortgage rates and home sales. With mortgage rates falling throughout December, home-buying activity should inevitably rebound in the coming months and help economic growth.” According to NAR, all four regions recorded annual and monthly decreases. The Northeast PHSI plunged 7.9% month over month to 63.3, a decline of 34.9% from November 2021. The Midwest index decreased 6.6% to 77.8 in November, a decline of 31.6% from one year ago. The South PHSI dropped 2.3% to 88.5 in November, down 38.5% from the prior year. The West index dipped by 0.9% in November to 55.1, down 45.7% from November 2021. “The Midwest region — with relatively affordable home prices — has held up better, while the unaffordable West region suffered the largest decline in activity,” Yun said. |

|

- iMove Chicago

- Real Estate School

-

Laws

-

CRLTO

>

- 5-12-010 Title, Purpose And Scope.

- 5-12-020 Exclusions.

- 5-12-030 Definitions.

- 5-12-040 Tenant Responsibilities.

- 5-12-050 Landlord’s Right Of Access.

- 5-12-060 Remedies For Improper Denial Of Access.

- 5-12-070 Landlord’s Responsibility To Maintain.

- 5-12-080 Security Deposits.

- 5-12-081 Interest Rate On Security Deposits.

- 5-12-082 Interest Rate Notification.

- 5-12-090 Identification Of Owner And Agents.

- 5-12-095 Tenants’ Notification of Foreclosure Action.

- 5-12-100 Notice Of Conditions Affecting Habitability.

- 5-12-110 Tenant Remedies.

- 5-12-120 Subleases.

- 5-12-130 Landlord Remedies.

- 5-12-140 Rental Agreement.

- 5-12-150 Prohibition On Retaliatory Conduct By Landlord.

- 5-12-160 Prohibition On Interruption Of Tenant Occupancy By Landlord.

- 5-12-170 Summary Of Ordinance Attached To Rental Agreement.

- 5-12-180 Attorney’s Fees.

- 5-12-190 Rights And Remedies Under Other Laws.

- 5-12-200 Severability.

- Illinois Eviction Law (Forcible Entry And Detainer)

- Illinois Security Deposit Return Act

-

CRLTO

>

- Today's Cool Thing

- Social Media