High home prices deter homebuyers but remain a boon for sellers

July saw another month of decline for homebuyer sentiment, with Fannie Mae’s Home Purchase Sentiment Index hitting another survey low. The index decreased 3.9 points month over month to 75.8 and was up 1.6 points year over year. “Historically, prime home buying groups appear to be increasingly sensitive to the lack of affordability, as home prices continue to increase and homes for sale remain in short supply,” said Fannie Mae chief economist Doug Duncan. “While all surveyed consumer segments have reported increased pessimism toward homebuying conditions over the past several months, two of the segments perhaps best positioned to purchase – consumers aged 35-44 and those with middle-to-higher income levels – have indicated even more pessimism than other groups.” On the buy-side, 66% of consumers said it’s a bad time to buy a home, up from 64% in June; while on the sell-side, 75% of respondents said it’s a good time to sell, down slightly from 77% last month. “Overall, the HPSI remains within a tight range established a few months after the onset of the pandemic in 2020,” Duncan said. “The percentage of respondents citing high home prices as the top reason for it being a ‘bad time to buy’ also reached an all-time high. On the flip side, selling sentiment remains extremely high, and well above pre-pandemic levels, for the same commonly cited reason: high home prices.” There was a drop in the net shares of those expecting home prices to rise in the next 12 months (46%), lower mortgage rates (5%), and those who are not concerned about losing their job (84%). Meanwhile, the net share of respondents who said their income had improved over the past year remained unchanged at 27%.

0 Comments

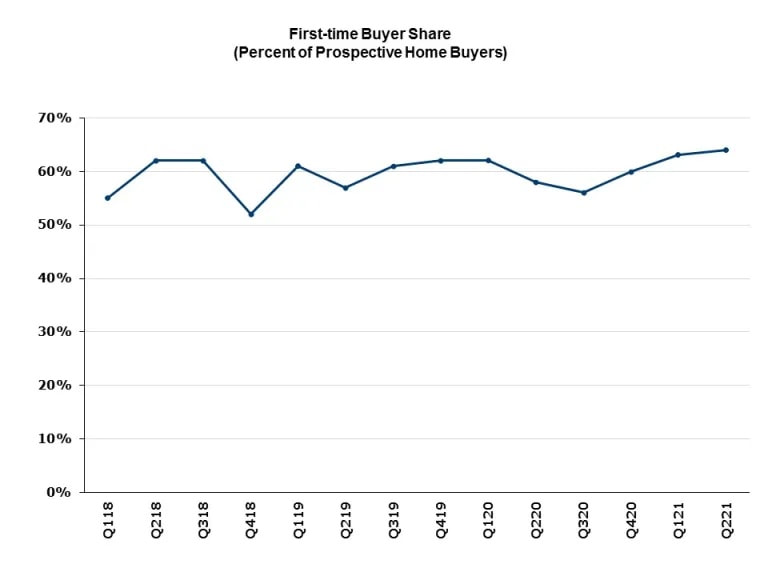

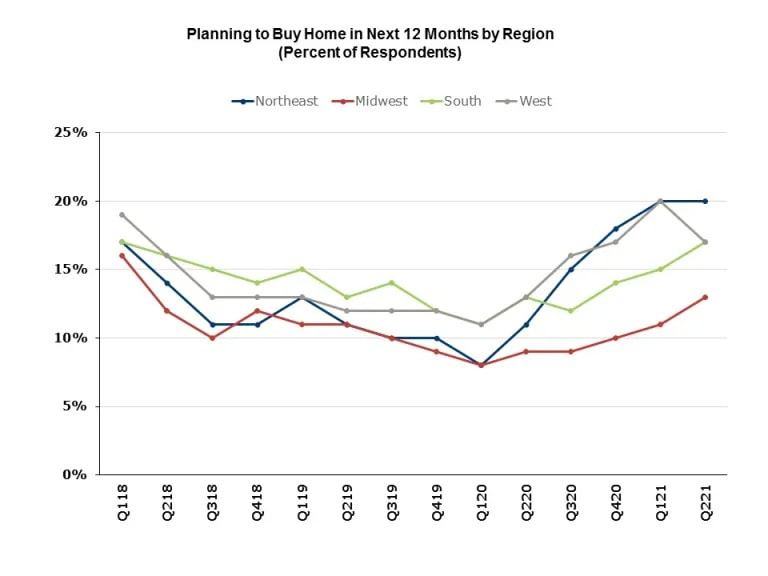

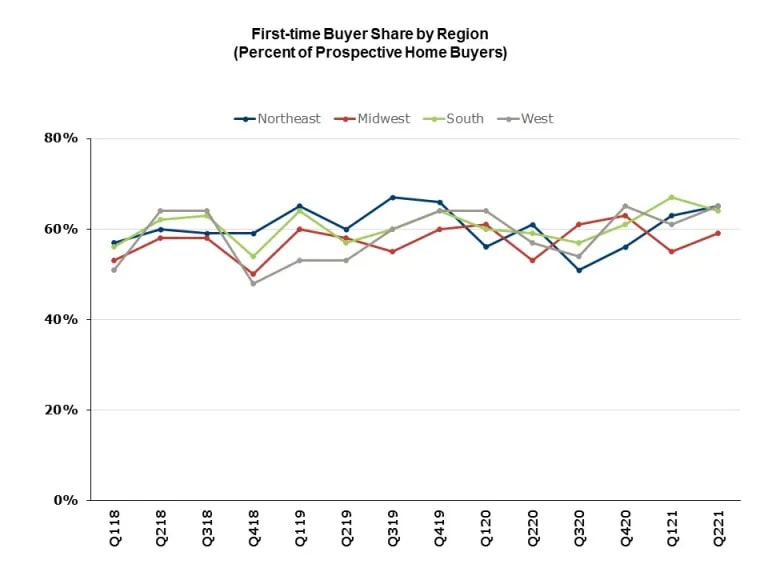

Seventeen percent of American adults are considering the purchase of a home within a year, according to NAHB’s Housing Trends Report (HTR) for the second quarter of 2021. The share (now seasonally-adjusted*) has increased for five consecutive quarters, after hitting a series low of 10% in the first quarter of 2020. The upward trend is clear evidence of Americans’ growing desire to become homeowners. Meanwhile, 64% of those prospective buyers in the second quarter of 2021 are first-time buyers– the highest share in the history of this series. The record high comes after three consecutive quarterly increases in the share of 1st-timers.  The Northeast is the region of the country with the largest share of adults planning a home purchase in the second quarter of 2021, at 20%. The share stood at only 8% in the first quarter of 2020. All other regions also saw a significant increase during this period: 8% to 13% in the Midwest, 11% to 17% in the South, and 11% to 17% in the West.  Over half of all prospective buyers in every region are first-time home buyers. In the second quarter of 2021, the shares stood at 65% in the Northeast, 59% in the Midwest, 64% in the South, and 65% in the West.   For many young or first-time homebuyers, purchasing a home can feel intimidating. A recent survey shows some homebuyers ages 25 to 40 may be unsure about the home buying process and what they can afford. It found:

If you’re interested in buying but aren’t sure where to begin, here are three key concepts about homeownership you should understand before you get started. 1. What You Need To Know About Down Payments Saving for a down payment is sometimes viewed as one of the biggest obstacles for homebuyers, but that doesn’t have to be the case. As Freddie Mac says: “The most damaging down payment myth—since it stops the home buying process before it can start—is the belief that 20% is necessary.” According to the most recent Home Buyers and Sellers Generational Trends Report from the National Association of Realtors (NAR), the median down payment for homes purchased between July 2019 and June 2020 was only 12%. That number is even lower when we control for age – for buyers in the 22 to 30 age range, the median down payment was only 6%. 2. You May Be Able To Afford More Home Than You Think Working remotely, exercising, and generally spending more time than ever in our homes has changed what many people are looking for in their living space. However, some young homebuyers don’t feel they can afford a home that suits their growing needs and have decided to continue renting instead. That means they’ll miss out on some of the long-term benefits of owning a home. As an article recently published by NAR points out: “Many young adults are underestimating how much they need for homeownership, the survey finds. Millennials underestimated how much home they can afford right now, how much interest they would pay over a 30-year mortgage, and how much home values appreciate, on average, over 10 years…” Knowing how much home you can afford when starting the buying process is critical and could be the game-changer that gets you from renting to buying. 3. Homeownership Will Become Less Affordable the Longer You Wait Finally, with mortgage rates starting to rise along with home prices appreciating, putting off buying a home now could cost you much more later. Sam Khater, Chief Economist at Freddie Mac, notes: “As the economy progresses and inflation remains elevated, we expect that rates will continually rise in the second half of the year.” Most experts forecast interest rates will rise in the months ahead, and even the smallest increase can influence your buying power. If you’ve been on the fence about buying a home, there’s no time like the present. Bottom Line: If you feel overwhelmed by the prospect of starting your home search, you’re not alone. Connect with a local real estate agent to learn more about the process, what you’ll need to start your search, and what to expect.  Americans take advantage of low borrowing costs

US household debt rose at the fastest pace since 2013 in the second quarter, driven by a mortgage boom as Americans took advantage of low borrowing costs and sought more space to work from home. Household liabilities climbed $313 billion to $14.96 trillion as of the end of June, a 2.1% rise from three months earlier, the Federal Reserve Bank of New York said in a report published Tuesday. Most of the increase came in mortgage balances. With the average 30-year rate declining in the period, millions of Americans with good credit took the opportunity to refinance and cut their monthly payments. Some 44% of the country’s entire $10.4 trillion stock of mortgages was originated in the 12 months through June, according to the New York Fed. “We have seen a very robust pace of originations over the last four quarters, with new extensions of credit for mortgages and auto loans combined with rebounding demand for credit-card borrowing,” said Joelle Scally of the Center for Microeconomic Data at the New York Fed. The US housing market has been so hot that many homeowners have higher levels of equity even though they’ve borrowed more. Home prices jumped 10.5% in the first half of 2021, according to Fannie Mae, the fastest pace on record. US homeowners withdrew about $50 billion in home equity in the first quarter, the most in more than a dozen years. Still, the opportunity hasn’t been available to everyone. Mortgage credit availability is down sharply since early 2020 when the pandemic was declared a national emergency, according to the Mortgage Bankers Association. More than 71% of mortgage originations in the second quarter were among borrowers with a credit score of at least 760, just shy of the 73% record in the previous three months. For other types of credit, like auto loans and credit cards, lending standards have been loosening, according to the Fed’s July Senior Loan Officer Opinion Survey released on Monday. Overall, household debt levels -- measured as a share of the economy -- remain well below the highs posted in the years leading up 2008 financial crisis. And some kinds of borrowing are still short of pre-pandemic levels in dollar terms. Credit-card balances, while they rose by $17 billion in the second quarter as the consumer economy rebounded, are about $140 billion lower than at the end of 2019. Pandemic policies -- from one-time checks and extra unemployment benefits to loan forbearance programs -- have helped Americans stay current on their debt, with delinquencies falling in most categories of borrowing. The biggest shift has been in student debt. About 5.7% of college loans were 90-plus days delinquent or in default at the end of June, compared with more than 11% before the pandemic. New York Fed officials said that delinquencies might start to increase as the COVID policies expire. The freeze on student loan repayments, for example, is due to end on Sept. 30.  Expectation is that forbearance exit volumes will put pressure on server’s operations

Around 65% of active forbearance plans are set to expire through the rest of 2021, and mortgage servicers may have to face the bulk of expirations earlier than expected. Approximately 1.86 million homeowners remained in forbearance as of July 20, according to data released Monday by Black Knight. Of that figure, nearly 950,000 plans – including nearly 80% of all FHA and VA loans – will expire in September and October alone. But due to the complexity of the forbearance expiration timelines across different federal agencies, Black Knight Data & Analytics president Ben Graboske is worried that this post-forbearance scenario will put servicers in a tough spot. “Over the course of just two months this fall, the nation’s mortgage servicers would have to process up to approximately 18,000 expiring plans per business day, guiding borrowers through complex loss mitigation waterfalls directed by changing regulatory requirements,” he said. Graboske explained that the “tiered forbearance plan lengths are designed to help shorten the overall window during which expirations will be taking place, and they do. But the current structure also results in the stacking of expiration activity upfront in the fall and noticeably increases the volume of expected forbearance expirations in late 2021 and early 2022, especially among FHA borrowers who may face heightened challenges in re-performing on their mortgages post-forbearance.” Graboske warned servicers to prepare for operational challenges related to the large volume of post-forbearance loss mitigation efforts. “The operational challenge this represents is staggering, even before noting the oversized share of FHA and VA loans,” Graboske said. “Given the heightened challenges those borrowers may face in returning to making mortgage payments as compared to those in GSE loans, effective loss mitigation efforts and automated processes become even more critically important.”  We like to congratulate our Managing Broker, Erickson Ocasio Payton, in getting accepted into the New York Real Estate Board and getting his real estate License. Congratulations to Erick.

|

|

- iMove Chicago

- Real Estate School

-

Laws

-

CRLTO

>

- 5-12-010 Title, Purpose And Scope.

- 5-12-020 Exclusions.

- 5-12-030 Definitions.

- 5-12-040 Tenant Responsibilities.

- 5-12-050 Landlord’s Right Of Access.

- 5-12-060 Remedies For Improper Denial Of Access.

- 5-12-070 Landlord’s Responsibility To Maintain.

- 5-12-080 Security Deposits.

- 5-12-081 Interest Rate On Security Deposits.

- 5-12-082 Interest Rate Notification.

- 5-12-090 Identification Of Owner And Agents.

- 5-12-095 Tenants’ Notification of Foreclosure Action.

- 5-12-100 Notice Of Conditions Affecting Habitability.

- 5-12-110 Tenant Remedies.

- 5-12-120 Subleases.

- 5-12-130 Landlord Remedies.

- 5-12-140 Rental Agreement.

- 5-12-150 Prohibition On Retaliatory Conduct By Landlord.

- 5-12-160 Prohibition On Interruption Of Tenant Occupancy By Landlord.

- 5-12-170 Summary Of Ordinance Attached To Rental Agreement.

- 5-12-180 Attorney’s Fees.

- 5-12-190 Rights And Remedies Under Other Laws.

- 5-12-200 Severability.

- Illinois Eviction Law (Forcible Entry And Detainer)

- Illinois Security Deposit Return Act

-

CRLTO

>

- Today's Cool Thing

- Social Media