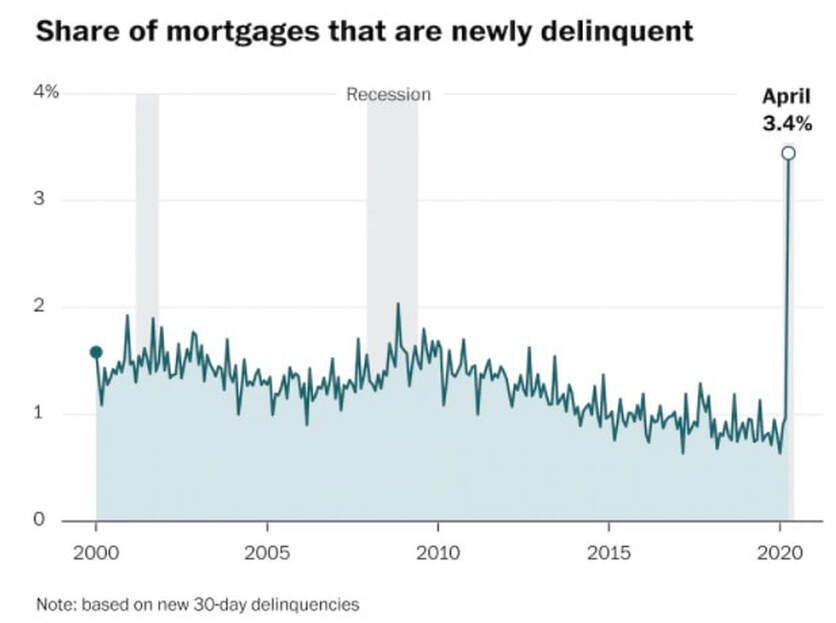

New mortgage delinquencies hit a record in April, well above anything seen during the Great Recession. Some 3.4 percent of Americans became at least 30 days delinquent on their mortgage in April, according to an analysis from CoreLogic. The real estate data firm’s figures include about three of four U.S. mortgages, going back to 1999. Mortgage delinquencies were among the first signs of the housing crisis and can signal underlying weakness in the housing market. But does the surge in delinquency mean a second housing crisis looms with a wave of foreclosures? Probably not. As with most data released during this coronavirus period, these figures come wrapped in caveats and uncertainty. For starters, the new delinquency figure includes an unknown number of households that are late on their payments because their loans are in forbearance, said Frank Nothaft, CoreLogic’s chief economist. On March 27, President Trump signed the Cares Act, which made it easy for qualified homeowners to request a total of 12 months of mortgage forbearance. That leaves a small window in which the first homeowners who applied for forbearance could show up in the April data. The forbearance program has been wildly popular. The Mortgage Bankers Association reports 4.1 million households were in forbearance as of July 5. To be sure, many applied after the April period measured here, and not all who apply for loan deferrals will actually fall behind on their payments. The program was broad, and many homeowners took advantage of the loan reprieve as a precautionary measure. Millions of Americans who didn’t have a loan backed by the federal government weren’t eligible for the program. “There are some loans that are not in forbearance that are going right into delinquency,” Nothaft said. There are endless reasons to fall behind on your payments right now. About 33 million people have lost their jobs and are receiving jobless benefits, Labor Department data show. The unemployment rate in April was at its highest since the Great Depression, plunging millions into dire financial situations, and the Federal Reserve projects unemployment will remain near double digits through the end of the year. Even excluding mortgage loan deferrals, a Census Bureau survey shows that as of June 30, about 8.4 million households missed a mortgage payment in the past month. That’s up from the end of April, when it stood at about 5 percent. I do think we’re going to see further increases in delinquency rates,” Nothaft said. And a year from now, if the economy hasn’t improved substantially by the time forbearance runs out, “you could be looking at a prospect where the lender begins foreclosure proceedings.” Delinquencies are concentrated in the Northeast and South, often in states harder hit in the earlier stages of the pandemic. If delinquencies continue to follow the virus, they could become a national phenomenon in the months to come. CoreLogic’s models forecast serious delinquency rates will quadruple during the next 18 to 24 months, meaning about 3 million borrowers could be at risk of losing their homes. That’s not to say the coronavirus crisis will be a repeat of the Great Recession. Almost 4 million homes were lost to foreclosure between 2007 and 2010, according to an analysis from the Federal Reserve Bank of Chicago, but the housing market is much healthier now. Subprime mortgages are rare, and homeowners have far more equity in homes. That leaves them in a much better position to weather a downturn and less likely to walk away from their homes when things go south. “Right now, there isn’t any risky behavior that’s resulting in a big rise in delinquencies,” said Redfin lead economist Taylor Marr. The housing market looks strong for now. There were 22 percent fewer homes for sale during the week ending July 4 than there were at the same time last year, according to Zillow, and ultralow interest rates have ensured steady demand from buyers. Low supply and high demand have had a predictable effect: Home prices are still climbing. That may change next year. If delinquencies lead to foreclosures, as the forbearance time period expires, we could see an increase in the number of properties on the market. It may be compounded by other stressed buyers, who need to cash out of their home to pay bills as the recession continues. The supply glut could increase further if shutdowns are lifted and homeowners who held off on selling during a pandemic suddenly flood the market. On the demand side, there are fears buyers could pull back as stimulus fades and unemployment remains high. Nothaft estimates home prices will fall about 6.6 percent from this May to the next. Mortgage giant Freddie Mac forecasts flat home prices next June. Redfin’s Marr, while optimistic, also says falling home prices are possible. However, he said, the supply glut could be alleviated by the long-awaited influx of first-time millennial home buyers, as well as the myriad forces that have prevented home builders from fully meeting demand. Like so many things right now, the future of the housing market ultimately depends on how quickly the novel coronavirus can be contained and whether the government’s stimulus programs will be extended as the pandemic drags on. “I would say the risk of a massive wave of foreclosures is pretty low,” Marr said. “I have high hopes that the government and other agencies will do what they can to keep people in their homes.”

0 Comments

On July 31, the extra $600 per week out-of-work Americans have been receiving as part of the federal CARES Act will be no more. With COVID-19 leading to a fresh round of lockdowns, unemployment still over 11 percent, and an estimated 17.6 million Americans unlikely to return to their pre-COVID-19 jobs, it’s crunch time for both the nation’s leaders and its unemployed workers.

In May, the Democrat-led House of Representatives passed the HEROES Act, which would extend the $600 benefit until January 2021. President Donald Trump deemed the Act “dead on arrival” after its passing, but has since changed his tune considerably, signaling that he is at least in favor of more stimulus checks. The HEROES Act is expected to face stiff resistance in the Senate once it reconvenes on July 20. But the Senate has no choice but to do something, says Michael Gregory, head of U.S. economics for BMO Capital Markets. The national unemployment situation alone is dire enough to make ending the program a colossal risk – both economically and politically. “We’re not at that point yet,” Gregory says. “Look at the jobs: We can say, ‘Fine, if we had three-quarters or 80 percent of the jobs back, maybe we could start thinking of winding these things down.’ But not at this point.” Senate Majority Leader Mitch McConnell has proven himself resistant to almost every bill passed by his Democratic rivals in the House. He may have no choice but to budge this time around, especially with one-third of the Senate up for re-election in less than four months. “If you’re a Democrat or Republican and you voted to cut off aid without less than half the people getting their jobs back yet, that’s a hard sell. Politically, they’re going to do something,” Gregory says. What that something is remains a mystery – perhaps a new round of stimulus checks? – but maintaining some form of enhanced unemployment benefits is considered the most impactful solution by some experts. As Harvard professor Raj Chetty explains, providing greater unemployment assistance ensures that federal funds will not only go to the people who most need them, they will also be more likely to be recycled back into the economy, which should speed its recovery. A stimulus check delivered to every American, on the other hand, would conceivably lead to well-to-do recipients squirreling the funds away rather than spending them. “We should be focusing on unemployment insurance and expanding safety net programs like SNAP fundamentally because those programs provide social insurance — they mitigate economic hardship in a time of crisis,” Chetty said in remarks to CNBC. In a development that will shock no one, the debate around extending unemployment benefits has been heavily politicized, with critics of such payments asserting that it disincentivizes people from working. “It was clearly the case for some workers in some states where the minimum wage was very low that they were actually getting more money not working than if they were working at their minimum wage job,” Gregory says. “That is a tremendous disincentive. There are a lot of anecdotes of businesses starting up and having a hard time finding the labor they need.” It's a line of thinking Chetty disagrees with. “It’s not that lots of folks who have jobs to go back to are choosing not to go, but there’s no work to do,” he says. Gregory thinks the eventual solution will involve some sort of incentive component, possibly in the form of continued, though decreased, assistance for people who show a willingness to go back to work. National Economic Council Director Larry Kudlow has suggested the Trump administration was working on a similar measure, but has provided no details. “It’s still costs the government something, but much less than it did before,” Gregory says. Whether it’s convincing employers to keep workers on their payrolls or encouraging out-of-work Americans to start pounding the pavement in search of new jobs, Gregory says incentives are the name of the game. “It’s all about incentives at the end of the day. Incentives for employers to maintain their payrolls and incentives for workers to want to not sit at home and collect cheques,” he says. “It’s a big experiment that we’re conducting.”  A spike in early-stage delinquencies pushed the national mortgage delinquency rate to its highest level in more than four years, according to a new report from CoreLogic.

As of April, the latest month covered in CoreLogic’s Loan Performance Insights Report, 6.1% of home mortgages were in some stage of delinquency (defined as at least 30 days past due, and including homes in foreclosure). The April delinquency rate spiked 2.5 percentage points from March as the impact of the COVID-19 outbreak and the resulting recession impacted borrowers’ ability to make their mortgage payments. The spike ended a 27-month streak of consecutive year-over-year decreases in the delinquency rate, and pushed the rate to its highest level since January of 2016. The share of mortgages in early-stage delinquency – 30 to 59 days past due – was 4.2% in April, up from 1.7% the year before. The share of mortgages 60 to 89 days past due was 0.7%, up from 0.6% in April of 2019. However, the serious delinquency rate – defined as 90 days or more past due and including loans in foreclosure – inched down to 1.2% from 1.3% last year, hitting its lowest level since June 2000. The foreclosure inventory rate fell from 0.4% to 0.3%, its lowest level in at least 21 years, according to CoreLogic. New York had the highest delinquency rate at 10%, while South Dakota had the lowest at 3%. All states posted annual increases in their overall delinquency rates. The states that saw the biggest jumps were New York (up 4.7 percentage points), New Jersey (up 4.6 percentage points), Nevada (up 4.5 percentage points) and Florida (up four percentage points). A record 32 million American adults were living with their parents or grandparents in April, according to the Current Population Survey from the U.S. Census Bureau, an increase of 9.7 percent over a year ago. The data, analyzed by Zillow researchers, showed that 2.7 million adults moved back home in March and April, and that about 2.2 million of them were aged 18 to 25 — also known as Generation Z.

The trend began well before the pandemic for what has been called the “boomerang generation,” and these returning adult children and their parents have been known to clash as they face the challenges of navigating their new adult relationships. Landlords, however, have a problem that family meetings can’t solve: lost rent. Gen Zers who returned to their childhood bedrooms in March and April represent lost rental revenue of $726 million a month, the survey shows. While that figure is only 1.4 percent of the total U.S. rental market, losses affect some landlords and areas disproportionately. This week’s chart, drawn from data provided by Zillow, shows the cities with the greatest dollar losses (New York topped the list, along with other large, expensive cities), as well as those with the greatest share of the market affected (overwhelmingly, college towns). Should at-home learning continue in the fall, college-town landlords and their local economies will suffer further.  Housing markets on the East Coast and in Northern Illinois are the most vulnerable to impact from the COVID-19 pandemic, according to a new report from ATTOM Data Solutions.

The report also found clusters in New York City, Baltimore and Washington, D.C., on the East Coast and Chicago in Illinois. It found that East Coast states running from Connecticut through Florida, plus Illinois in the Midwest, had 43 of the 50 counties most vulnerable to the economic impact of the pandemic. The West was less vulnerable, with only four Western counties in California in the top 50, and no other counties on the West Coast or in Southwestern states. Markets were considered at risk based on the percentage of homes currently facing possible foreclosure, the portion of underwater homes, and the percentage of local wages required to pay for major homeownership expenses, ATTOM said. “Home-sales data from around the country is starting to show that eight years of price gains may be coming to an end amid the economic damage flowing from the virus pandemic,” said Todd Teta, chief product officer with ATTOM Data Solutions. “It’s still too early to make definitive calls, but the latest number show storm clouds gathering over the market.”  A recent report by Redfin found that redlining, the racist housing policy that first began preventing Black families from securing home loans almost 90 years ago, is still impacting the fortunes of Black homeowners today.

“The typical homeowner in a neighborhood that was redlined for mortgage lending by the federal government has gained 52% less—or $212,023 less—in personal wealth generated by property value increases than one in a greenlined neighborhood over the last 40 years,” writes the report’s author, Dana Anderson. Black homeowners, Anderson explains, are almost five times more likely to own in a formerly redlined neighborhood than in a greenlined neighborhood. Much of the economic equality faced by Blacks in America can be traced back to the diminished home equity that results from this redlining hangover. As many white homeowners discovered decades ago, home equity is one of the most powerful tools for creating generational wealth. Black families living in formerly redlined neighborhoods are still waiting for their chance to find out what that’s like. Redfin agent Brittani Walker deals with the effects of redlining every day in Chicago. “Homebuyers have boundaries they’ve set for themselves, or a friend of a friend has set for them,” she says. “They don’t want to buy in certain neighborhoods, especially on the South Side in formerly redlined areas, because those places don’t get the culture, the restaurants, the fun events – they don’t even get healthy food at grocery stores. And that contributes to why home prices don’t go up in those neighborhoods.” Like so many of America’s current problems, redlining can be traced back to the nineteenth century, when an 1896 Supreme Court decision upheld the constitutionality of racial segregation. When the Home Owners’ Loan Corporation began redlining in the 1930s, many U.S. cities were segregated into Black and white neighborhoods. That allowed HOLC to slice up communities based on their racial make-up and color code them, both literally and figuratively, on local maps. A descending scale affixed higher “mortgage security” to green neighborhoods, followed by blue (“still desirable”), yellow (“definitely declining”) and red (“hazardous”). Predominantly black neighborhoods were the ones most likely to be redlined. “In redlined neighborhoods,” writes Anderson, “it was virtually impossible to get a loan.” According to Redfin chief economist Daryl Fairweather, America’s atrocious homeownership gap – 44 percent of Blacks own homes compared to 73.7 percent of whites – can be directly traced to redlining. The idea of “Type A” and “Type B” neighborhoods, introduced by redlining into the public consciousness, still persists. Minorities face discrimination when buying homes in “Type A” neighborhoods, which forces many of them to buy in less desirable areas where homes don’t appreciate nearly as quickly. Redfin found that Black homeowners are 4.7 times more likely to own in a former “Type D” or redlined neighborhood than in a “Type A” neighborhood. “[I]t’s one major reason why Black families today have less money than white families to purchase homes either as first-time or move-up homebuyers,” Fairweather says. “That has had a lingering effect on their children and grandchildren, who don’t have the same economic opportunities as their white counterparts. Not only are Black parents less likely to have the resources to pay for higher education and help with other expenses, but studies show that children of homeowners are about 7.5% more likely to become homeowners than children of renters.” Tai Christensen, director of governmental affairs at CBC Mortgage Agency, says the housing industry needs to do more if it’s serious about bringing economic and political equality to Blacks in America. “Increasing equitable access to credit for minorities will create intergenerational wealth these communities have yet to enjoy,” she says. “Decreasing the homeownership gap between blacks and whites can solve for inequities such as the quality of education, access to healthy foods and quality healthcare, and other amenities within these neighborhoods.”  Available mortgage credit decreased again in June as investors continued to hold back from purchasing certain loans amid economic uncertainty caused by COVID-19.

MBA's Mortgage Credit Availability Index (MCAI) dwindled by 3.3% to 125 in June, indicating a tightening in lending standards. The baseline of the index was set to 100 in March 2012. Investors' unwillingness to buy jumbo and non-QM loans drove the downturn last month, according to Joel Kan, associate vice president of economic and industry forecasting at MBA. "Mortgage credit supply dropped again in June, as investors further reduced their willingness to purchase jumbo loans and those with lower credit scores. Lenders are navigating a gradual economic and housing market recovery that is still facing headwinds from the ongoing COVID-19 pandemic," he said. "The overall credit availability index decreased 3.3% to its lowest level since April 2014, with all of the sub-indexes falling to lows not seen since 2014-2015." The MCAI for conventional loans fell 4.1%, while the government MCAI dropped by 2.8%. Of the component indices of the Conventional MCAI, the Jumbo MCAI was down by 7.3%, and the conforming MCAI was 1% lower than the previous month. "Credit supply has fallen over 30% since February – before the pandemic – with an 18% decrease in government loan availability, and a 57% drop in jumbo loan availability," Kan said.  In remarks to the Senate Judiciary Committee on June 9, the assistant director of the FBI’s Criminal Investigative Division described for lawmakers a range of schemes being used to defraud unsuspecting Americans during the coronavirus pandemic. Rather than being brought under control, Calvin A. Shivers explained to the SJC that the threats have only become more frequent and sophisticated.

“Moreover,” Shivers said, “they adversely affect the United States by destabilizing our financial system and institutions and harming people at higher risk, including older adults and people with underlying medical conditions.” Shivers provided multiple examples of fraud schemes that are still proving effective:

In addition to taking extra precautions when emailing documents that contain personal information, such as password-protecting attachments, Scheumack says consumers also need to make sure they are storing their sensitive information properly. “The best way to send sensitive info is to request a secure place to upload the files,” he says. “If a consumer used their smartphone to scan their W-2 or tax return, make sure those documents are deleted from the phone’s files right away. If not, and you lose your phone or it’s stolen, someone else might have access to your personal information.” As Scheumack explains, borrowers may have their guard down as they go through the home loan process because they are expecting to share their personal information. “They know their tax information, pay stubs, etc., are going to be requested,” he says. “But when it comes to such sensitive information, now is the time for them to be especially cautious when sharing it.” Scheumack says borrowers should always be double-checking senders’ email addresses, ignoring unexpected attachments, and not clicking on hyperlinks before verifying their authenticity. “A good rule to follow is to contact the lender, underwriter or real estate agent to confirm they sent the email before moving forward,” he says. This may seem like common sense to most readers, but frazzled homeowners can easily miss these small details. They need to know that their lack of vigilance can have catastrophic results. Scheumack says mortgage professionals should urge their clients to keep their guard up even after they’ve purchased a home. “This is when homebuyers receive the most amount of unsolicited email, mail and phone calls,” he says, “some of which can resemble communication from their new mortgage company but in reality could be another attempt to steal personal information.”  Wells Fargo is quadrupling its balance requirement for customers applying for jumbo refis.

The lending giant is now requiring new customers to bring at least $1 million in balances if they want to refinance a jumbo mortgage, according to a CNBC report. That’s up from their previous balance requirement of $250,000. The policy change was part of a July 1 overhaul of lending guidelines that lowered the threshold for jumbo refinances for existing Wells Fargo customers, while making it much more difficult for new customers to qualify, sources with knowledge of the matter told CNBC. While many lenders have tightened mortgage credit in response to the COVID-19 pandemic, that tightening has been especially pronounced at Wells Fargo, which is also operating under an asset cap imposed by the Federal Reserve in response to its numerous scandals. In May, the bank hit pause on accepting HELOC applications. The month before that, Wells Fargo restricted its jumbo mortgage program, announcing that it would only refinance jumbo loans for customers who had $250,000 in liquid assets in the bank. However, the move caused plenty of dissension within the ranks, according to CNBC. Demand for refis is 111% higher than it was a year ago at this time, according to the Mortgage Bankers Association – and Wells Fargo mortgage personnel complained that they had to turn away good customers who sought to take advantage of historically low rates. In response, Wells Fargo last week issued an “expansion of guidelines” that nixed the $$250,000 requirement for existing customers, according to CNBC. Under the expansion, customers with a Wells Fargo bank or brokerage account of any level, or those who already had a mortgage with Wells Fargo, were able to access jumbo refinances. “The changes we implemented on July 1 substantially increased the number of borrowers from which we’ll accept applications for non-conforming refinances,” Tom Goyda, Wells Fargo spokesman, said in a statement. But if new customers want a jumbo refinance, they’re out of luck unless they bring a million bucks to the bank, CNBC reported. The requirement can be satisfied with a combination of deposits or investment balances. Wells Fargo also tightened mortgage lending standards across the board in the overhaul, sources told CNBC. For both primary and secondary home mortgages, the bank reduced the LTV by 5%. It also boosted its post-closing liquidity requirement for borrowers from 12 to 18 months, CNBC reported. Black borrowers are denied mortgages at 3 times the rate of white borrowers in these cities7/9/2020  Black borrowers are denied mortgages at 3 times the rate of white borrowers in these citiesNearly 16% of Black Americans who apply for mortgages are rejected, while just 7% of white Americans are rejected, according to a new analysis of Home Mortgage Disclosure Act data from Redfin.

That gap is even wider in Milwuakee, San Francisco, Detroit, Chicago and St. Louis. In those cities, denial rates for Black borrowers are more are more than 10 percentage points higher than they are for white borrowers. In Milwaukee and San Francisco, Black borrowers are more than three times as likely to be denied a mortgage than white borrowers. “Getting denied a loan serves a huge blow to a person’s self-esteem – especially for people of color, who often feel like the world is already falling in on them,” said Brittani Walker, a Redfin agent in Chicago. “My mother has been a renter since she moved out of her parents’ house. I tried to get her pre-approved for a mortgage a couple of years ago, but she was rejected because she has some blemishes on her credit. She broke down in tears and hasn’t tried again since. When people of color are stuck in this cycle of renting, their children often meet the same fate, missing out on thousands of dollars’ worth of home equity. If your parents never owned a home, where do you learn the value of homeownership?” Overall, Americans are only half as likely to be denied a mortgage today as they were in the aftermath of the 2008 financial crisis, Redfin said. In 2008, the share of total applicants who were rejected for a mortgage was 18%. By 2019, that figure had dropped to 8.9%. However, Black loan seekers are more frequently denied due to debt and low credit scores, according to the report. “These two factors are more likely to be roadblocks for Black mortgage applicants due to decades of wealth inequality, as well as bias among lenders,” Redfin said. While the mortgage gap between Black and white borrowers has narrowed in recent years, Black loan seekers are still denied home loans at a higher rate than white loan seekers in every one of the 50 most populous US metro areas. Milwaukee had the largest gap, with 19.5% of Black mortgage applicants rejected, as opposed to just 4.8% of white applicants. “In other words, Black applicants are four times more likely to face rejection,” Redfin said. San Francisco has the second-largest gap (19.2% vs. 5.9%), followed by Detroit (20.3% vs. 7.2%), Chicago (18.5% vs. 5.7%), and St. Louis (18.1% vs. 5.6%). Not coincidentally, Milwaukee is the most segregated metro area in the nation, with nearly 90% of Black residents living in the inner city. Chicago, Detroit and St. Louis are the third, fourth and sixth most segregated, Redfin said. Milwaukee also has the second-lowest Black homeownership rate of any metro in the country. Just 27% of Black families own their own homes there, compared with 70% of white families – 13 percentage points wider than the national homeownership gap. “The residue of redlining is still very tangible in Milwaukee and Chicago,” said Arnell Brady, a Redfin Mortgage advisor who originates in both cities. “Segregation continues to perpetuate the uneven playing field for Black communities, which are severely underserved when it comes to financial education and access to credit. Buying a home isn’t like walking into a bank and getting a credit card. Everyone wants a piece of the American dream, but that’s hard to achieve when you don’t have access to the right tools and information.” The metro with the smallest gap is San Diego, where 10.8% of Black mortgage applicants are rejected, compared with 7.3% of white applicants. Seattle (10% vs. 5.2%) is in second place, followed by Sacramento (11.2% vs. 6.2%), Anaheim (13.2% vs. 8.1%), and Las Vegas (13.7% vs. 8.1%). |

|

- iMove Chicago

- Real Estate School

-

Laws

-

CRLTO

>

- 5-12-010 Title, Purpose And Scope.

- 5-12-020 Exclusions.

- 5-12-030 Definitions.

- 5-12-040 Tenant Responsibilities.

- 5-12-050 Landlord’s Right Of Access.

- 5-12-060 Remedies For Improper Denial Of Access.

- 5-12-070 Landlord’s Responsibility To Maintain.

- 5-12-080 Security Deposits.

- 5-12-081 Interest Rate On Security Deposits.

- 5-12-082 Interest Rate Notification.

- 5-12-090 Identification Of Owner And Agents.

- 5-12-095 Tenants’ Notification of Foreclosure Action.

- 5-12-100 Notice Of Conditions Affecting Habitability.

- 5-12-110 Tenant Remedies.

- 5-12-120 Subleases.

- 5-12-130 Landlord Remedies.

- 5-12-140 Rental Agreement.

- 5-12-150 Prohibition On Retaliatory Conduct By Landlord.

- 5-12-160 Prohibition On Interruption Of Tenant Occupancy By Landlord.

- 5-12-170 Summary Of Ordinance Attached To Rental Agreement.

- 5-12-180 Attorney’s Fees.

- 5-12-190 Rights And Remedies Under Other Laws.

- 5-12-200 Severability.

- Illinois Eviction Law (Forcible Entry And Detainer)

- Illinois Security Deposit Return Act

-

CRLTO

>

- Today's Cool Thing

- Social Media